Piipolla ei ollut vielä omaa ketjua, joten perustin sellaisen. Piippoa analysoi @Thomas_Westerholm.

Piippo on vuonna 1942 perustettu kansainvälinen sitomiseen ja kiinnittämiseen soveltuvien tuotteiden eli paalausverkkojen, köysien, lankojen ja narujen valmistamiseen sekä markkinointiin ja myyntiin keskittynyt teollisuusyhtiö. Piipon liiketoiminta jakautuu asiakkaiden mukaan kolmeen eri segmenttiin, jotka ovat Agri, Kuluttajatuotteet sekä Tuotteet kaapeliteollisuuteen. Yhtiöllä on globaali jakeluverkosto joka kattaa yli 40 maata ja sen kotipaikka on Outokumpu.

Piipon liikevaihto oli vuonna 2021 14,8 miljoonaa ja sen globaalit jakelukanavat kattavat yli 40 maata. Tärkeimpiä maita Piipolle on mm. Saksa, Puola, Australia ja USA.

Piipon H1-kasvu oli vahvaa, mutta suhteellinen kannattavuus koki poikkeuksellista painetta kohonneista valmistus- ja logistiikkakustannuksista johtuen. Vakuuttava kasvu ja markkinaosuuksien voittaminen vahvistaa mielestämme sijoitustarinan pidemmän aikavälin näkymää, minkä seurauksena suhtaudumme raportin antiin lievän myönteisesti.

Toimitusmäärät kasvoivat yhtiön päätuoteryhmissä paalausverkoissa, paalauslangassa sekä kaapeliteollisuuden tuotteissa. Kuluttaja- ja välitystuotteissa jäätiin jälkeen vertailukaudesta. Liikevaihto kasvoi selvästi päätuoteryhmien toimitusmäärien ja raaka-ainehintojen noususta johtuen, sillä myyntihinnat seuraavat raaka-aineiden hintakehitystä. Myös valuuttakurssien edullinen kehitys paransi liikevaihtoa edellistilikauteen verrattuna.

Tässä on Kauppalehden minuutissa luettava uutinen tuloksesta. Ei maksumuuria.

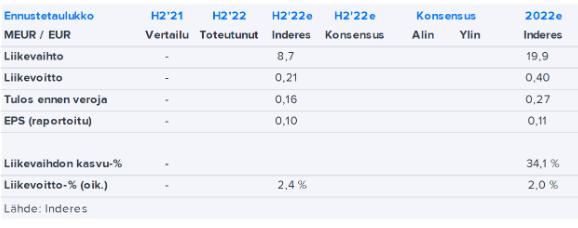

Huhti-syyskuun puolivuotiskauden liikevaihto nousi 11,2 miljoonaan euroon vertailukauden 10,3 miljoonasta eurosta.

Liiketulos nousi 0,7 miljoonaan euroon vertailukauden 0,3 miljoonasta eurosta.

Puolivuotiskauden osakekohtainen tulos parani 0,29 euroon 0,14 eurosta.

Lisään tänne vielä Thomaksen 29.11.2022 päivätyn kommentin.

Piipon H2-raportti oli odotuksiamme parempi vakuuttavan liikevaihdon kasvun ja kannattavuutta avittaneen tehokkuusparannuksen sekä merkittävien valuuttakurssivoittojen tukemana. Hyvän operatiivisen tuloksen ohella yhtiö sai rahavaroja vapautettua käyttöpääomastaan, mikä vahvisti sen taseasemaa ja laskee nähdäksemme osakkeen riskiprofiilia.

EDIT:

Lisään tähän vielä kommentin, joka on kaikkien luettavissa.

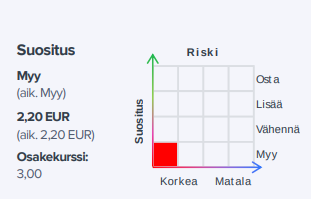

Piipon H2-raportti oli odotuksiamme parempi vakuuttavan liikevaihdon kasvun ja kannattavuutta avittaneen tehokkuusparannuksen sekä merkittävien valuuttakurssivoittojen tukemana. Hyvän operatiivisen tuloksen ohella yhtiö sai rahavaroja vapautettua käyttöpääomastaan, mikä vahvisti sen taseasemaa ja laskee nähdäksemme osakkeen riskiprofiilia. Laskeneen riskiprofiilin ja vakuuttavan kasvun seurauksena nostamme suosituksemme vähennä-tasolle (aik. myy). Toistamme 3,0 euron tavoitehintamme.

@Thomas_Westerholm on tehnyt laajan rapsan Piiposta. Laajat rapsat ovat aina kaikkien luettavissa.

Kuluva vuosi on Piipon syömähampaana toimivan Agri-segmentin kannalta jäämässä välivuodeksi, mikä korkean varastotason ja velkaisen taseen vuoksi aiheuttaa yhtiölle lyhyen aikavälin haasteita. Yhtiön on vapautettava käyttöpääomaa liiketoiminnan jatkuvuuden turvaamiseksi ja lyhyellä aikavälillä painopiste onkin tuotannon sijaan puhtaasti myynnissä. Osakkeen tulospohjainen arvostus on korkea, mikä yhdessä kohollaan olevan taseriskin kanssa johtaa mielestämme heikkoon riski/tuotto-suhteeseen.

Piippo julkaisee torstaina H2-rapsansa ja alla on Thomaksen kommentit.

Piippo julkistaa H2-raporttinsa torstaina arviomme mukaan kello 13. Marraskuun alussa annetun tulosvaroituksen ja päättyneen tilikauden ennakkotietojen myötä yhtiön heikot operatiiviset H2-luvut ovat pääpiirteiltään tiedossa, joten kiinnostuksemme kohdistuu yhtiön taseasemaan ja johdon kommentteihin yhtiön näkymiin liittyen.

Tässä on Thomaksen ennakkokommentti, kun Piippo julkaisee H1-tuloksensa torstaina.

Piippo julkistaa H1-raporttinsa torstaina arviomme mukaan kello 13. Piipon kotimarkkinaan nojaavan valmistuksen ja kansainvälisen myynnin vuoksi Suomen poliittiset lakot osuivat yhtiöön erityisen rajusti, minkä odotamme lykänneen toimituksia juuri agrikauden alussa tilikauden ensimmäiseltä puoliskolta jälkimmäiselle. Kuluvana vuonna Piippo odottaa liikevaihdon ja liiketuloksen kasvavan heikon vertailukauden tasolta, mutta jäävän 2022 tasolta. Ennusteemme ovat ohjeistuksen kanssa linjassa, mutta ulkoisten haasteiden vuoksi odotamme ohjeistuksen nojaavan vahvasti paranevaan suoritustasoon tilikauden jälkipuoliskolla.

Tässä olisi tuore yhtiöraportti Piiposta, tekijänä Thomas Westerholm.

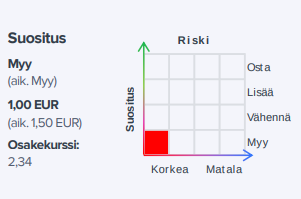

Piipon H1-luvut jäivät odotuksistamme ennakoitua heikomman liikevaihdon ajamana. Suomen satamalakot iskivät yhtiöön erityisen rajusti vientiin nojaavasta liiketoimintamallista johtuen ja yhtiön mukaan toimituksia siirtyi kuluvan tilikauden jälkipuoliskolle. Ennustealituksesta huolimatta kuluvan vuoden ohjeistus toistettiin, mikä povaa huomattavasti vahvempaa jälkipuoliskoa. Osakkeen nykyinen kurssitaso ei mielestämme hinnoittele sisään velkaiseen taseeseen ja heikkoon tuloskuntoon liittyvää riskiä, minkä seurauksena toistamme myy-suosituksemme. Säilytämme tavoitehintamme ennallaan 1,0 eurossa.

Thomakselta uusi yhtiöraportti Piiposta, jolla ei mene kovinkaan vahvasti.

Piipon päivitetty ohjeistus povaa aiempaa pienempää liikevaihtoa, mutta tekijät sen taustalla vaikuttavat ajoituksellisilta ja liiketulostason odotetaan edelleen paranevan vertailukaudesta. Teimme raportin yhteydessä negatiivisia ennustemuutoksia, mutta ne painottuivat kuluvaan vuoteen. Osakkeen nykyinen kurssitaso ei mielestämme hinnoittele sisään velkaiseen taseeseen ja heikkoon tuloskuntoon liittyviä riskejä, minkä seurauksena toistamme myy-suosituksemme. Säilytämme tavoitehintamme ennallaan 1,0 eurossa.

Tässä on Thomaksen ennakkokommentit, kun Piippo julkaisee tuloksensa torstaina päivällä.

Piippo julkistaa H2-raporttinsa torstaina arviomme mukaan kello 13. Syyskuussa annetun tulosvaroituksen ja H2-ennakkotietojen myötä tulevan raportin pääpiirteet ovat lukujen osalta jo tiedossa. Tämän seurauksena huomioimme kiinnittyy alkaneen tilikauden ohjeistukseen (huom: Piippo noudattaa kalenterivuodesta poikkeavaa tilikautta), taseasemaan ja edistysaskeliin lankatuotannon ulkoistamisessa.

Tässä on Thomakselta tuore yhtiöraportti Piiposta.

Piipon heikot H2-luvut olivat pääpirteiltään jo tiedossa syyskuussa annetun tulosvaroituksen myötä. Katsauskaudella lankatuotannon ulkoistaminen, sisäiset tehostamistoimet ja Venäjän tytäryhtiön alaskirjaus painoivat yhtiön tulostasoa, mutta hankkeet paransivat yhtiön edellytyksiä tuloskäänteen saavuttamiseksi.

Rapsasta lainattua:

Piippo on viime vuosina karsinut selvästi kulurakennettaan, minkä pitäisi luoda hyvät edellytykset kannattavuuden elpymiselle liikevaihdon kasvun myötä. Yhtiön kannalta on kuitenkin kriittistä, että tuloskäänne saavutetaan pikimmiten, velkaisen taseen aiheuttaman rahoitusriskin lieventämiseksi.

Inderes päättää Piipon seurannan yhtiön irtisanottua yhtiöseurantasopimuksemme.

Piipon sijoitustarinan keskiössä lähivuosien osalta on tuloskäänteen vieminen kunnialla maaliin velkaisen taseen aiheuttamien riskien purkamiseksi. Mielestämme yhtiö on 2024 vuoden aikana tehnyt oikeita ratkaisuja liiketoiminnan tervehdyttämiseksi, mutta niistä saatavien hyötyjen ulosmittaaminen vie aikaa.

Harva sijoittaja on muuten edes kuullut yhtiöstä, Inderesin seurannasta ja analyysistä huolimatta, joten ei yllättävää että seuranta päätettiin. Firma ei oikeastaan kuuluisi edes pörssiin vaan se pitäisi vetää yksityiseksi ja hakea sitä kautta tiukalla kädellä johtoa ohjaavaa rahoitusta kasvuun tai vaihtoehtoisesti myydä isommalle toimijalle, kun ei tuosta oikein nyt tule mitään. Onnea tulevaisuuteen Piippon jengille

Piippo Oyj on päättänyt muutosneuvottelut, jotka koskivat yhtiön paalausverkkotuotantoa, kunnossapitoa, varastotoimintoja ja tuotannon esihenkilöitä. Yhteensä muutosneuvotteluiden piiriin kuului 42 henkilöä.

Yhtiö on päättänyt sopeuttaa paalausverkkotuotannon kapasiteettia ja lomauttaa osan paalausverkkotuotannon henkilöstöstä. Lomautukset toteutetaan vaiheittain ja ne koskevat yhteensä 39 henkilöä.

Lomautukset alkavat 17.2.2025 ja ovat voimassa enintään 90 päivää. Yhtiö perustelee muutosneuvotteluiden pohjalta tehtyjä päätöksiä taloudellisilla ja tuotannollisilla syillä, sekä markkinatilanteen epävarmuudella, jotka lopulta johtivat työntekijöiden lomautuksiin.

Mielenkiintoinen tapaus, sääli että analyytikkoseuranta ei enää avaa-

Eli 6 meur tulee koneista, varaosista, tuotemerkistä.

Tällä firmasta tulee tiedotteensa mukaan nettovelaton

Jäljelle jää osakkeen omistajille (1,293 m kpl)

-Manilla Oy, joka 1,8 meur liikevaihdolla tekee nollatuloksen

-valmistuote varasto / nettokäyttöpääoma 4,2 meur

-toimitilat Outokummuissa ja Lempäälässä. Taseessa rakennukset ja rakennelmat 1,4 meur

-kuori listausta harkitsevalle

? mitähän on tapahtunut sitten 30.9.2024, ja mitä tulee tapahtumaan ennen kuin asiakassitoumukset on toimitettu? Lopputuote varastojen alemyyntiä? Toisaalta asiakassitoumuksia kerrotaan toteutettavan

-hallintokuluja, alasajokuluja ?

-korkokuluja ?

Ehkäpä joku voisi arvioida jäljelle jäävän arvon, hullulta tuntuisi esim

-Manilla Oy: 0,0 meur (ei tee rahaa)

-nettokäyttöpääoma 4,2 meur -30% alennusta ja alaskirjausta = 3,0 meur

-rakennukset 1,4 meur -30% alennusta ja alaskirjausta: 1,0 meur

-kuoriyhtiö: +1,0 meur

-alasajokuluja, hallintoa -1,0 meur

-korot -0,5 meur

=> 0+3,0+1,0+1,0-1,0-0,5 = 3,5 meur

3,5 meur/ 1,293 mkpl osaketta = 2,71 eur/osake

Em laskelma siis heittoja tehden, laskekaapa joku joka kunnolla osaa !

Suunnitellusta Kaupasta saatavat varat parantaisivat Yhtiön rahoitusasemaa merkittävästi ja Yhtiö arvioi, että Kaupasta saatavilla varoilla Yhtiö kykenee maksamaan velkansa Yhtiön päärahoittajille siten, että Yhtiö olisi Kaupan toteuttamisen jälkeen nettovelaton.

Vaikutukset Yhtiön liiketoimintaan

Suunnitellun Kaupan toteutuessa Yhtiön agrituotteiden, eli paalausverkkojen tuotanto lopetettaisiin Outokummussa. Alustavan suunnitelman mukaan Yhtiö jatkaisi tuotantoaan vuoden loppuun asti ja Yhtiö on sitoutunut täyttämään kaikki nykyiset tuotantotarpeet ja asiakkaidensa kanssa sovitut tilaukset vähintään tilikaudelle 2025 ja osin tilikaudelle 2026. Alustavan suunnitelman toteutuessa, Yhtiö tulisi varmistamaan, että tuotannon mahdollinen alasajo toteutettaisiin näiden sitoumusten mukaisesti, ja että Kaupan kohteen mahdollinen siirto Portugaliin toteutettaisiin harkitusti, jotta Yhtiö pystyisi varmistamaan asiakkaidensa odottamien korkealaatuisten tuotteiden toimittamisen.

Piipon tytäryhtiö Manilla Oy jatkaa Yhtiön kuluttajaliiketoimintaa normaalisti. Vuonna 2019 perustettu Manilla Oy maahantuo ja välittää sitomiseen, kiinnittämiseen ja nostamiseen liittyviä kuluttajatuotteita Suomessa ja lähialueilla. Manillan liikevaihto tilikaudella 2024 oli 1,8 miljoonaa euroa ja liiketulos 6 tuhatta euroa. Manilla Oy työllistää 3 henkilöä ja ostaa tarvitsemansa varastointi-, hallinto- ja toimitilapalvelut Yhtiöltä. Lisäksi Yhtiön taseeseen jää nykyinen valmistuotevarasto, Yhtiön omistamat toimitilat Outokummussa ja Lempäälässä sijaitseva kiinteistö, joita Yhtiön hallitus arvioi selvitystyössään.

Mahdollisen järjestelyn seurauksena Piipon hallitus aloittaa selvitystyön jäljelle jäävän emoyhtiön ja Manilla Oy:n tulevaisuudesta ja sen on tarkoitus päättää tulevasta strategiasta Kaupan toisen vaiheen toteuttamiseen mennessä. Hallitus arvioi mahdollisuutta jatkaa liiketoimintaa sekä muun muassa mahdollisuutta myydä jäljellä oleva liiketoiminta tai Yhtiön koko osakekanta niin sanottua käänteistä listautumista suunnittelevalle Yhtiölle.

Yhtiön nettokäyttöpääoma 30.9.2024 oli 4 155 tuhatta euroa.

@Thomas_Westerholm tämähän on ollut seurannassi vielä hetki sitten, ehkäpä voisit verestää muistoja ja arvioida mitä tämä päivän uutinen toteutuessaan tarkoittaisi?

Toteutuessaan tämä olisi mielestäni oikein hyvä asia Piipon ja yhtiön osakkeenomistajien kannalta. Merkittävän velan, rikkoutuneiden kovenanttien ja kiristyneen kilpailuympäristön myötä liiketoiminnan kääntäminen omin neuvoin olisi ollut erittäin haastavaa. Nyt saadaan tase nettovelattomaksi ja pidetään samalla kiinni tietyistä omaisuuseristä ja Manillan liiketoiminnasta. Lisäksi jää myös sauma myydä jäljelle jäävä liiketoiminta.

Nopealla vilkaisulla tämä hahmotelma vaikuttaa omaan silmään oikein järkevältä. Hyvässä lykyssä Manillalle löytyisi ostaja ja Outokummun rakennukset saisi myytyä parempaan hintaan. Vastapainona toki riski, että strategiset hankkeet venyvät odotettua pidempään aiheuttaen kuluja (listayhtiön kulut jäisivät yksin Manillan harteilla) ja menetettyä aika-arvoa. AktiiviOmistajilla ei välttämättä ole kuitenkaan heti uutta yhtiötä listattavaksi. Olen itse kaupan puolesta, mutta erikoistilanteen jätän sijoittajana pelaamatta (oma kokemus on, että suhtaudun yleensä turhan optimistisesti osien summan purkautumiseen).