Pitch #4: UBER TECHNOLOGIES

How about a rapidly growing mega-tech company with a dividend stock valuation? This company isn’t completely unknown, but it’s not a crowd favorite either. Sentiment around the company isn’t at its brightest, but to my taste, it has strong growth drivers. Even the legendary Bill Ackman trusts Uber and has bet a couple of billions on the company.

For those on the forum who might not know, Uber is known for its platform that connects drivers and customers for mobility and delivery services. Uber is best known as a ride-hailing service (approx. 51% of revenue), but today, Uber Eats (approx. 46% of revenue), i.e., food delivery services, is also a significant platform. Additionally, the portfolio includes Uber Freight (approx. 3% of revenue), which is freight brokerage. Uber does not own cars or employ drivers itself; its operation is purely platform economy.

Uber’s business benefits from significant megatrends such as urbanization, digitalization, and the development of artificial intelligence and data analytics. The concentration of population in cities creates a platform for operators like Uber, as the service operates most cost-effectively in large cities. Uber primarily simplifies the lives of busy people in large cities, and one can personally observe in large cities that the service is becoming very smooth (rides are quick to get and payment is convenient) and affordable (the price of a single ride is starting to challenge public transport fares). With the help of AI and data analytics, Uber can optimize routes, pricing, and the matching of drivers and customers better than before. These trends provide a nice underlying current for the business.

Uber’s market potential is enormous. According to various sources, the global taxi and ride-hailing service market is projected to grow at an annual rate of approximately 9-11% in the coming years as urbanization progresses and consumers shift from owning cars to using services. Platform services like Uber are growing faster than this, as traditional taxis lose market share. In the food delivery sector, the market size is estimated to be between 200-250 billion dollars according to various estimates, with a growth rate of approximately 10% per year for the next five years or so. Urbanization, ease of service, and a growing middle class are accelerating market growth. Uber offers everyday convenience to busy city dwellers!

Why will Uber then win these growth markets? Because Uber is already the undisputed market leader; in its most important market, the United States, Uber’s market share in ride-hailing services is approximately 76%. Uber has 180 million monthly active users, a 15 percent increase from a year ago! I believe that in platform services, the winner eventually takes all: Market leadership is a competitive advantage that cannot be copied. The market leader’s brand is the most recognized, its app is already in most pockets, it has the most drivers in the city (meaning a driver is likely nearby and ready to pick you or your food up immediately), and additionally, the market leader’s fixed costs are relatively the lowest. Being the market leader is also beneficial for drivers: The market leader can offer you more customers, and a customer is more likely to be found wherever you happen to be. Uber thus benefits from significant network effects: More drivers, more customers, better service.

Uber is constantly developing its service. One example is the Uber One membership program, which already has 36 million members (membership $9.99 per month, generating approx. $4.3 billion in revenue for Uber annually). With an Uber membership, you get benefits from ride-hailing and food delivery services, which distinguishes Uber from its competitors. Due to the integration of ride-hailing, food delivery, and package services, Uber has significant cross-selling/advertising revenue potential. For example, if you order a ride to the office in the morning, the app might suggest a place where you could pick up your morning coffee. By developing this type of service, Uber can further increase user transactions through Uber in the future.

If we envision the future even further, I see that Uber has enormous opportunities ahead. Uber is already investing heavily in the development of drones and robotaxis, as well as other future visions. By 2050, the average person will no longer own a car, but will instead hail a dirt-cheap (humans disrupted out) robotaxi ride with their phone wherever they go (the service will likely be much better, cheaper, and smoother than public transport). It will no longer be worth cooking food oneself, as ordering food by drone to one’s balcony will be fast and relatively inexpensive. In the air, a food drone won’t even need to worry about traffic jams or detours; it can go directly from the restaurant to the customer. Packages will also arrive at your home by drone or robotaxi, depending on the package size, very quickly. Deliveries will no longer be handled or transported by humans at any stage; instead, AI and autonomous vehicles will take care of things. This ensures that prices are low, which further increases the popularity of services. If Uber can maintain its position as the leading platform until then, the company will be massive and present in everyone’s daily life! The company is investing heavily in these technologies, so this isn’t just my own daydreaming. The visions might sound crazy, but if these narratives dominate sentiment five years from now, the company’s attractiveness in investors’ eyes will be in a completely different league than it is today.

There are risks in this story too. The stock price has recently been pressured by fears of Elon’s robotaxis. The market seems to fear that Tesla will conquer the entire robotaxi market, leaving no crumbs for others, as rides can only be ordered through Tesla’s own app. I don’t believe this. It’s enough for Uber that at least someone else succeeds in developing a functional robotaxi, and in fact, they already have. Uber already has a partnership with Waymo, and Waymo rides can be ordered through Uber. Robotaxis are still a long way off, and in the meantime, there’s money to be made in traditional ride-hailing as well. It remains to be seen how the market will play out, but I personally believe that Tesla’s robotaxi will not be the only one when robotaxis become widespread and are globally permitted. Uber itself sees robotaxis as a great opportunity and has invested in several companies developing them. Uber is already investing heavily in the transition towards robotaxis and has made it clear that Uber does not intend to be the next Kodak or Nokia. However, the market tends to price Uber as such.

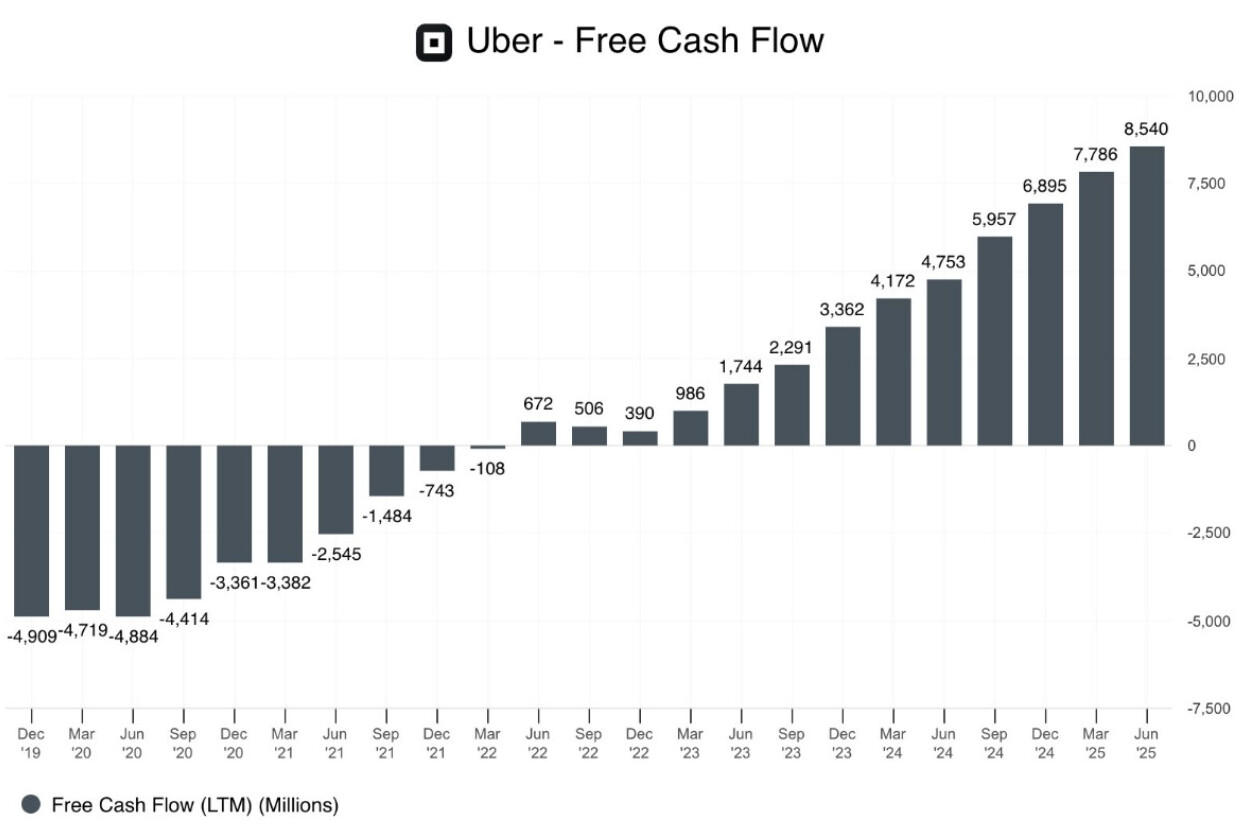

Uber’s main competitors in ride-hailing include Lyft and Bolt, and in food delivery, Doordash. Uber is the only one of these that is profitable. In addition to network effects, profitability gives Uber a competitive advantage going forward; more can be invested in product development than others, and if necessary, prices can be competed with more aggressively than others. I’m not claiming that Uber will permanently destroy these competitors, but a competitive advantage exists. Here is Uber’s free cash flow development; it turned profitable already in 2022, and since then, the curve points northeast:

Growth has been strong:

The company’s market capitalization at the time of writing is approximately 192 billion dollars. The free cash flow for the preceding 12 months is about 8.5 billion, so the P/FCF (for the preceding 12 months) is 22.5. In my opinion, this is very reasonable considering that the company is growing by about 15% per year according to analysts’ forecasts (18% in the preceding 12 months, so the estimate is likely pessimistic). Few scalable US tech companies benefiting from megatrends can be acquired at this price. In addition, Uber has announced a massive 20 billion dollar share buyback program (about 10.4% of market capitalization), which could be expected to support the share price in the future. If one trusts that the company can benefit from long-term trends and continue to grow at least at its current pace, the investment opportunity is very interesting. If the company can convince the markets that it can be a leading platform also in the era of robotaxis and drones, the valuation will be in completely different spheres; in this scenario, today’s prices will be remembered with nostalgia.

The company’s market capitalization at the time of writing is approximately 192 billion dollars. The free cash flow for the preceding 12 months is about 8.5 billion, so the P/FCF (for the preceding 12 months) is 22.5. In my opinion, this is very reasonable considering that the company is growing by about 15% per year according to analysts’ forecasts (18% in the preceding 12 months, so the estimate is likely pessimistic). Few scalable US tech companies benefiting from megatrends can be acquired at this price. In addition, Uber has announced a massive 20 billion dollar share buyback program (about 10.4% of market capitalization), which could be expected to support the share price in the future. If one trusts that the company can benefit from long-term trends and continue to grow at least at its current pace, the investment opportunity is very interesting. If the company can convince the markets that it can be a leading platform also in the era of robotaxis and drones, the valuation will be in completely different spheres; in this scenario, today’s prices will be remembered with nostalgia.

In my opinion, this story holds truly great opportunities for a long-term investor. I have seized this opportunity myself and believe that in 20 years, the company has the potential to be one of the world’s most significant companies. I recommend learning more about the company and its product!