The pace of news is brisk. Now, from Delbrück, the outlook for the next five years until 2027 has been outlined. In bullet points, they are:

- Revenue over EUR 300 million (currently approx. EUR 175 million)

- Focus on North American sales (sales office opened)

- Strong growth in the Power business unit’s sales in the medium term

For 2023, the targets are:

- EBITDA 12-15%

- Revenue over EUR 170 million, meaning the Semvox divestment will be compensated for

First, regarding next year’s figures. When the company’s market cap is EUR 25 million, even a rough back-of-the-envelope calculation shows the figures are contradictory. EBITDA at the upper limit would equal the entire market cap. Free cash flow is not yet known, but the figure should become clearer next year. The base assumption is EUR 10-15 million. 2023 and 2024 are still years for paying down debt, but eyes are already turning to the future.

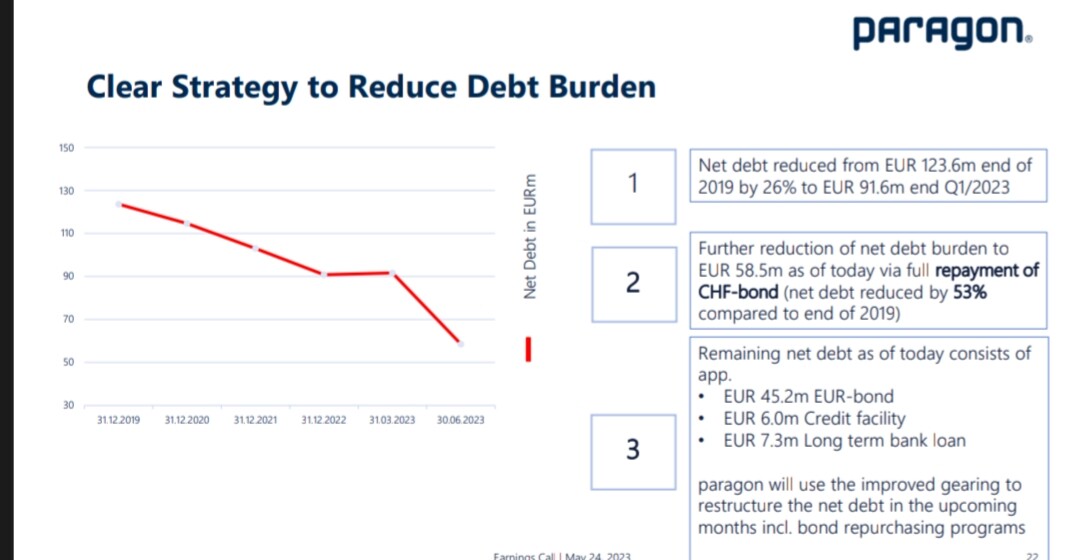

In recent years, there has been tension over whether the mountain of debt would sink the ship. Following the Semvox sale, the CHF bond redemption and potential additional Eurobond redemptions (min. EUR 5 million) will drop the debt level to approximately EUR 75 million, possibly lower. Interest expenses will not decrease in the same proportion because the Eurobond interest rate is higher than before.

Paragon will likely prioritize paying off other loans if covenants allow. Relative to inflation, the interest rate (6.5%) is not even impossible if Paragon can manage to pass increased costs into its contracts! In any case, as the risk level decreases, loans will be refinanced at lower rates.

Looking further ahead, growth in the Power unit seeks a fresh start powered by lithium-based starter batteries. Paragon acquired the technology from the portfolio of its former subsidiary Voltabox. Paragon has produced starter batteries before (starting around 2014-15), so this is not a new expansion. Investors are more interested in profitability and the amount of capital tied up than just revenue.

A CMD (Capital Markets Day) wouldn’t hurt to explain in more detail what achieving this growth requires and what the EBIT level will be in the future. Historically, the base level has been between 8-12%, but there is still a way to go.

In a bull scenario, revenue grows steadily toward the EUR 300 million target and EBITDA hovers between 15-20%. Debt does not consume the cash flow and leverage is brought under control, which should leave enough for shareholders as well. If 5-10% of revenue trickles down to the bottom line, we are talking about a result of EUR 15-30 million, roughly EUR 3-6 per share.

The figure is appetizing, but should be taken with a grain of salt. This is a back-of-the-envelope calculation and susceptible to swings in the automotive industry.

https://ir.paragon.ag/websites/paragon/English/4250/news-detail.html?newsID=2397357