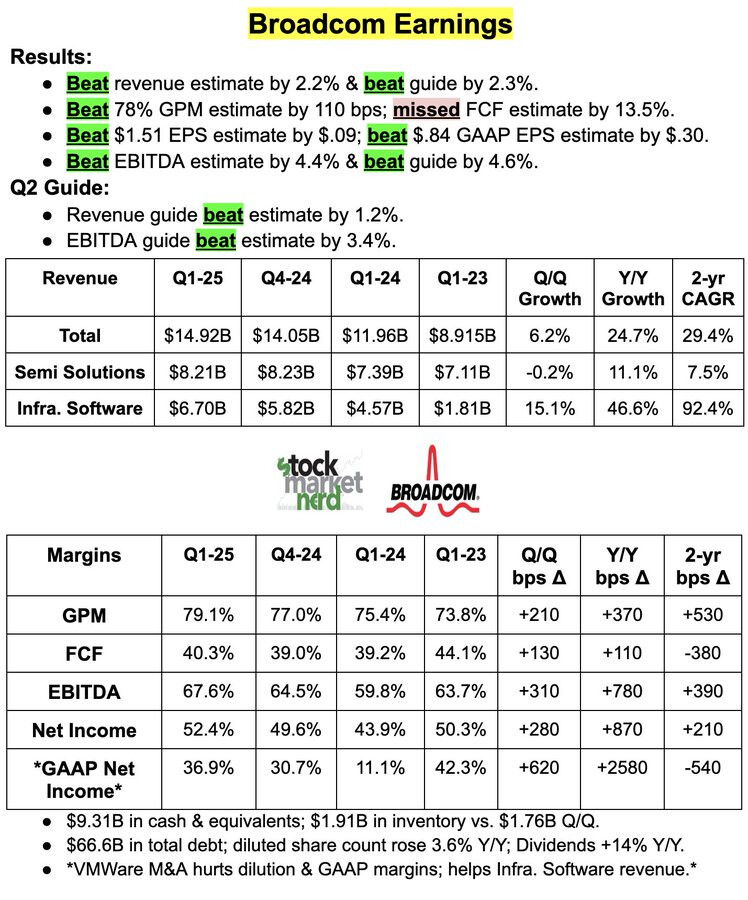

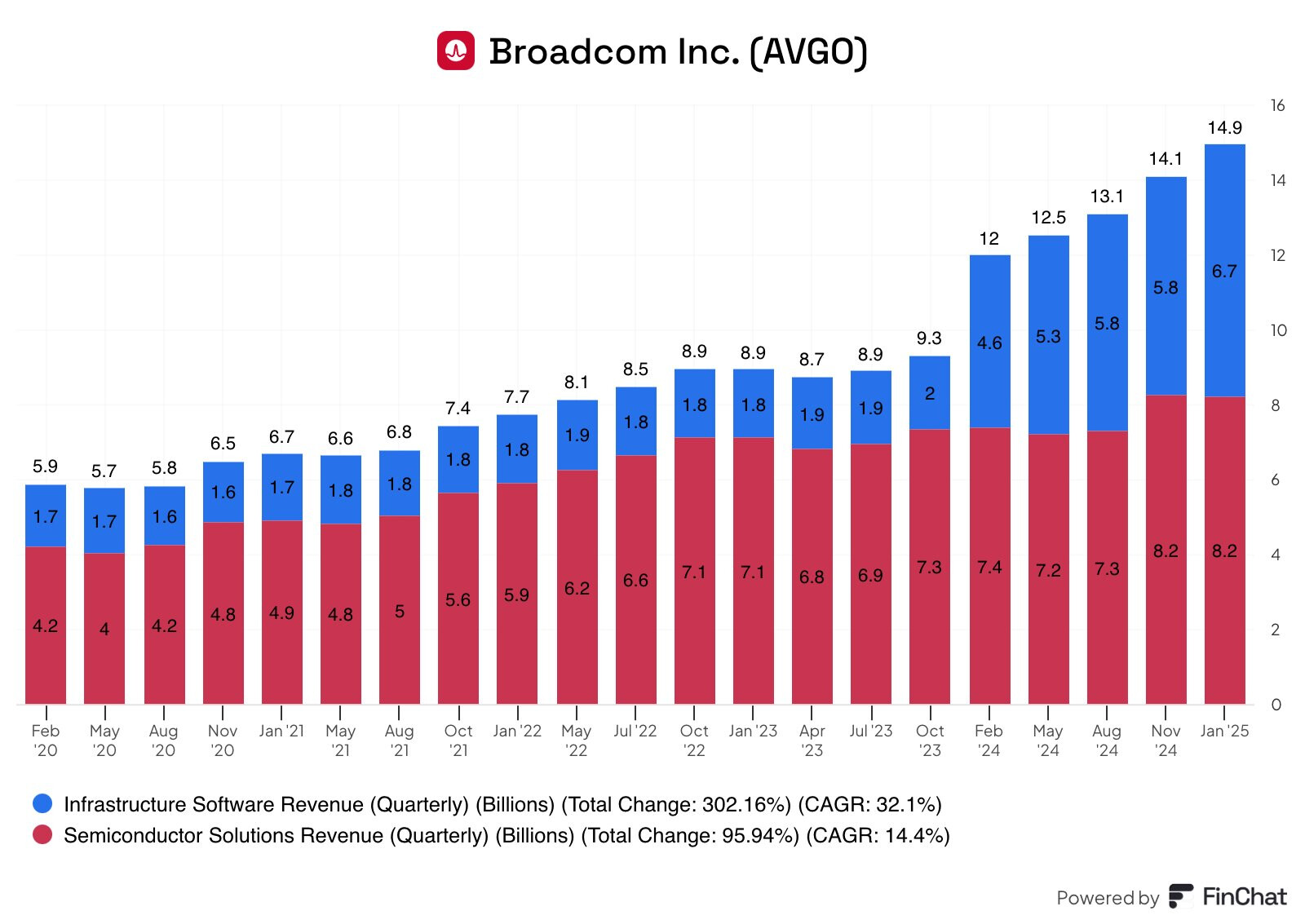

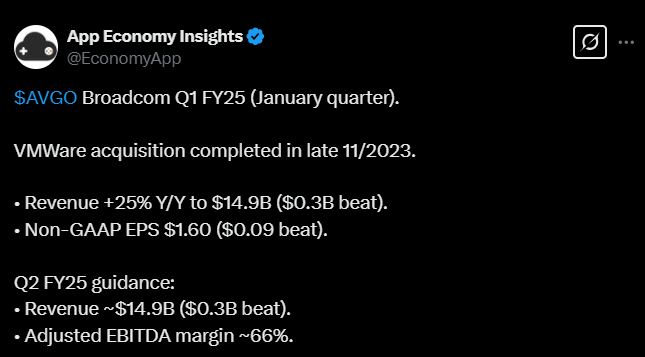

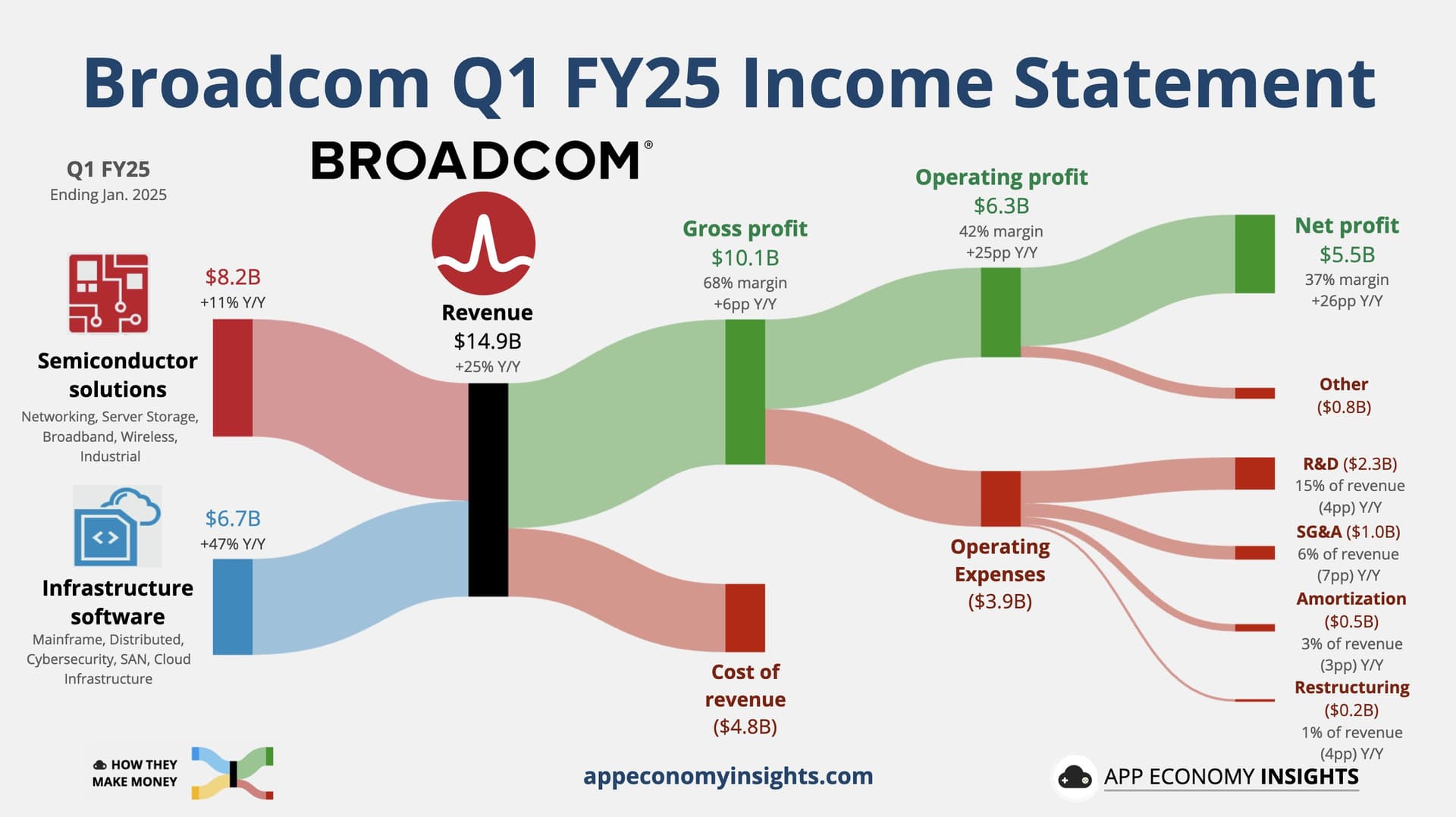

Bodari exceeded expectations in both revenue and profit.

The VMware acquisition accelerated the growth of the software business, and the company had succeeded in boosting its operational activities. Investors are concerned about the high valuation, which is above the industry average, and semiconductor supply chain issues could cause production delays and cost pressures, increasing future uncertainty.

I previously thought it would decline in the aftermarket (I suspected it was due to future outlook), but it actually went up.

Jeff Geerling made a small video that reminded me of the existence of RISC-V.

RISC-V is an open and free processor architecture that is comparable to the x86 architecture (Intel and AMD) and the ARM architecture (e.g., Apple and practically all mobile devices).

RISC-V is currently significantly behind those two mentioned in most applications, but even though the machine Jeff tested (HiFive Premier P550) is painfully slow and doesn’t even run YouTube properly, for example, Witcher 3 (an AAA game from ten years ago) does work, albeit only at 1-2 FPS (with an AMD graphics card, of course).

A lot has to be working correctly for it to work at all.

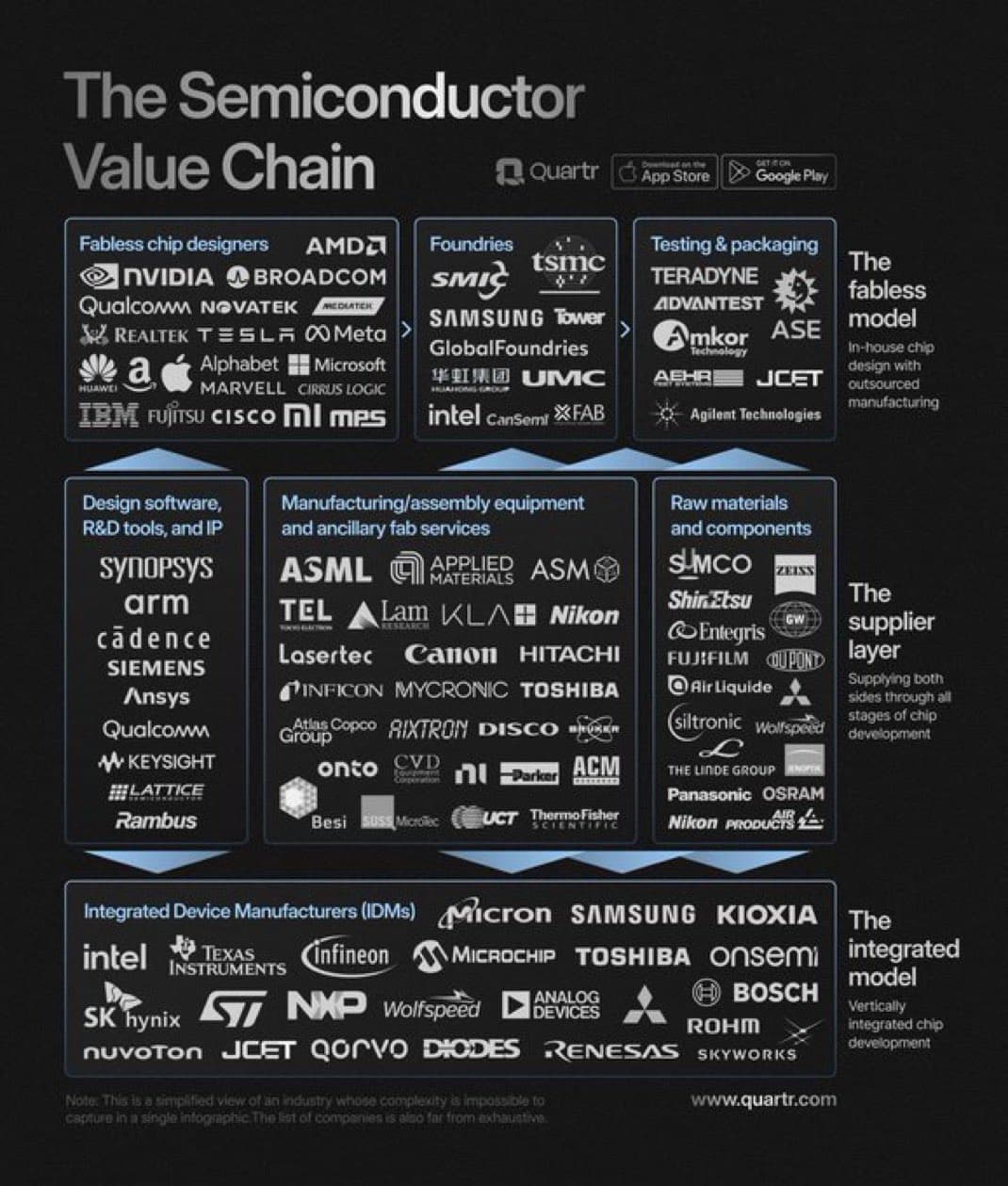

TSMC on ehdottanut yhdysvaltalaisille sirusuunnittelijoille, kuten Nvidialle, AMD:lle ja Broadcomille, sijoitusta yhteisyritykseen, joka operoisi Intelin valimoliiketoimintaa. TSMC ei kuitenkaan omistaisi yli 50 %:a. Neuvottelut ovat alkuvaiheessa ja liittyvät Trumpin hallinnon pyrkimykseen pelastaa vaikeuksissa oleva Intel.

Intel kärsii suurista tappioista, ja sen osakkeet ovat menettäneet yli puolet arvostaan. Yhtiön hallitus tukee neuvotteluja, mutta osa johtajista vastustaa niitä.

Lisäksi 18A-valmistusprosessi on ollut neuvotteluiden kiistanaihe, koska Intel väittää sen olevan parempi kuin TSMC:n 2 nm -prosessi.

This sounds like a potentially more realistic scenario than the previous rumor that TSMC would buy them. It’s clear that TSMC couldn’t own more than 50% of them, as that would take control out of American hands. Presumably, TSMC would be involved in offering its know-how to get expensive equipment to produce better results. Still, the scenario would be strange in that TSMC would join in supporting the operations of a major competitor’s factories.

However, conflicts of interest inevitably come to mind; i.e., is it in TSMC’s interest to ensure that Intel’s manufacturing side always remains safely far enough behind so that TSMC can continue printing money…?

It would be much healthier for the semiconductor market if Intel stayed in the race and manufactured modern goods – as there are only three competitors at the forefront of technological development (TSMC, Samsung, Intel), and Intel’s collapse out of the race would lead to a duopoly for the latest chips, which has essentially been the case for the last few years as Intel has stumbled.

He’s not a familiar face from Poland or Finland, so I don’t know this guy who was chosen as Intel’s CEO.

Right… so Intel appointed Lip-Bu Tan as CEO to strengthen production and generally investor confidence. As a former executive at Cadence Design Systems, he has strong experience in creating growth. Zinsner and Holthaus are reportedly continuing in their current roles; I don’t know them either. Perhaps they are local gems and pioneers.

Here’s a bit about Intel’s new CEO and especially his salary.

He will receive a base salary of one million dollars, as well as approximately 66 million dollars worth of stock options and awards that will “vest” in the coming years. In addition, he can earn bonuses and additional shares if the company’s stock price develops favorably.

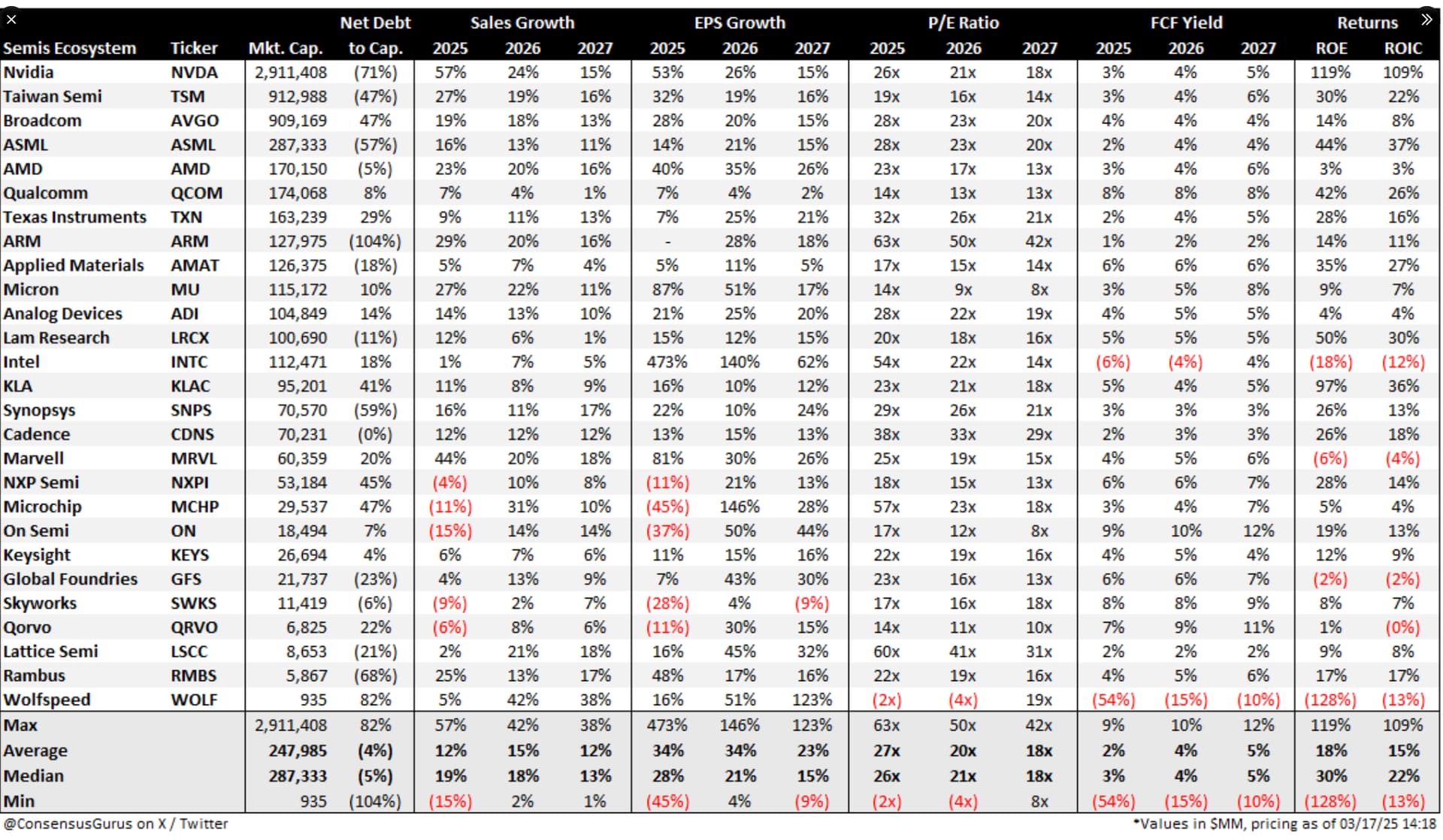

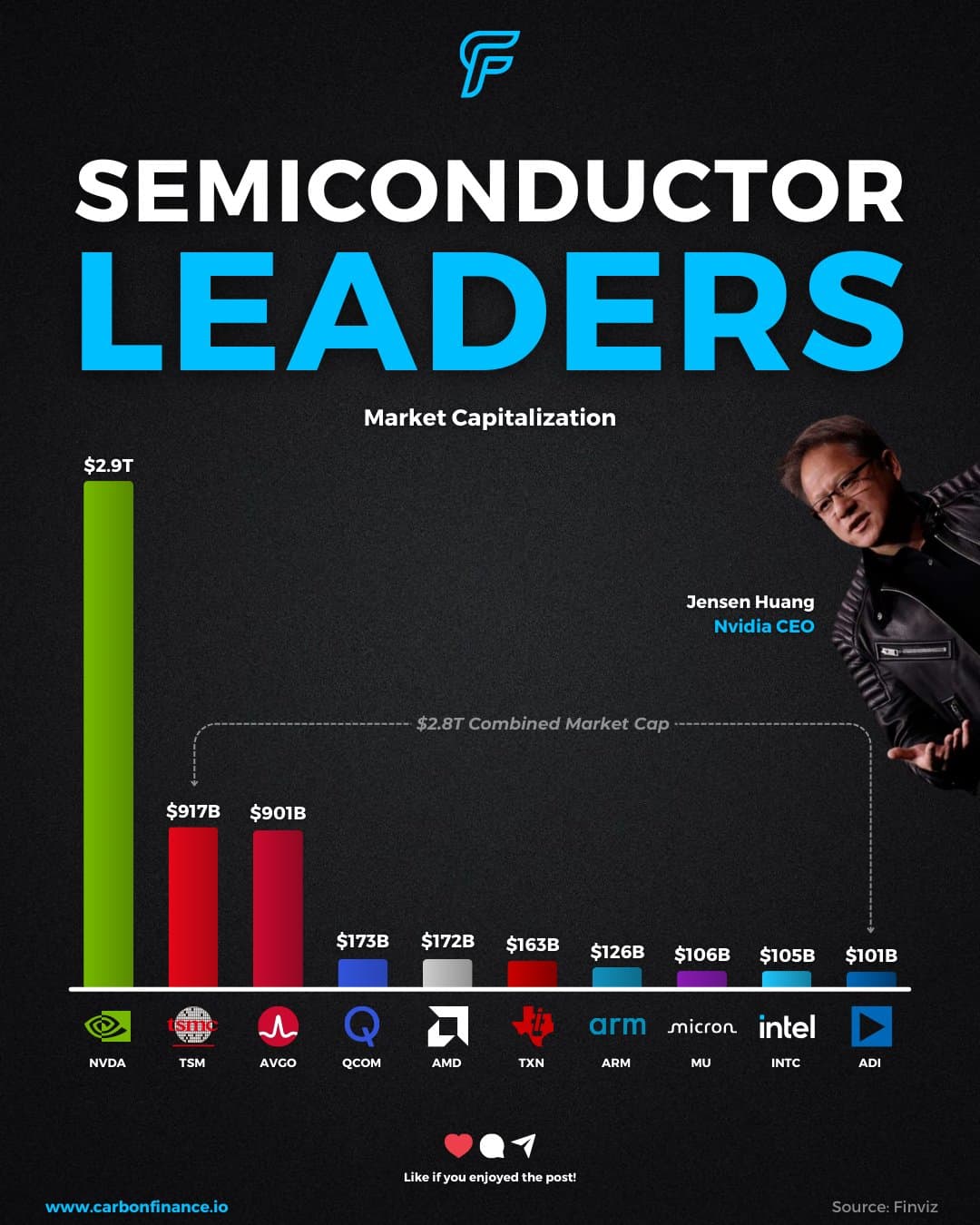

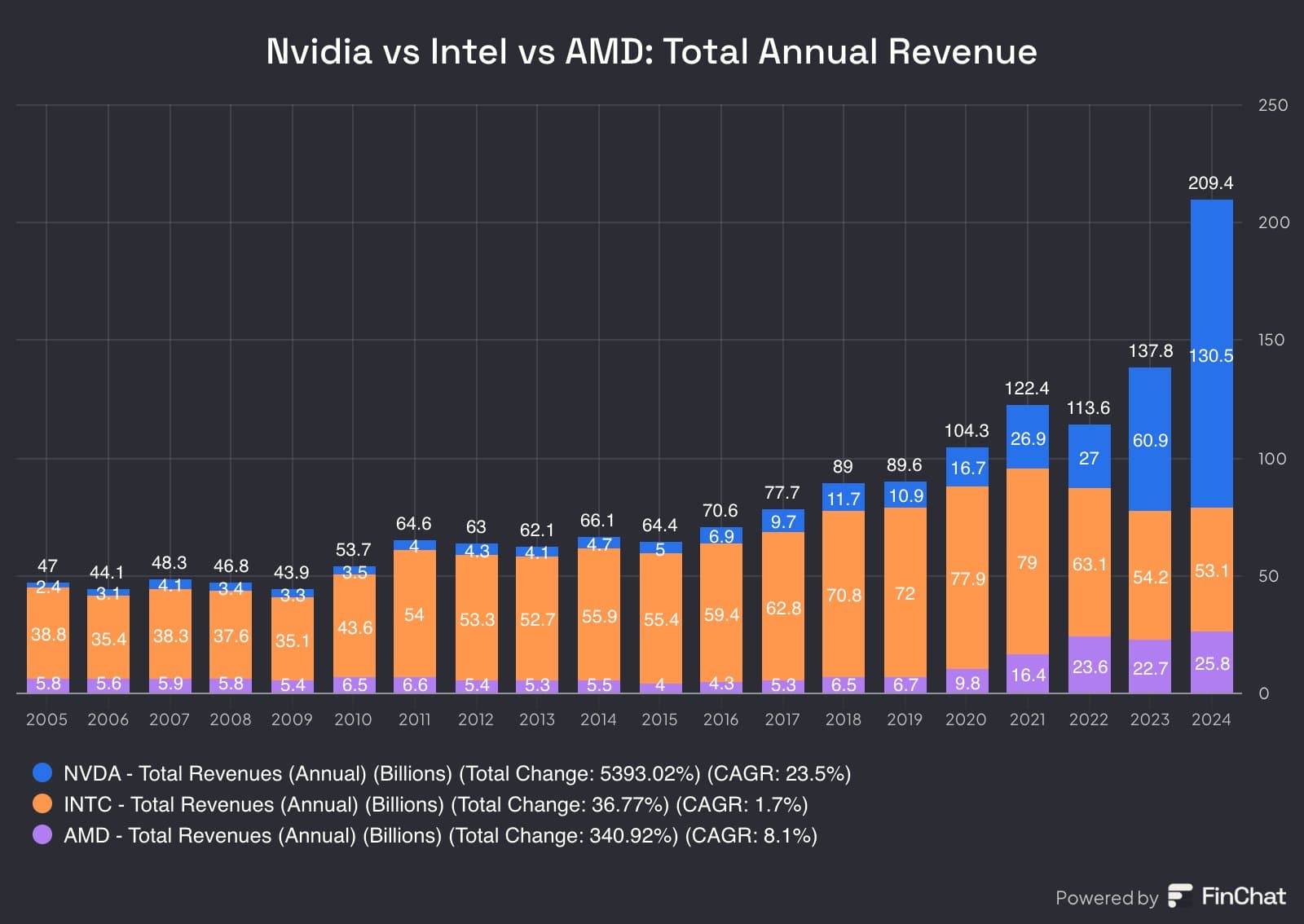

Here are the market capitalizations of companies in the industry for comparison; Nvidia’s dominance is not surprising. However, I didn’t realize that the second and third ones are so big. Intel’s and AMD’s “smallness” was a bit surprising.

That was an excellent chart. It makes me wonder greatly why the valuation difference between AMD and Intel is so incredibly large.

You see, looking at the curve of the last couple of years with a simple visual analysis, it would seem that Intel’s drop has stabilized and AMD’s rise has also somewhat slowed down. So the valuation differences should be quite moderate. But they are not, instead they are huge.

What do the markets know? Or are they just guessing?

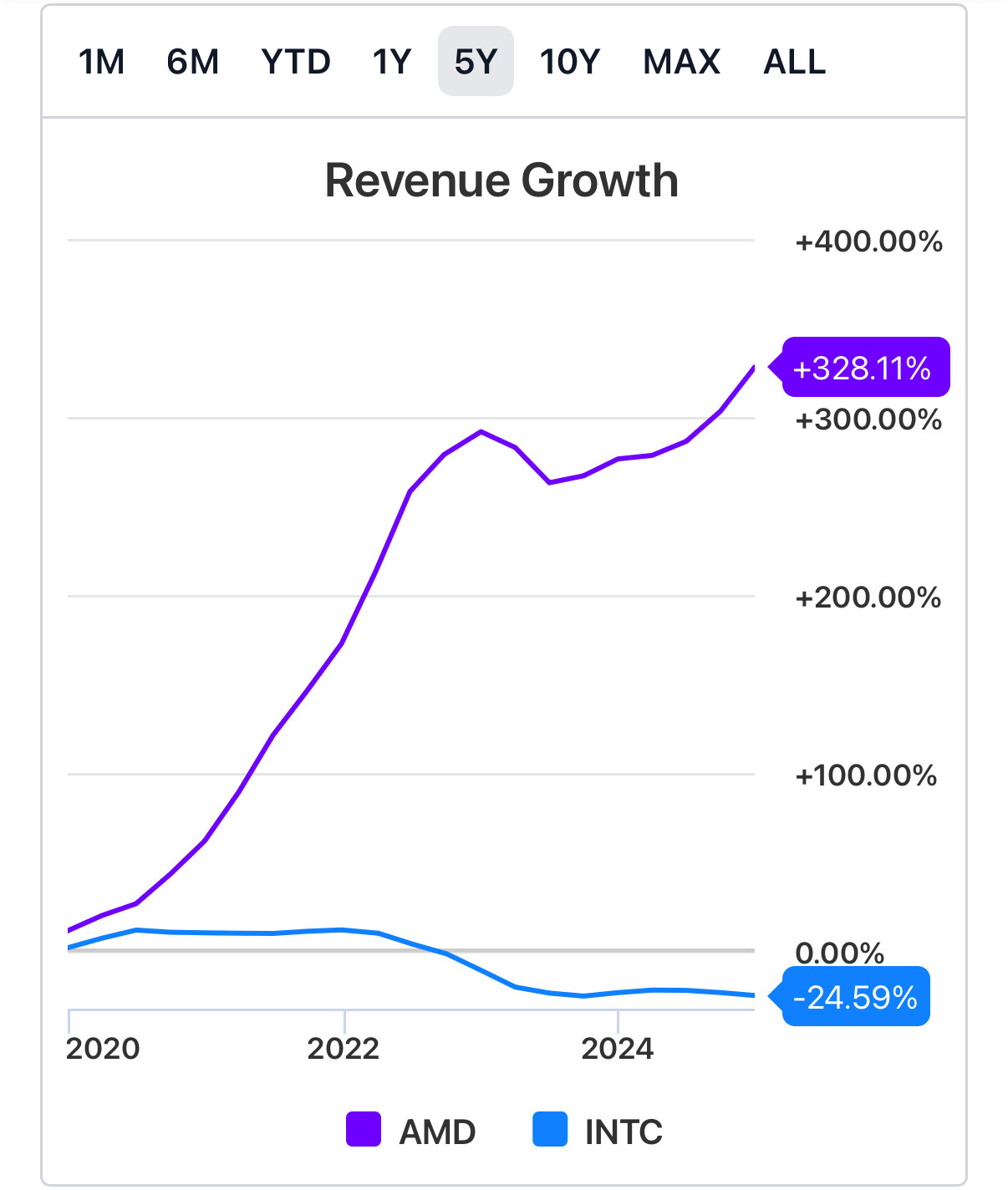

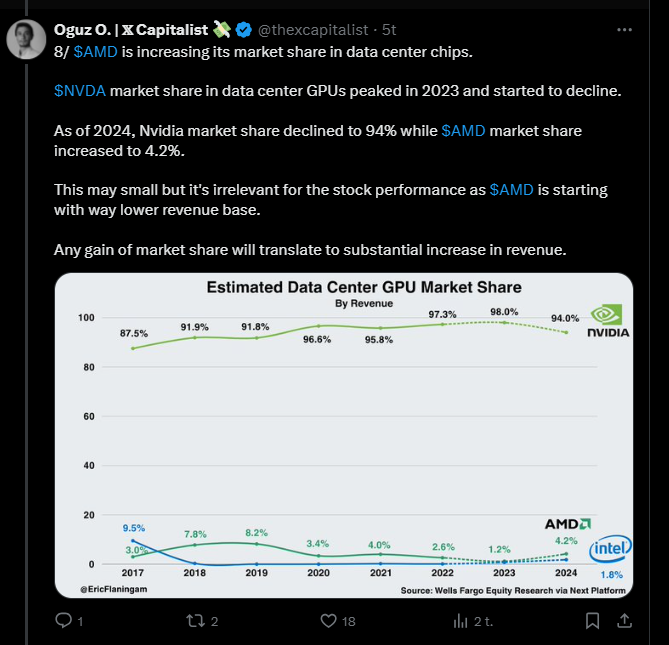

AMD’s business is constantly developing in the right direction. This cumulative revenue growth chart illustrates the point quite well. AMD is constantly taking market share from Intel and has also gained a fair foothold on the DC (Data Center) side, where NVIDIA operates.

Well now, if the curve continued the same way as from the beginning of the picture to the middle, then even a huge difference in valuation would be justified. But I was trying to ask, that when the curves from the middle of the picture to the right edge of the picture have no longer been nearly as dramatic, then shouldn’t the valuation differences even out among themselves?

Of course, if AMD’s curve for the last six months continues and continues, then yeah, AMD will pull further ahead. But is there a basis to predict that will happen?

Intel is not growing this year either, and AMD is growing by 25%. Intel’s Forward PE is 48 and AMD’s is 22. Intel’s numbers would need to turn significantly in different directions for the stock to start looking attractive from a valuation perspective. Currently, their strategy is purely defensive.

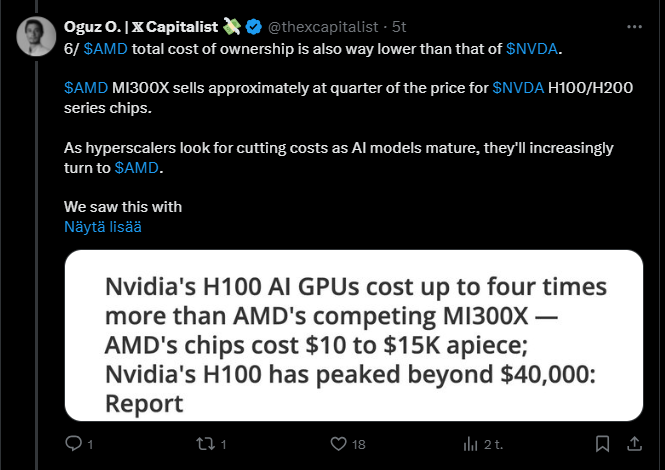

The tweet thread predicts that AMD is on the rise because its data center revenue grew by 69 percent last year, and the company is starting to outperform Nvidia.

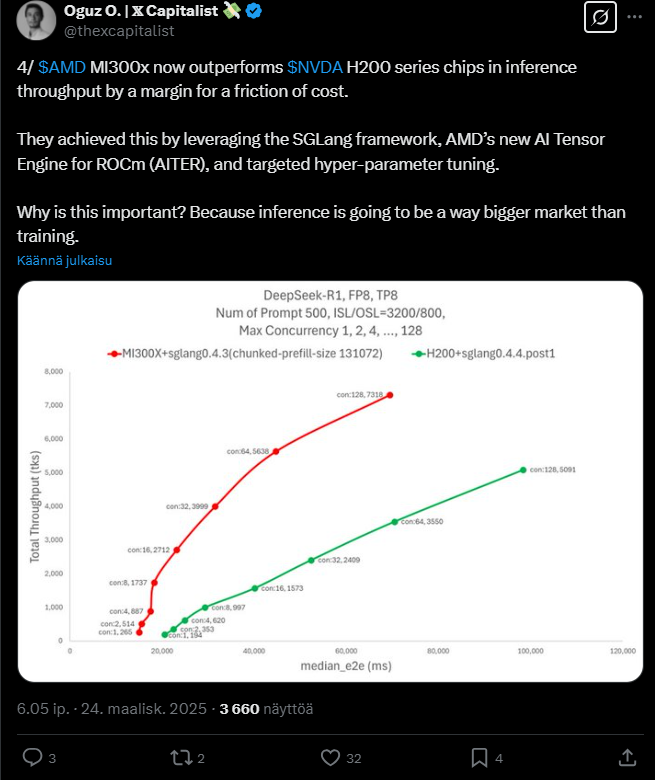

AMD’s MI300x boards outperform NVDA’s H200 series more cost-effectively, and the company is increasing its market share in data centers.

A great win indeed for AMD’s MI300X vs Nvidia’s H200, even though the market doesn’t quite seem to believe it yet.

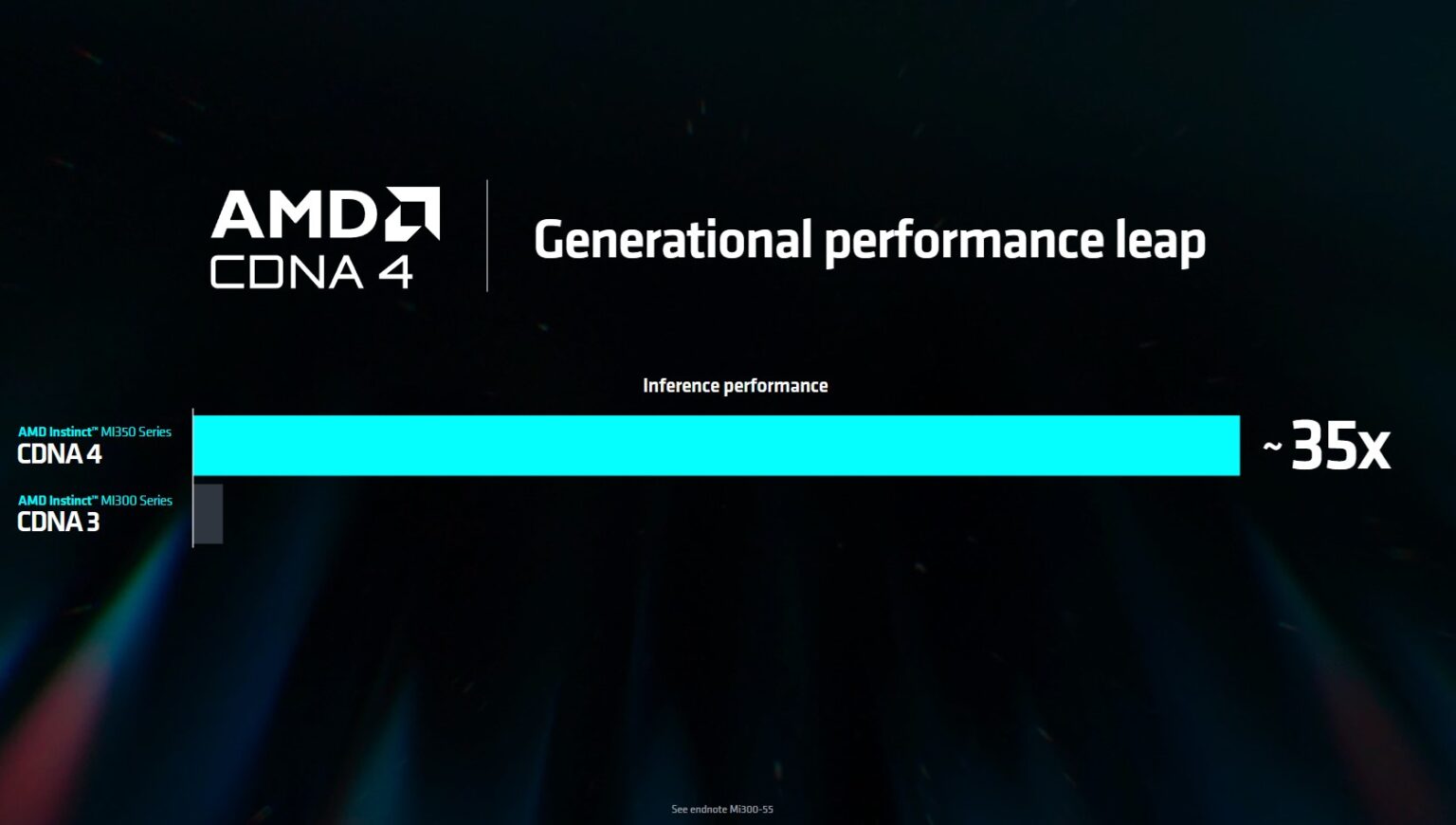

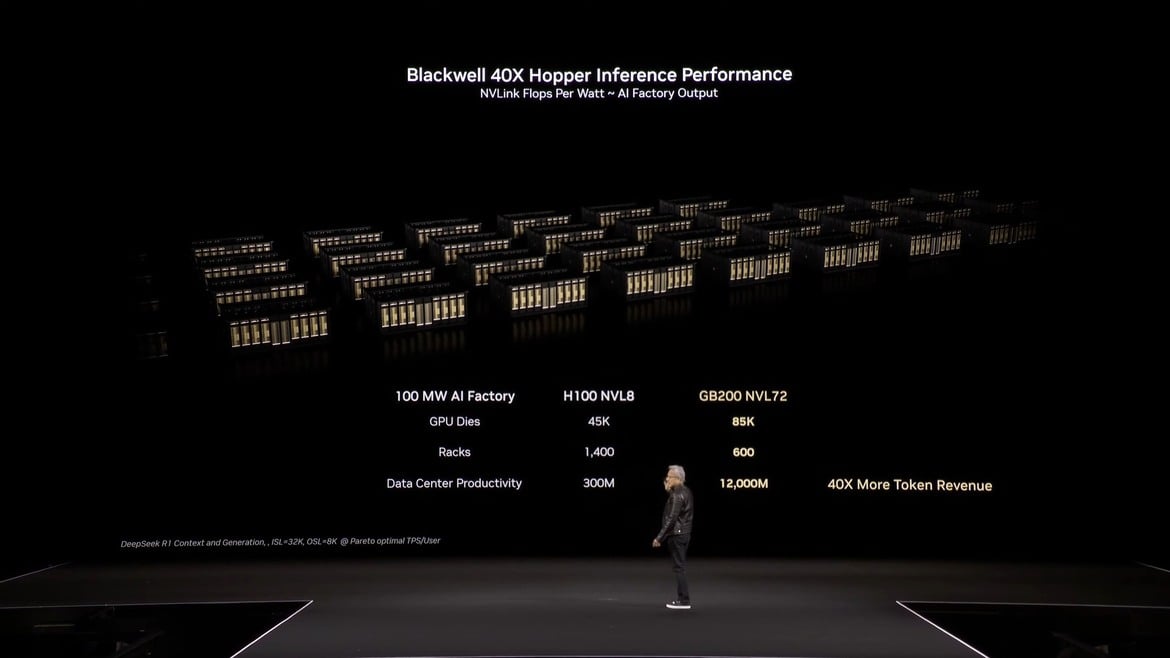

It will be interesting to see what the difference is with this year’s newest chips, MI350 vs B200. Both companies seem to be saying that the next chip is much better.

AMD stated at last year’s Computex fair that the CDNA 4 chipset is up to 35 times more powerful than the previous CDNA 3.

Nvidia again stated at last week’s GTC event that the Blackwell series is 40 times more performant than Hopper.

Intel announced on Thursday that three board members, namely Omar Ishrak, former CEO of Medtronic, physician and philanthropist Risa Lavizzo-Mourey, and Tsu-Jae King Liu, dean of the College of Engineering at the University of California, will not stand for re-election in May.

The change is related to Intel’s leadership change, where Lip-Bu Tan replaced Pat Gelsinger as CEO. Intel’s stock price has fallen by nearly 50 percent over the past year.

Does anyone have any idea if the customs exemption applies more broadly to various semiconductor products, or if it’s just an exception targeting AI chips? I understood that at least Nvidia’s and AMD’s products are currently protected from customs duties, but what about Micron’s memory solutions or other components for IoT devices?