Revenue: 145 mEUR (2021E)

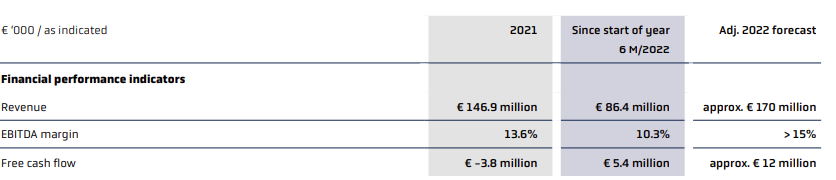

EBITDA %: 12-15 (2021E)

Free Cash Flow: 10-12 m€ (2021E)

Market Cap: approx. 50 m€

Website: https://ir.paragon.ag/websites/paragon/English/0/investor-relations.html

Latest presentation (in English): https://ir.paragon.ag/download/companies/paragon/Presentations/20201116-18_PGN_Eigenkapitalforum_WEB.PDF

Some key figures (current year, based on company guidance):

EV/EBITDA: approx. 3

EV/SALES: 0.35

A Preamble

Once upon a time in Germany, there was an automotive supplier, a family business, that listed a large portion of its promising battery technology company on the stock exchange. With the funding received, the supplier implemented an ambitious growth program, making acquisitions and investing in manufacturing capacity and technology development.

The company proudly stated that one in seven cars sold worldwide contained technology it manufactured. In 2019, investments amounted to nearly 30 m€. In its hunger for growth, it also took out a franc bond from Switzerland. Big expectations were set for 2020.

But alas, the growth promises in the battery technology sector of its subsidiary did not materialize on time as an important customer delayed large purchases. Write-downs had to be made, and these were consolidated on the parent company’s side, marring the figures.

Then the terrible corona hit. Our main supplier to the German automotive industry (especially the VAG Group) found its cash flow under severe pressure. Costs ran high, but car factories were closed for several weeks. The previous year’s annual report included a note about the risk of liquidation if the difficult corona situation prolonged.

The equity ratio in Q3/2020 was only 6%, while the company’s target was 30%. An analyst’s target price of approximately 90€ was now a distant dream, and the share price plummeted below 10 euros. Just ten years earlier, the company had had to renegotiate its debts for the last time. Now, large write-downs were made, extended payment terms for purchase invoices were negotiated, and bond covenants were relaxed…

A gruesome true story, especially if Paragon Ag has been in your portfolio for several years! My condolences to the holders. Asbestos gloves have come in handy.

Yes, why don’t you recommend Argentine government bonds? Tell me more anyway.

Paragon Ag is thus a supplier to the (mainly) German automotive industry. Below is a list of its offerings, which can be considered quite extensive.

In 2020, over 20% of the company’s employees were involved in product development. The focus on product development suggests that the company is seeking a first-mover advantage, thereby avoiding competitive pressure and price erosion in more established products.

The core business is healthy, and for a long-term investor who accepts risks (see separate section), the target is therefore attractive. The second image shows the revenue distribution for 9 months/2020 by region. There are three equally strong pillars, and Digital Assistance is the most recent investment in software and AI. As can be seen, the share of software is rising steeply (48.7% y-o-y).

From good things to bad. The most significant reason for the low valuation is the extremely weak balance sheet structure and indebtedness. The balance sheet cannot withstand – without a share issue or other forced solution – a new shock like the corona pandemic.

Addressing the balance sheet problem is a key driver for a significant rise in share price and creation of shareholder value. Therefore, this post focuses more on opening up risks than on the business. Perhaps more on the business will follow later.

So how are these messes cleaned up?

In bullet points:

-

Cost-cutting program: Operations in Germany are being centralized as overlapping functions from acquisitions are eliminated and locations merged. This work has already begun. Sale of surplus corporate properties.

-

Business growth: As the corona risk subsides, the benefits from investments made will finally be realized. Demand for software, sensor, and cabin air purification technology has been stronger than anticipated. In software, voice control is a rapidly growing area. The free cash flow forecasted for this year is strong. In software, Paragon sells a license-based platform solution that generates continuous revenue.

-

Voltabox sale: The company has stated its intention to sell its publicly listed battery technology subsidiary, Voltabox, entirely. The market value of its stake (54.5%) is approximately 40 m€ at the time of writing.

Nice, but why should I invest my money in this?

If you deduct the Voltabox ownership from Paragon’s market capitalization, simple math would suggest the company’s value corresponds to less than one year’s free cash flow. Not bad, as a certain Dancing with the Stars judge would say. The 2019 annual report mentioned an order backlog of approximately 800 mEUR for the next 60 months. A basic workload for the coming years exists.

The EV/EBITDA and EV/SALES figures mentioned in the initial info box for this year scream cheapness. Larger competitors/peers have EV/EBITDA multiples hovering between 5-6, so a 50% increase in share price would leave the multiple at approximately 4.5, which could be an acceptable level if and when the company gets its debt situation even slightly more in order.

(Note! I have not calculated pro forma figures for if and when a partial Voltabox divestment occurs, so these key figures come with that caveat.)

The company appears to be unpopular, which greatly pleases a hunter of even somewhat cooled cigarette butts like me. The general corona bubble has not managed to inflate the stock’s valuation.

So what are the monsters then?

As one might expect, reality is more complex. The sale of Voltabox ownership is intended to be made to an industrial player in larger blocks. The sale was supposed to happen last year, but negotiations with a Swiss buyer candidate have continued. The extended timeline for the sale could mean good things (not a forced sale situation, seeking better terms) or bad things (the target to be acquired is unsatisfactory).

I lean towards the positive side. As the cash situation improves, Paragon does not need to give away assets to pay off debts. The company’s situation is comparable to NoHo, which ran into corona and only recently sold its Eezy ownership. (Unlike NoHo, Paragon is already generating positive cash flow.)

A block sale of Voltabox ownership may fetch a price lower than the market price, even if it is done in several parts. If the sale is not finalized during the current quarter, it is unlikely to materialize with the current Swiss buyer candidate at all. Voltabox’s cash situation has also been tight, so in a bad scenario (battery sales do not recover), Voltabox ownership will be diluted, and Paragon’s creditors will become nervous. This risk must definitely be considered, as the deal has been negotiated for almost a year now.

If the sale does not happen, there is a risk of a share issue and/or the sale of a company division. Both actions would destroy shareholder value and be reflected in the share price. Therefore, the Voltabox sale is the primary way to reduce the debt-to-equity ratio, either through a block trade or by selling to the market in small increments.

Paragon is largely dependent on the success of the VAG Group. Although the market has opened up to China (e.g., Geely), the company is still a captive of the German automotive industry’s success. This dependence is mitigated by a broad product repertoire and a focus on more niche areas and software where growth prospects remain good.

Problems with chip orders plaguing car manufacturers may slow customer sales, at least in the short term. Germany, however, has boosted its domestic market for new cars, maintaining demand for Paragon’s offerings.

Finally, I will address management. Family entrepreneurship is often mentioned in a positive light, but founder Klaus Frers, who holds power with a 50%+1 voting share, is in a significant position to decide the company’s direction.

OK, is this a buy or a sell?

I will outline an optimistic scenario below, but not, in my opinion, with overly bullish glasses. This can, of course, be freely challenged, as it contains a big V-shaped assumption:- The Voltabox sale will go through. Paragon will remain a minority owner, committing to sell its stake (~10-15%) later. The money will be used to pay off debts and redeem below-par bonds. Equity ratio will significantly improve, and risk level will decrease.

- Sales will grow by 10-15% over the next couple of years, but no dividends will be paid for a couple of years, as debt – mainly bonds – repayment will continue. This is fine with me.

The actions taken should be reflected in the share price. Unless otherwise agreed in connection with the Voltabox sale, there is also an option to benefit from Voltabox’s improved performance.

Q4/2020 will be published tomorrow, and we will get more information on how the sale of Voltabox ownership is progressing.

Disclaimer: I own Paragon shares.

Fun fact: Taalerin Mikro Rein fund has owned a couple of percent slice of Paragon, apparently still does.

Fun fact 2: I started with an analysis of Voltabox, but ended up as an owner of Paragon. Some like the mother and some like the daughter. So far, I got both.

Ed: typo corrected in the heading