Any experiences with Private Banking services focusing on real estate investing? The standard Private Banking model focuses on financial assets, and to access the service, one needs to have a sufficiently large portfolio. However, many services nowadays advertise Private Banking as comprehensive, covering all asset classes. I’m asking this from the perspective that things are stalling with my current loan officer, and I’m wondering if the service would improve for real estate investment loans if the contact person were from the Private Banking side.

At Danske Private Bank, the drawdown of investment property loans has proceeded smoothly, and for example, various interest rate hedging options have been flexibly reviewed when needed. Some of the loans are in my own name, some through a limited company.

Contact persons have also changed there occasionally (in which bank haven’t they?), but service has always been received quickly enough. Sometimes answers have come directly from the management level, where they seem to be very well informed about things.

So, all in all, professional service in my opinion. Of course, it makes me wonder a bit that once you become more ‘married’ to the bank in question, will they slowly start to creep interest rate offers upwards from the original introductory levels.

EDIT: And let me also mention that if handling something has taken too long in another department at Danske, our own contact person has certainly stood up for us and got things moving.

4 Likes

Today I started using Nordnet’s Private Bank “services”. Trading prices are okay, the limit is a good product, but the interest rate is mediocre. The PB page has nothing useful. Customer service responds quickly, which is a plus. So I agree with previous messages that it’s just about cheaper trading prices, that’s it.

As a nuance to the discussion, my main client relationship has been with Lauttasaari Savings Bank’s Private Banking since May. There, the threshold is smaller than the “normal” 500k, but I don’t remember exactly how much. Really good service, home loans, company loans and investments quickly through the same person, with direct contact via message or call.

I had never even considered Savings Bank as an option, well, due to historical traumas, but the trading costs are the same as with Nordnet’s Private Banking, I get quite reasonable sparring (guidance) at least for domestic stocks, and all dealings are much easier than they were with Nordea. Perhaps it depends on the contact person; generally, in my previous experiences, the “Private Banker” title hasn’t brought much expertise regarding investing… Here I got a quite reasonable bond portfolio and there were no complaints about me managing the equity side myself. Oh, and the Private Banking fee is just a fixed grand (thousand) per year, meaning they don’t take a percentage fee from AUM (Assets Under Management), unlike competitors.

3 Likes

Are there any recent experiences with that OP service?

It probably could work, but the company’s antique trading application annoys me every time I use it. Also, since I’m used to using Nordnet, where potential limits and trading work excellently, the barrier to switching is quite high.

Just came to my mind regarding Nordnet’s new upcoming PB (update): will they somehow take into account if the main portfolio has, say, 200k, and other family portfolios (i.e., portfolios under the main portfolio) bring the total sum across all portfolios to between 500-700k? Into which “privilege class” will the owner of the main portfolio then be placed in the new PB?

There’s been a rumor that PB benefits could be tied to the total sum of portfolios? Or maybe it’s just a rumor without any basis in truth. =)

About what new Nordnet PB? Link to the topic?

3 Likes

More on the topic from here:

I’m considering switching from my own stock picking → wealth management. Does anyone have experience with Index, UnitedBankers’ “UB360” or Mandatum’s “Mandaatti” wealth management solutions? At least UB offers it at an attractive price. The sum to be invested would be around 200k€. I’ve also heard Evli, CapMan, and SEB are good. Broad diversification, a good investment team, and low costs are of interest ![]() If one were to switch from own stock picking to wealth management.

If one were to switch from own stock picking to wealth management.

On the other hand, it feels like all indices are so high right now that I wouldn’t want to put a large sum of money in all at once…

From the perspective of wealth management or private banking, that amount is so small that you’ll practically get the same service as someone investing 2,000 euros. You’ll achieve at least the same outcome much cheaper by investing the money yourself in an index fund.

27 Likes

Why wealth management, why not just index investing? Is there a special reason why you want to pay extra for someone else to manage your assets instead of buying an index yourself and watching contentedly as the portfolio yields with minimal costs? Clearly you are not a complete novice if you have engaged in stock picking.

I understand wealth management when talking about exceptionally large wealth, special needs, or complete lack of knowledge and unwillingness to learn. But for many, index investing is a viable and more affordable option.

19 Likes

When I researched the matter a few years ago… Wealth management for assets under a million is usually practically selecting funds on behalf of the client - at worst, only from the bank’s own selection, in which case the selection might not even be among the best on the market anyway.

At some point, something comes along that isn’t easily accessible to a private investor, but at least in my circle of friends, it seems to require a 7-figure or higher portfolio.

For this reason, I have invested either directly in stocks or in index ETFs.

2 Likes

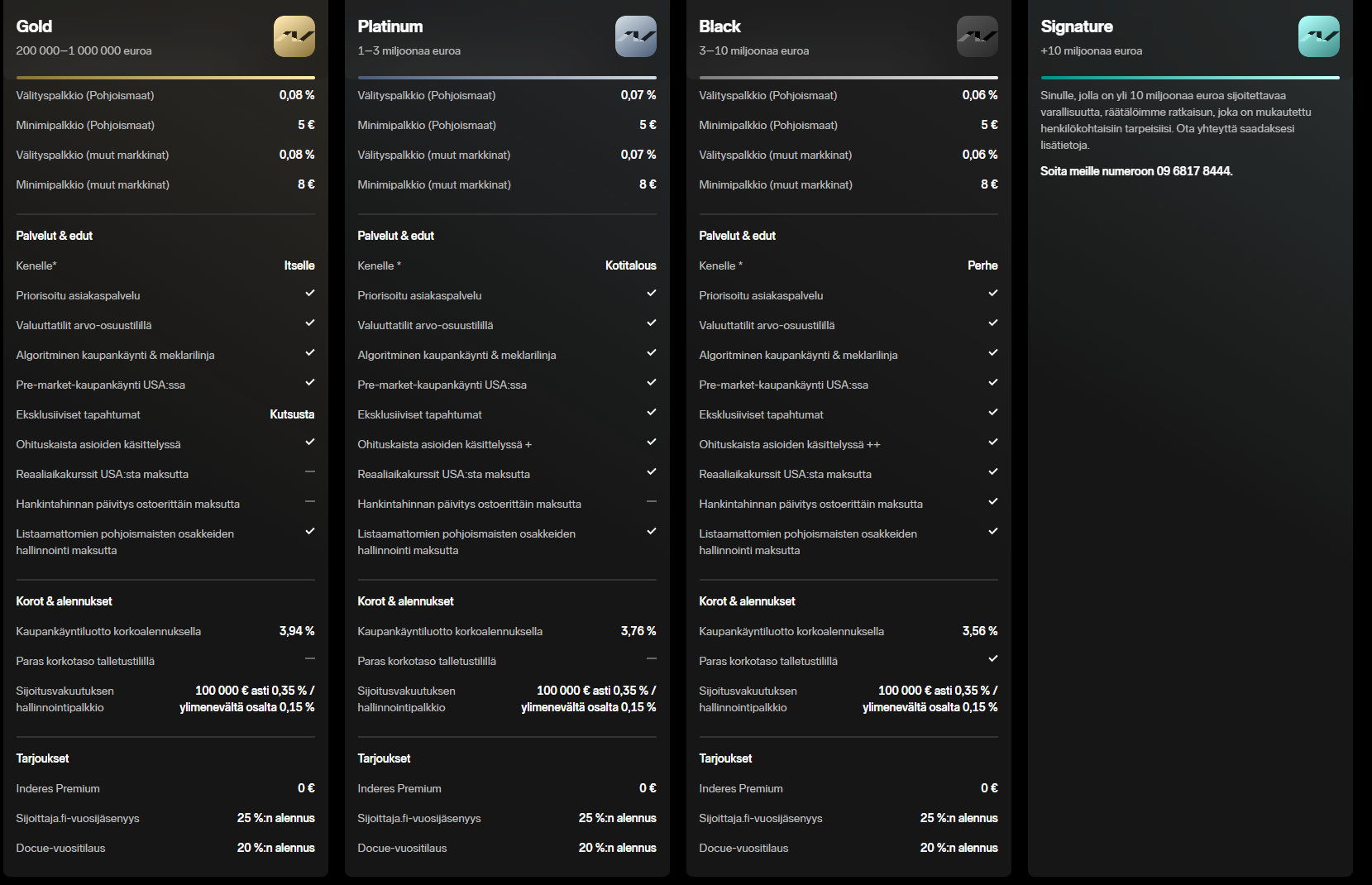

In Sweden, there are indeed tiers based on the wealth to be invested.

The Gold Club and its corresponding pricing become available when wealth > 10 MSEK, which includes the household. For 2.5 - 10 MSEK, it’s based on the ‘du själv’ principle and traditional terms. At today’s exchange rate, 10.9 MSEK is approximately 920 KEUR.

Below is the next level from the gold tier, i.e., the platinum tier. One can say that it is considerably more affordable than ‘Gold’.

EDIT: It seems there’s a drawback here: other portfolios of the same household (child) dropped out of the more favorable pricing.

7 Likes

Private Banking’s interest rate indeed dropped today at Nordnet to the current gold loan level (3.94%), but I have mixed feelings about the reform since the tiered levels are practically impossible to reach (the first step up from the basic level requires 1M, proper benefits and a clearly lower interest rate only at the 10M level) and the terms and conditions have subtly included “Private Banking level customers will also not be able to activate the Superloan feature in the future.” Especially the latter bothers me.

Previously, the Superloan interest rate was significantly lower for a long time, even at the silver level, than this Private Banking rate, and it was possible to move between levels. I guess the Superloan interest rate will also come down soon after, and then one can ponder whether to give up Private Banking if the difference in interest rates is significantly favorable to the Superloan.

6 Likes

I bet that gold-tier interest rate and Superloan are the same thing. If the Superloan rate drops, so does the gold-tier rate. Otherwise, it makes no sense.

//

The loan interest rate dropped to 3.94% and you can no longer share your account benefits with family members. These are probably the two things I spotted. Of course, one shouldn’t forget the most important thing, which is the gold-plated theme in the app.

3 Likes

I quickly looked at this new, tiered model from Nordnet and didn’t quickly notice that anything had changed for me (I’m on the lowest tier). Did I miss something essential, or does this continue as before (i.e., is there a catch here?)

I still find it a bit questionable that Nordnet’s pricing is discussed in this thread just because the name of the pricing tier happens to be “Private Banking”. In my opinion, the pricing tier doesn’t make the service Private Banking even if it’s named as such. On the other hand, the thread starter specifically meant Nordnet.

The new Signature tier, however, could to some extent meet the definition of Private Banking, as it involves tailoring the service to the client. For other tiers, it’s about the same kind of customer level as other tiers. Meaning you get a certain commission, certain interest rates, and so on. Plus a few extra services. No customization, no personal advice, no wealth management. So it’s not a so-called private bank/private banking service, and the name doesn’t make it one.

I quickly looked at this new, tiered model from Nordnet and didn’t immediately notice anything had changed for me (I’m on the lowest tier). Did I miss something essential, or does this continue as before (i.e., is there a catch)?

A weakening, at least for family members, meaning the Gold tier is only for the customer themselves. But otherwise, it seems to be similar.

16 Likes

It does make sense from Nordnet’s perspective if people don’t easily switch to a cheaper interest rate, for example, if a situation arises where the gold loan is 3%, the silver loan is 4%, and private banking is 3.94%, and the portfolio’s leverage varies between the gold and silver loan.

It’s certainly unfortunate and a worsening from the user’s perspective at that point. Previously, one could change the interest rate tier by messaging customer service (and many also had an agreed upon / customized interest rate level possibly in use).

From Nordnet’s perspective, perhaps so, if one thinks that it wouldn’t drive people away, or at least reduce the use of leverage. It’s too clear a deterioration for customers for professionals to implement it like that. But we’ll see how it works over time.

Those agreed and customized solutions are probably still in effect, but this is also just speculation.

An interesting update from Nordnet. At least at a quick glance, because the interest rate for the first tier of Superluotto (Super Loan) and Private Bank is practically the same. However, Superluotto has conditions regarding portfolio allocation and the amount of leverage. Now these are no longer required for PB’s interest rate tiers, and leverage can be used freely, with the benefit increasing according to the tiers. If this is indeed the case, then my own investment diversification to other brokers will significantly decrease.

Then one can, of course, complain about the huge difference in PB price lists between Sweden and Finland, and especially at these higher tiers, the differences are really significant.

On the other hand, Nordnet is a business, and since there is practically no real competition for private individuals’ money in Finland, this is the result. Competition is also unlikely to emerge in the future, because this small nation, taxed into destitution, is of no interest to any foreign company.

23 Likes