Plejd released its full-year 2025 figures today: Year-end report

Looking quite good!

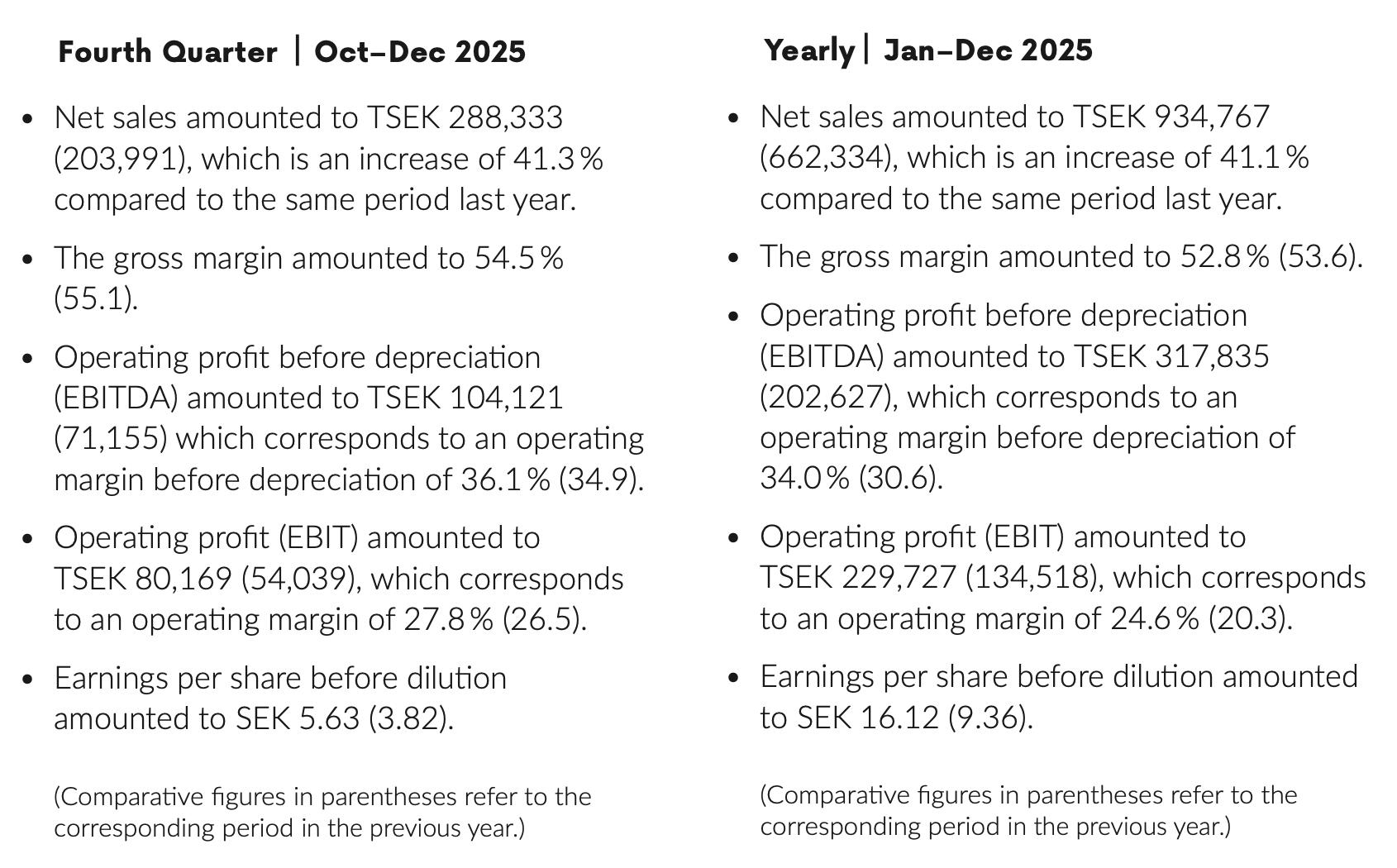

41% organic growth in sales (both full year and Q4).

Strong earnings growth continued, and profitability also improved. Full-year EBIT grew by 71%, the annual operating margin was 24.6% (2024: 20.3%), and EPS grew by 72%.

TRM-01 thermostat as a breakthrough product, especially in Norway.

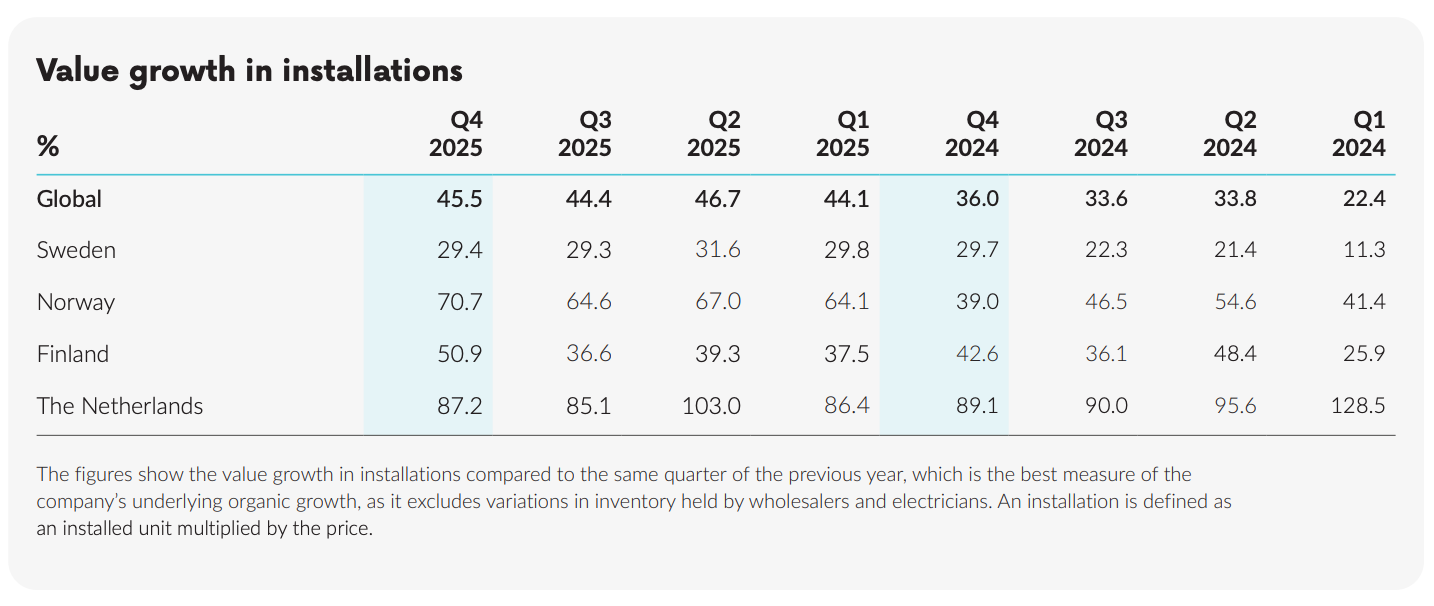

According to the “Value growth in installations” metric, the strongest growth in Q4 was in the Netherlands and Norway, but growth also accelerated in Finland.

Plejd once again surprised the market positively with its Q1 report.

Quick highlights:

EBIT increased by 87% y/y (33% q/q), driven by a higher gross margin (56% vs 52%). The main reasons for its improvement were “optimizations of our most installed product, the downlight DWN-01” and “increased share of in-house production in our own factory”.

At the end of the quarter, a new LED panel was launched: LPN-01, “our first luminaire aimed exclusively at commercial installations”. Deliveries will begin and production will be ramped up in Q2.

The transfer to the main list of the Stockholm Stock Exchange was planned for the end of 2026, but the schedule has been delayed to the latter half of 2027, with the reasoning “we have chosen to prioritize operational execution”.

First quarter │ Jan–March 2026

Net sales amounted to TSEK 307,876 (220,383), which is an increase of 39.7%

compared to the same period last year.

The gross margin amounted to 55.8% (51.6).

Operating profit before depreciation (EBITDA) amounted to TSEK 132,282 (77,140), which corresponds to an operating margin before depreciation of 43.0 % (35.0).

Operating profit (EBIT) amounted to TSEK 106,767 (57,100), which corresponds to

an operating margin of 34.7% (25.9).

Earnings per share before dilution amounted to SEK 7.51 (4.02).

Pareto Securities says that the Q1 report crushed expectations and significant forecast upgrades are expected. Plejd’s share price at the time of writing is approximately +13% (SEK 971), and it appears to have reached a new intraday ATH of SEK 1000.

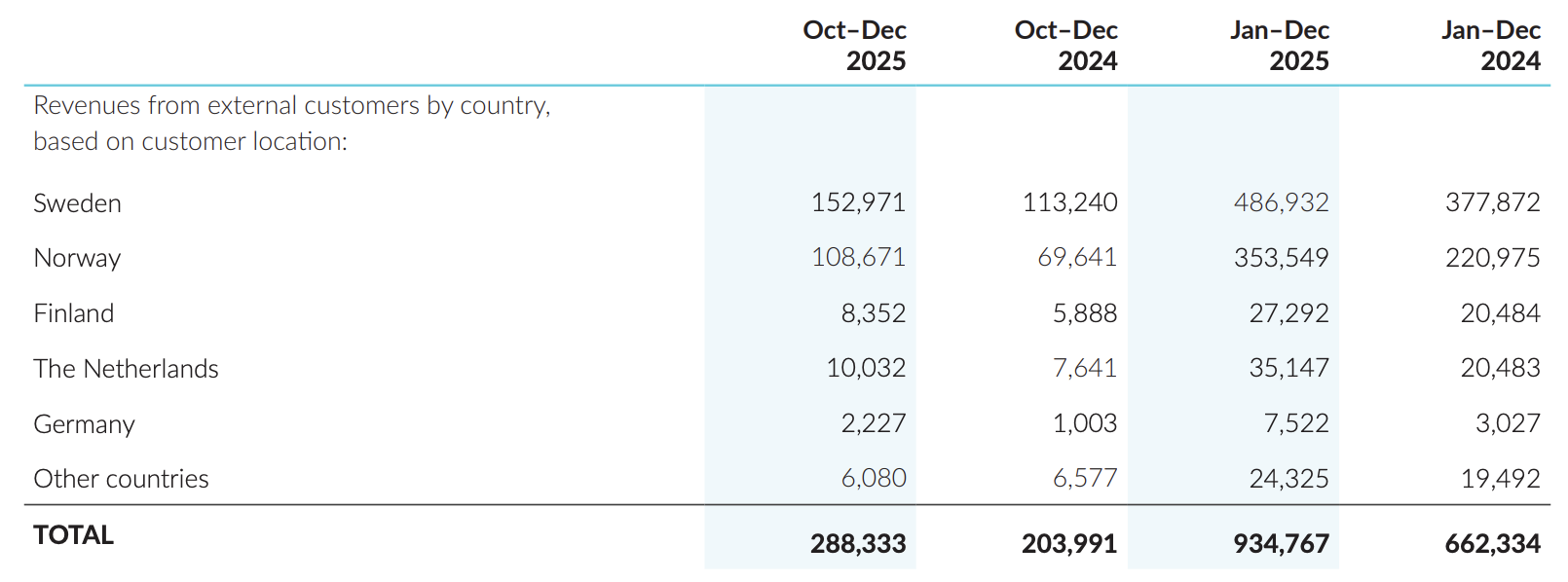

The Netherlands and Norway continue to be the fastest-growing markets:

From within the lighting industry, I have to say that selling that LED panel wasn’t made easy at all. LED lighting happens to be the most competitive product. Huge amounts of it are sold annually, but the profit margin for each project remains low. At least, that’s the situation in Finland.

Even if Plejd control systems were used in the project, it’s still extremely difficult to get the panels into the project.

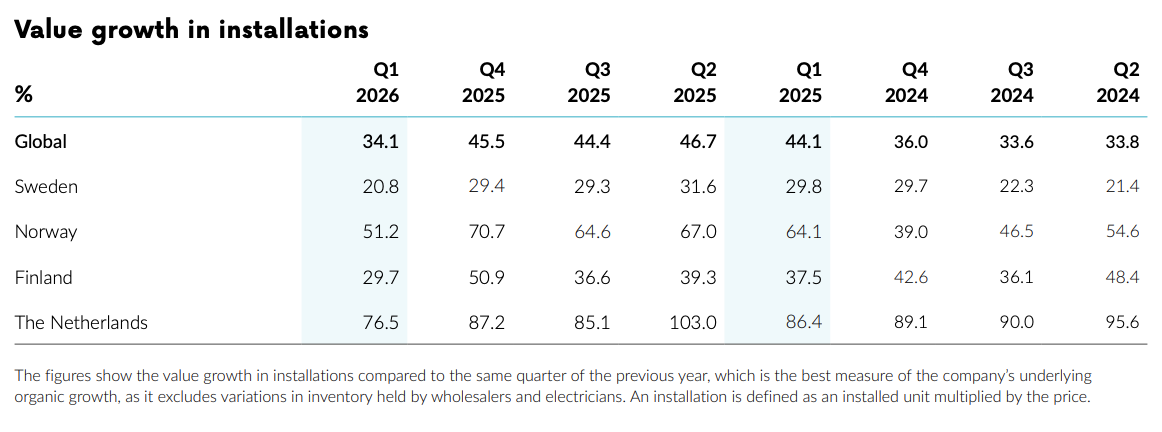

Tough report. Norway caught up with Sweden in revenue and growth in the Netherlands looks incredibly good. Babak probably wasn’t talking for nothing when he said the thermostat is an anticipated product in Norway.

I don’t know the market for that panel in detail, but I would assume that Plejd’s panel’s target market is not large properties with extensive building automation solutions, but rather smaller spaces. In these cases, the decision is influenced by the installation company, to whom Plejd is already a familiar and trusted brand.

The challenge with those is that there are fewer smaller properties that are being lit with panels here. I believe the aim is also to seek larger projects. So the project size doesn’t have to be school-sized for the competition to be tough.

The “Fair value range” is 700 (bear) – 1840 (bull), with a base case of 1220 SEK.

More detailed information is not available for free. This appears to be user-paid (not company-paid) analysis.

Redeye initiates coverage of Plejd, a Swedish smart home company that has built a dominant position in the Nordic market by placing the professional electrician at the centre of its strategy. Having grown into the default standard for smart lighting control in Sweden and Norway through an exclusive wholesaler channel model, the company is now expanding its product portfolio into heat management, commercial LED-panels, and solar shading while rolling out the proven playbook across Europe. We view its electrician-first model, deep channel loyalty, and a world-class management as key enablers of sustained high double-digit growth.