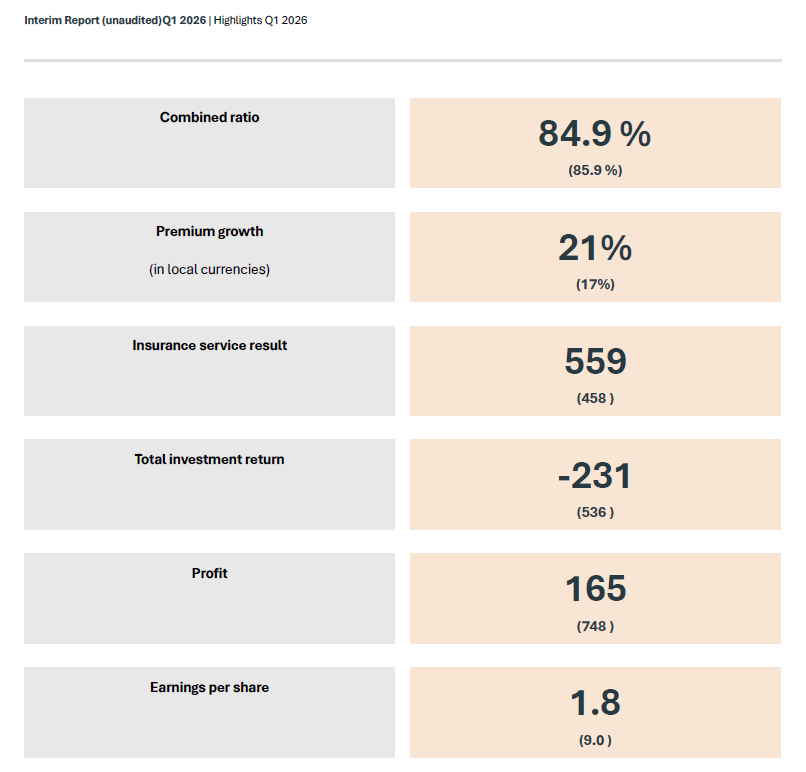

The essential part is under the interim report: the underwriting result and growth are rocking - investment returns are stalling.

- In investment returns, equities -7.2% and bonds +0.1%

In bonds, rising interest rates lowered paper values, but the yield rose slightly (5.1% => 5.3%) while the risk level was reduced (high yield bonds down by 15.5%)

In bonds, rising interest rates lowered paper values, but the yield rose slightly (5.1% => 5.3%) while the risk level was reduced (high yield bonds down by 15.5%) - Solvency requirements decreased due to the reduction in the investment risk level, so Prote paid an exceptionally large quarterly dividend of 8 NOK despite the strong growth.

- Renewal rate 93%

- Growth is stalling in the UK Growth was only 5% in the key insurance policies starting on April 1st, due to lower quoting activity and a lower hit rate. However, the renewal rate was over 100% in public entities and real estate.

- UK profitability is diamond-grade - CR a measly 77%

- Half of the 21% growth came from France, where growth was 172%

- Surprisingly, 19% growth in Norway as well

- France already reached a clearly positive result (CR 91.7%) even though it has only been in the market for 1.5 years!!! Of course, it’s still very early days and as I’ve mentioned before, they took a hit in Denmark after the first good years when pricing had been too aggressive.

- A lower reinsurance rate was reflected in 1.8 percentage points lower reinsurance costs. This should manifest as higher volatility in the loss ratio, but this quarter large claims were exceptionally low (1.7% of premiums, compared to an average of 6%).

Excellent performance is being drowned out by poor investment returns. In my opinion, this is starting to look like a good spot to add more to the portfolio.