Ah. Kiitos korjauksesta. Omiin silmiin tämä näyttää enemmän cost-driven hankkeelta kuin siltä että pelisarjaan oltaisiin tosissaan satsaamassa, mutta mene sitten tiedä.

2 tykkäystä

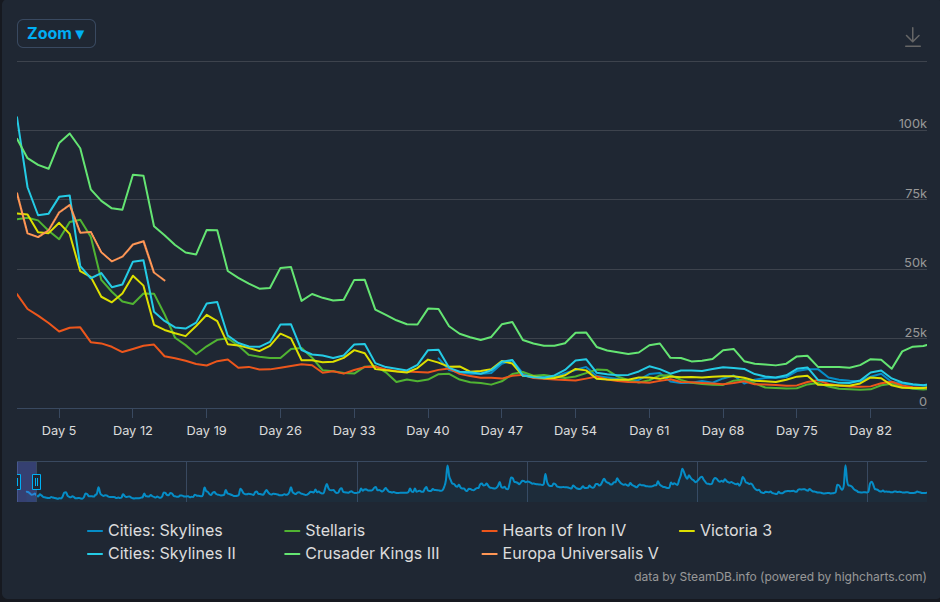

HOI 4:seen julkaistiin eilen uusin DLC, No Compromise, No Surrender.

Mitä selailin Steamin arvosteluista ja Redditistä kommentteja, niin vastaanotto oli hyvinkin kädenlämpöinen ![]() 30 euron DLC, joka vastaa siis 60% peruspelin hinnasta, ei selkeästikkään tyydyttänyt yhteisön haluja hinta/sisältö-skaalalla.

30 euron DLC, joka vastaa siis 60% peruspelin hinnasta, ei selkeästikkään tyydyttänyt yhteisön haluja hinta/sisältö-skaalalla.

Steamissa arvostelut tällä hetkellä Mixed, eikä pelaajamäärissä oikeastaan muutosta. Pitännee kuitenkin odottaa viikonloppuun, että oikea efekti näkyy.

Tämä oli sinänsä harmi, koska omissa papereissa EU 5, CK 3: AUH ja tämä DLC olivat ne “turvalliset syömähampaat”, jonka piti tuoda Paradoxille rahaa kassaan tässä kvartaalissa. Varsinkin CK 3 ja HOI 4 ovat pelaajamääriltään merkittäviä tuotteita. Bloodlines 2 ja Mars olivat omissa papereissa lähinnä…noh ![]()

Täältä voi tehdä omia johtopäätöksiä arvosteluista: Reddit

EDIT: HOI 4 on Steamissa ilmaiseksi pelattavana viikonlopun ajan, sekä -70% alessa. Todnäk vaikuttaa pelaajamääriin.

Jos jotain positiivista, niin EU 5 on Paradoxin kaikkien aikojen toisiksi paras julkaisu retention suhteen! Pelaajaluvut pysyvät ällistyttävän hyvinä.

Aikoinaan kun CK 3 julkaistiin syyskuussa, niin se myi kahdessa kuukaudessa miljoona kopiota (lähde: Paradoxin Q3 2021). Tällä tahdilla voisi arvella EU 5:n myyneen kyllä jo yli puoli miljoonaa kopiota.

Kuvaajassa näkyy Paradoxin pääpelien pelaajamäärät normalisoituna julkaisuun. Ykkösenä siis CK 3 ja toisena EU 5.

9 tykkäystä

Bloodlinesiin reipas alaskirjaus

Paradox Interactive has today decided to make a non-cash write-down of MSEK 355 of capitalised development costs for the game Vampire: The Masquerade - Bloodlines 2 in the fourth quarter. The write-down is made in addition to the quarter’s scheduled degressive amortisation of MSEK 346. At the end of the year, MSEK 40 of the capitalised development costs will remain on the balance sheet. The write-down is based on an updated sales forecast made 30 days after the game’s release.

Vampire: The Masquerade - Bloodlines 2 is a strong vampire fantasy and we are pleased with the developers’ work on the game. We’ve had high expectations for a long time, since we saw that it was a good game with a strong IP in a genre with a broad appeal. A month after release we can sadly see that sales do not match our projections, which necessitates the write-down. The responsibility lies fully with us as the publisher. The game is outside of our core areas, in hindsight it is clear that this has made it difficult for us to gauge sales. Going forward, we focus our capital to our core segments and, at the same time, we’ll evaluate how we best develop World of Darkness’ strong brand catalogue in the future, said Fredrik Wester, CEO of Paradox Interactive.

5 tykkäystä

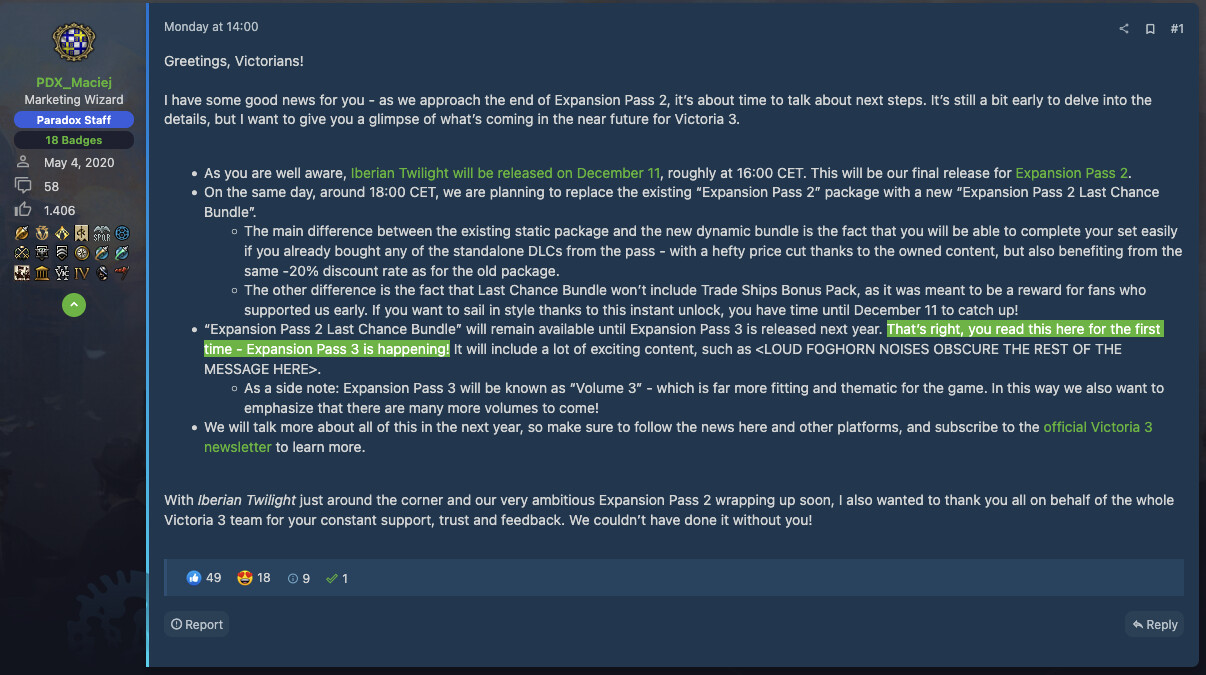

Myös Victoria 3 lisäosatuotanto jatkaa täyttä häkää eteenpäin. Iberian Twilight julkaistaan joulukuussa eikä homma jää siihen, vaan myös Expansion Pass 3 on tulossa ensi vuonna:

4 tykkäystä

Odotettu uutinen. Ja Fredrikin viesti on selkeästi ”ei enää ydinosaamisen ulkopuolelle”.

Tämä on muuten myös hyvä muistutus Paradoxin melko nopeasta pelien poistoista taseesta muutenkin. Yhtiö aktivoi taseeseen työntekijöiden vessakäyntejä myöten pelikehitysmenot. Kun peli julkaistaan, näitä aktivointeja poistetaan nopeassa aikataulussa.

Niinpä alaskirjaus tulee suunnilleen samankokoisen poiston päälle ja melkein koko noin 70MEUR kehitysprojekti häviää taseesta yhdessä kvartaalissa. ![]()

”Paradox Interactive has today decided to make a non-cash write-down of MSEK 355 of capitalised development costs for the game Vampire: The Masquerade - Bloodlines 2 in the fourth quarter. The write-down is made in addition to the quarter’s scheduled degressive amortisation of MSEK 346. At the end of the year, MSEK 40 of the capitalised development costs will remain on the balance sheet. The write-down is based on an updated sales forecast made 30 days after the game’s release.”

Harvoin Sharevillessä on tänne lainaamisen arvoisia kommentteja, mutta tämä kommentti Paradoxista tiivistää hyvin mielestäni sijoitustapauksen tällä hetkellä. Englanninkielinen on automaattinen käännös.

Haven’t looked much at the company yet, but it seems like it’s priced to do roughly what it has done previously, and the downside is that they fuck up and the upside is everything else?

Har ikke sett noe særlig på selskapet enda, men virker som det er priset til å gjøre omtrent som det har gjort tidligere og nedsiden er at de fucker opp og oppsiden alt annet?

Ps. Vielä yksi potentiaalinen alaskirjaustapaus on kehityksessä, eli PA2.

9 tykkäystä

Osake reagoi avauksessa muutaman prosentin plussalle. Olisiko tämä merkki siitä, että voidaan lopullisesti haudata nämä sekoilut, sekä keskittyä jatkossa coreen?

Mikä itsellä paistoi silmään tuosta Fredrikin viestistä, oli tämä lause:

" Going forward, we focus our capital to our core segments and, at the same time, we’ll evaluate how we best develop World of Darkness’ strong brand catalogue in the future."

Voisiko tämän tulkita niin, että World of Darkness IP olisi Paradoxilla myynnissä? Näpit tuli poltettua niin pahasti, että joku muu voi tämän kanssa touhuta jatkossa?

Tuosta alaskirjauksen suuruudesta kertoo hyvin se, että viime vuoden Q4 Paradox teki noin 311 MSEK EBITtiä. Eli sieltä on aika reilu lovi pyyhkiytymässä pois tulevasta ennätyskvartaalista.

Toinen vertailukohta on Remedyn Firebreak. He alaskirjasivat muistaakseni 19 milj. €, mikä on paljon pienempi kuin tämä Bloodlinesin ~32 milj. €, ilman mainittuja luontaisia poistoja.

En tiedä ovatko muut huomanneet saman, mutta Paradox on tuotannollistanut tämän “jatkuvaluonteisen tilauksen” aika hyvin pääpeleihinsä. Jos menette vierailemaan käytännössä mihin tahansa pääpelin Steam-sivulle, niin näette tämänlaisen mainoksen:

Toisena esimerkkinä Stellaris, johon muuten ilmestyi tuo DLC, Infernals, pari päivää sitten:

Tuolta Steamista voi siis melkeenpä parhaiten vakoilla, mihin kvartaalille tulee aina mitäkin myyntiä. Ja kun yksi Expansion pass (vai millä nimellä sitä kutsutaankaan kussakin pelissä) loppuu, niin seuraava julkaistaan. Näin kävi Victoria 3:kin tapauksessa.

8 tykkäystä

Terve foorumille,

mukavaa, että Paradoxista löytyy suomeksikin sijoittajakeskustelua, olen tätä parin vuoden ajan käynyt lukemassa.

Sijoittajan näkövinkkelistä on oivallista, että Paradox pitää taseensa realistisena ja pelien arvo tai sen puute tunnistetaan ja kirjataan. Ei pitäisi jäädä suurempaa epäilyksen varaa.

Itse tuotteista olen aina pitänyt ja EU5 on mielestäni valtava menestys toiminnaltaan ja pelinä itsenään. Kaupallinenkin menestys on mielestäni lupaavaa steam-arvostelujen ja pelaajamäärien perusteella, mutta laskuharjoitteita en ole kerennyt tehdä. Myös pelin foorumit ovat erittäin aktiivisia, joka on hyvä merkki siitä, että peli kiinnostaa ja ihmiset jopa keksivät itse jatkuvasti ideoita deveille miten korjata asioita. Ja nämä myös otetaan huomioon.

Näen tämän melko suurena valttina, pdx yhteisö toimii ilmaisena resurssina kehitykseen ja sen on firma tajunnut huomioida. Myös maine on pelifirmalle epätyypillisen hyvä kuluttajien näkökulmasta, vaikkakaan tähän minulla ei mitään dataa ole. Ns. Trust me arvio siis. (pl. julkaisijana muiden möhlimiset, eli CS2 ja uusin Vampires).

Olen yllättynyt tosin miten valtaisien q4 releasien ajoitus ja menestys ei tosin näy kurssissa. Eu5 on varmastikim tulevaisuuden cash cow, ja luulisi että sen julkaisuonnistumisen epävarmuus olisi pitänyt kurssissa jo korjaantua. Aiempia erheitä on ollut näissä esim. pahamaineinen Leviathan EU4.

Osaaminen on näissä GSG, joten todella hyvä uutinen että näihin keskitytään ja lypsetään lähes monopoliasemaa tässä niche pelialassa.

Mitä mietteitä teillä, mennäänkö osakkeessa järkevissä hinnoissa? Olisi mieleistä ajaa laskuharjotteita eu5 menestykselle, jos löytäisi enemmän aikaa.

Yksi mahd. negatiivinen detaili pelaajan näkökulmasta: Eu5 ja Vic3 ovat hyvin saman henkisiä. Olen itse jättänyt jälkimmäisen lähes 0 huomiolle ja näin saattaa pysyäkkin, vaikka aiemmin olenkin kovasti siitä pitänyt.

10 tykkäystä

Tuli vaan tuossa aamulla vastaan että Danske nostaa tavoitehintansa 210 SEK ja suosituksen Pidä → Osta.

Mikä nyt siis on minun mielestä ajallisesti outo, että heti kun saatiin Bloodlinesin alaskirjaus tehtyä niin samantien Paradox muuttui super-huippu osakkeeksi. Että aika paljon se Westerin lause siinä tiedotteessa näyttää painavan.

Ja minähän olen vaan katkera etten kerennyt tähän ralliin mukaan ja odotin että kurssi ottaa nenään siitä alaskirjauksesta.

Alla Nordnetistä kopioitu ja tekoälyllä käännetty

Danske Bank nostaa suosituksensa peliyhtiö Paradoxille tasolta pidä tasolle osta ja tavoitehinnan 210 kruunuun (180), analyysin mukaan.

Nostoa perustellaan sillä, että tärkeä julkaisu Europa Universalis 5 on kehittynyt hyvin, ja peli näyttää etenevän analyysitalon neljännesvuosiennusteiden mukaisesti.

”Vielä tärkeämpää on, että tämän pelin menestys on todennäköisesti raivannut tietä monille vuosille jatkossakin sarjan ja sen ‘pelipalveluna’ -mallin onnistumiselle”, pankki kirjoittaa.

Lisäksi Danske Bank huomauttaa, että DLC:t (pelien ladattavat lisäsisällöt) on julkaistu lähes kaikkiin yhtiön ydinsarjoihin ja että ne vaikuttavat suoriutuvan hyvin.

Samalla Bloodlines 2:n odotettu alaskirjaus tarkoittaa, että yhtiön tilanne on vihdoin jättänyt taakseen ”roskajaksonsa”.

Tämä merkitsee, että katse voidaan suunnata tulevaisuuteen, ”joka koostuu käytännössä vain siitä, missä Paradox on markkinajohtaja: suurista strategia- ja simulaatiopeleistä”, pankki kirjoittaa.

Kokonaisarviona Danske Bank toteaa, että yhtiö ”on nyt parhaassa asemassa pitkään aikaan”, kun viimeaikaiset onnistumiset otetaan huomioon.

7 tykkäystä

Jälleen hyvä muistutus Mr. Marketin mielialoista ![]()

Ps. Hallituksen jäsen Mathias Hermansson kävi tankkailemassa osaketta 410 880 SEKillä https://x.com/InsynshandelSE/status/1994031678545596601

3 tykkäystä

On tämä kyllä. Itsekin odottelin, että tässä vielä jonnekin 150 SEK tasoilel valuttaisiin ennen kuin kiinnostaisi panoksia tähän laittaa sisään. Sen sijaan jatkan edelleen sivusta katsomista, kun reippaasta alaskirjauksesta huolimatta yhtiö ampaisi yli Remedyn markkina-arvon verran ylöspäin negatiivisiin, joskin odotettuihin, uutisiin. Alaskirjaus tuskin olisi myöskään hirväesti isompi voinut olla. Koon perusteella kyllä siinä suurin osa kehitysbudjetista alaskirjattiin.

Edelleen kaksijakoiset fiilikset tästä osakkeesta. Puhutaan laatuosakkeesta, mutta lähes kaikki tekeminen Grand Strategy coren ulkopuolella ollut älytöntä arvon aktiivista tuhoamista. Prison Architecht 2 vielä odottelee samaa kohtaloa kuin Cities Skylines 2, Bloodlines 2 ja Life of You. Sinänsä toki positiivista, että johto on nyt muutaman pelin muuta markkinaa jälkijunassa ymmärtänyt, että ehkä tämä genren ulkopuolisten pelien tai 3rd party julkaisutoiminta ei ole ihan parasta yhtiön corea. Kehitysputkessakin taitaa enää PA2 olla näitä huonosti hallinnoituja 3rd party tekeleitä, niin siinä mielessä mielestäni toimarin kommentti on nolllauutinen, enkä täysin ymmärrä markkinareaktiota.

Onneksi kuitenkin EUV julkaisu näyttää riittävän onnistuneelta, että jatkanee dominointia omassa coressaan.

Vaikka onkin huolestuttavaa, että pelaajamäärät ovatkin timesink-kaltaisessa pelissä näin merkittävässä laskussa, on julkaisu kuitenkin ollut sen verta iso, että mitään hätää ei ole. Lisäksi Paradox on kouluttanut pelaajakuntansa, itseni mukaan lukien, odottamaan pelien ostoa myöhemmin kun peliä riittävästi korjailtua ja muutamia lisäsisältöjkä tehty. Eiköhän peli 2-3v akselilla myös omaan pelikirjastoon löydä, yleensä ajan kanssa muutaman lisäsisällön kanssa.

Uskon kyllä, että Grand Strategy coressa on vielä kasvuvaraa, ellei markkinalla tapahdu jotain, mikä muuttaisi Paradoxin monetisaatiomallia toimimattomaksi. Sisäinen kannibalisaatio genren sisällä saattaa myös tulevaisuudessa olla riski, erityisesti jos kuluttajien ostovoimahaasteet markkinalla jatkuvat. Uskon, että Grand Strategy coressa on poikkeuksellisen vahva pelaajaretentio. Nämä pelaajat ovat nyt keski-ikäisiä ja jatkanevat näiden pelien pelaamista 60+ ikään asti, vaikka ympäröivä markkinakasvu pysyisikin hitaana tai stagnoivana.

Grand Strategy core tuo suht tasaista ja ennustettavaa pohjaa ja turvaa operatiiviviselle kassavirralle, kun sen verran etabloituneita IP:tä ja back-katalogitavaraa, joille voi tasaisiin väliajoin tehdä jatko-osia. Toisaalta tämän ja seuraavan vuoden P/E 30-45 hinnoittelee yhtiölle voimakasta tuloksen kasvua. Samoin myös EV/EBIT parinkymmenen yläpuolella ja EV/S laatupeliyhtiön kertoimilla jossain 6-7 paikkeilla. Grand Strategyn osalta mielestäni kertoimet varmaan pätisivät, mutta niin kauan kuin kaikki muu tuhoaa aktiivisesti arvoa, niin mietityttää.

En ehkä ihan täysin yhdy Vernerin/Nordettiläisen kommenttiin. Kyllä mielestäni nykyhintaankin, ainakin nyt edellisen 2pv nousun jälkeen, leivotaan selvää operatiivisen tekemisen paranemista, jolle toki EUV julkaisu luo hyvän pohjan. Harva julkaisija kuitenkaan loputtomiin voi selvästi tappiollisen ROI:n pelejä julkaista.

Voi olla, että olen Remedystä liikaa traumatisoitunut, mutta saan Paradoxista liian Remedynkaltaisia viboja viime vuosien tekemisestä, että uskaltaisin tähän koskea ellei tule selkeää sentimenttiylilyöntejä alaspäin, joka tasaisi niin yhtiö- kuin markkinariskejä. Alaskirjaukset kuuluu pelialaan, mutta tuotantovaiheessa ei saa pelejä alaskirjata, ja Bloodlines 2 / Skylines 2 on varmasti ollut kaikki merkit ilmassa että ei tästä kaupallisesti oikein mitään voi tulla. Julkaisupuolen projekti/portfoliojohtaminen on ollut käsittämättömän surkeaa, mutta sitä on onneksi paikattu sillä, että kotipesä pidetty kunnossa (EUV / Paradox Tinto).

World of Darkness myyntiin, AA julkaisutoiminta minimiin ja jatketaan hissukseen Grand Strategy monopoliaseman kasvattamista hyvillä marginaaleilla ylläpitäen hyvää kassatilannetta erikoistilanteita varten (fokusoitua M&A silloin kun valuaatiot alhaalla ja omistajille hillon jakamista kun valuaatiot ylhäällä) niin eiköhän matka kohti vanhoja tai uusia kurssihuippuja voi alkaa.

12 tykkäystä

Tämä on myös hauskaa, että Fredrik on ilmaissut yhtiön keskittyvän ydinosaamiseensa jo vuosia strategiassa ja puheissa, vaikka “legacy” projekteja mihin on ollut edes vähän uskoa on jatkettukin. Bloodlines 2:sen alaskirjaus taas ei pitäisi olla yllätys, vaan perusodotus. ![]() Itse odotin vain sen tapahtuvan Q4:sen yhteydessä, mutta nyt kun tarkemmin miettii pitäähän aktivoidut menot heti kirjata alas kun on ilmiselvää ettei ne tuota odotetusti.

Itse odotin vain sen tapahtuvan Q4:sen yhteydessä, mutta nyt kun tarkemmin miettii pitäähän aktivoidut menot heti kirjata alas kun on ilmiselvää ettei ne tuota odotetusti.

Toisin sanoen, mitään odottamatonta ei ole tapahtunut! ![]()

Kait tässä on psykologista efektiä, kuin mätä hammas olisi vedetty vasta nyt suusta pois.

Tottakai! Yhtiön raportoitu tuloshan tulee olemaan alaskirjausten takia tänä(kin) vuonna kehno.

Mutta kun legacyprojektit on kirjattu alas ja unohdettu, jäljellä on vahva ydin minkä pelit tekevät jopa 60 % liikevoittomarginaalia!

Sen lisäksi pelikehitysfilosofiaa on hiottu. Aiemmin kokeiltiin isolla rahalla uutta (Life by You, BL2 jne.). Nyt kokeilut tehdään pienellä kokeilurahalla Arcissa ja skaalataan isommaksi, jos näyttöjä on tai lopetetaan pelin tukeminen, jos ei ole. Kuten kävi äskettäin Milleniumille.

8 tykkäystä

Kun tässä olen koittanut keksiä, että mistä se tulevaisuuden kasvu tulee kun kohta kaikki coret on saanut uusimman iteraationsa (ps. Stellaris 2 julkistetaan ensi vuonna, kuulit sen ekana täältä) niin täältä se varmaan löytyy ja tämä on aika riskitön tapa kuten Verneri sanoi. Mutta kyllä tässä pitää olla kunnianhimoisempi kuin mitä se nyt Space Trash Scavengereiden Darfallien kanssa.

Uusien IP:iden tuominen grand strategy genreen on ollut vaikeaa ja nämä tuntuu tarvitsevan useamman iteraation että nämä lähtee lentoon. Kaikki coret on periaatteessa tarvinneet sen toisen iteraation että ne on lähtenyt lentoon (CK, HoI, EU). Olisikin hauska nähdä (muiden rahoilla tietty) että jos Imperator: Rome 2 tulisikin ulos että miten sille kävisi.

4 tykkäystä

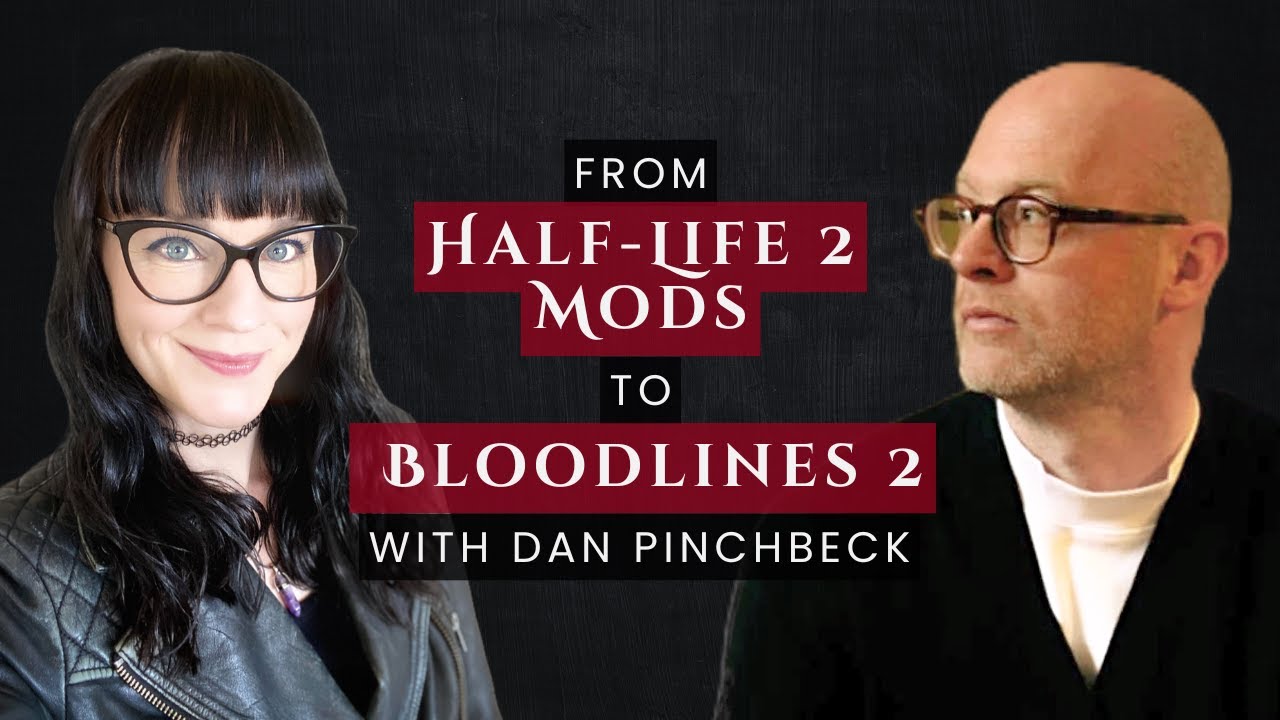

The Chinese Roomin Dan Pinchbeckillä (TCR:n perustaja ja ex-luova johtaja ja Bloodlinesin käsikirjoittaja) kommentoi Bloodlinesin handoveria. Paradoxilla on vissiin ajateltu, että pelkästään Bloodlinesin nimellä saadaan positiivinen ROI. Selvää on ollut alusta (puolivälistä) lähtien että tästä ei tule mitään.

Ja jos nimi olisi vaihdettu niin ei se sekään olisi ollut kyllä voittava liike.

[…] He was sceptical whether the studio could develop a worthy sequel to the 20-year-old original.

“Right from the word go, there was one of the producers, then at Paradox, who I’m still friends with, who’s now with another publisher,” he explained. “We used to sit there and go and have these planning sessions of, ‘how do we get them to not call it Bloodlines 2?’

“’That feels like the most important thing we do here is to come at this and say this isn’t Bloodlines 2. You can’t make Bloodlines 2. There’s not enough time. There’s not enough money’.”

However, he claimed that due to the many interests from the various stakeholders, Bloodlines 2 became like “untangling an anaconda fuckball of competing priorities and what everybody wants and things like that”.

Haastattelu timestampattynä alkamaan siitä kun aletaan käsittelemään Bloodlinesia

3 tykkäystä

Toisaalta nykyiselläkin ydinportfoliolla on kasvettu tähän asti komeasti, ja oletettavasti kiitos EU V:n kuluva Q4 on uusi myyntiennätys.

Kaikki hiekkalaatikon ulkopuolelle laajentumisen rönsyt, kuten lamplighterit, lifebyyout ja bloodlinesit eivät ole joko päässeet ulos kehityshelvetistä tai ne ovat flopanneet. Kasvua on siis pääosin ajaneet mahtiviisikko-IP:t kuten Hoi, EU, CK, CS ja viimeisimpänä Victoria.

Yhtiön liikevaihto on yli 2020 hulinavuosien huippujen, kiitos ydinportfolion, ei kiitos sen porukan ulkopuolisten kasvuhankkeiden. ![]() Ja oletettavasti vuoden 2024 huippu ohitetaan myös pian.

Ja oletettavasti vuoden 2024 huippu ohitetaan myös pian.

Miniatyyrimahti Games Workshop toistelee, että paras tapa luoda omistaja-arvoa on olla tuhoamatta sitä.

Tavallaan toivon, ja Fredrikin viime vuosien viestintä tukee tätä, että Paradoxilla on otettu samanlainen ote pääoman allokointiin.

Yhtiön kassavirta on vuolasta, mutta sitä on heitetty hölmöihin ja kalliisiin projekteihin ydinosaamisen ulkopuolelle.

Tyytyisin mielelläni ydinpelien hitaampaan (joskin muistaakseni Paradox-esityksessä he puhuivat ~15 % kasvusta eli ei se pientä ole) kasvuun ja fiksumpaan kassavirran allokoimiseen esimerkiksi osinkoina, kuin että yritetään kiihdyttää kasvua kaatamalla rahaa kankkulankaivoon.

Juu tajusin, halusin vain kompata sitä laajentamalla pohdintaa. ![]()

8 tykkäystä

Tämä se minun pointti oli. Kaikki coret ovat saaneet uusimman iteraationsa joka näkyy komeasti käppyröissä; mutta entä sen jälkeen kun Stellaris 2 tulee ulos. En näe oikein realistisena sitä että iteraatio sykli aloitetaan uudestaan? Toisaalta Hearts of Iron V voisi olla 2030 korvilla ja CK4 2033 etc…?

5 tykkäystä

Eikö pelien ja käppyröiden numerot termien sykli ja iteraatio lisäksi kerro syklin olemassaolosta ja toimivuudesta. Core tai ydin on vahvistunut kun on pysytty omalla vahvuusalueella. Eivätkä luonnollinen pelisarjan rakenne ja uuden aloittaminen poissulje toisiaan. Jos se vaikka pysyy mainitun fiksumman kassavirran allokoinnin raameissa.

Mikromaksupohjaisen lisäsisällön/palvelulaskutuksen ideahan on vain siirtää muuhun siirtymistä. Kun se tulee eteen mikä järki tappaa lypsävää lehmää kun viime kädessä ainoa mitä pelaajat haluavat on laadukas kokemus. Uuden kokemuksen saa mistä vain.

2 tykkäystä

Paremmasta fokuksesta ja kassavirran käytöstä tuli mieleen myös tämä tuore uutinen Tencentistä, joka poikkeuksellisesti kasvaa pelimarkkinalla näinä vaikeina aikoina.

Tencent Goes Hands-On to Reshape $10 Billion Global Games Empire

Tencent ennen roiski vain rahaa menemään sinne tänne, ja se omistaa mm. Paradoxista sekä meidän Remedystäkin siivun. Liekkö Tencentiltäkin vihjattu studioille, että saa välillä tehdä enemmänkin rahaa. Aiemmin se on ollut omistajana passiivisempi.

4 tykkäystä

Siis miksi pitäisi aloittaa uudestaan? Paradoxin ansaintamalli perustuu hyvin pitkälti lisäosamyyntiin, ei sillä ole juurikaan väliä miten usein uusia pelejä julkaistaan. Jos tota Vernerin graafia katsoo, niin ei siinä julkaisuvuodet tee oikein minkäännäköistä pomppua. Uutta peliä tarvitaan vasta siinä kohtaa, kun vanhaan ei pystytä enää tuottamaan myyvää lisäsisältöä.

4 tykkäystä

Pieni spekulointi sallittakoon ![]()

Paradox on vekkulina osakkeena taas livahtanut alle 160 SEKin. Suhteessa yhtiön positiiviseen suorittamiseen tämä on omituista. Aina voi vedota teknisen analyysin laskutrendiin, mutta peliosakkeissa kurssia usein tuntuu ohjaavan enemmän tunteet, kuin fundamentit.

Spekulointia, johon törmäsin alunperin X:ssä: Paradoxin yksi suurimmista rahasto-omistajista on ruotsalainen TIN Ny Teknik A, joka kuuluu rahastoyhtiölle Tin Fonder. Rahasto ei omista yhtiöstä kuin reilun prosentin lyhyen googlauksen perusteella, mutta koska Paradoxin float on ylipäätään pieni suuren sisäpiiriomistuksen vuoksi, niin myös “pienet pelurit” voivat vaikuttaa kurssiin. Paradox istuu rahastossa noin ~8% painolla.

Ny Teknik A on ollut ruotsalaisten huomiossa tämän vuoden aikana, koska rahaston poiminnat eivät ole menneet putkeen. Rahaston isompien omistusten pommeihin kuuluvat mm.

- Surgical Science Sweden AB (-78% YTD)

- Novo Nordisk (-50% YTD)

- Evolution (-28% YTD)

- Qt Group (-52.5% YTD)

- BioGaia (-12% YTD)

Itse rahaston YTD on -24%. Hikikarpalot on varmasti geelitukkien otsalla.

Foliohattuteesi: Joutuukohan TIN Ny Teknik A keventelemään Paradoxin painoa parhaillaan, koska se kasvaa liian suureksi? En tiedä juuri tuon rahaston sääntöjä, mutta 8% paino alkaa olemaan jo aika suuri. Jos koko muu salkku haukkaa turskaa, niin pakko iskeä suurinta osaketta laitaan hinnasta huolimatta? Puhumattakaan siitä, että rahastosta otettaisiin rahoja ulos huonon vuoden jälkeen-> pakko nostaa käteispainoa.

Minut saa vapaasti polttaa roviolla, jos tuntuu liian villiltä spekuloinnilta

13 tykkäystä

Warren Buffett taisi joskus sanoa, että jos joutuu Pythonilla analysoimaan firman lukuja, niin osakkeessa ei ole tarpeeksi turvamarginaalia.

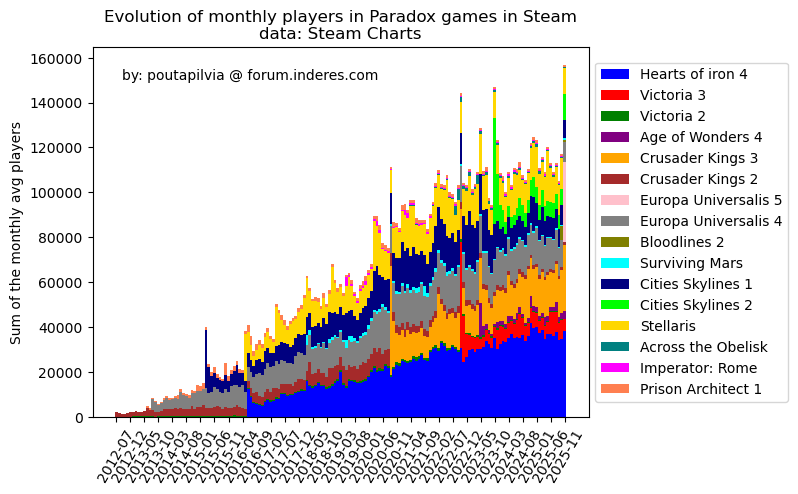

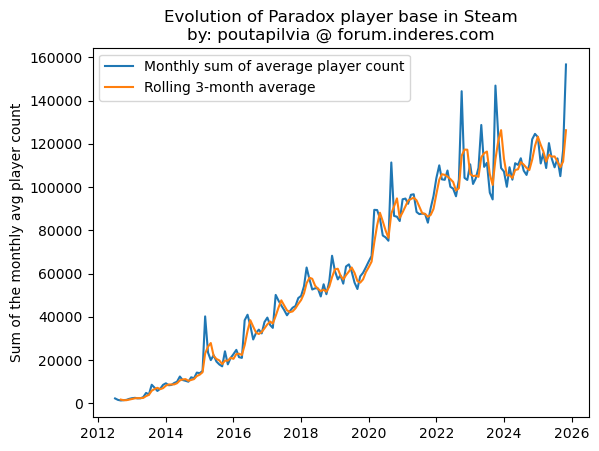

Anyways, kävin repimässä netistä (Steam Charts) Paradoxin pelaajamääriä seuratakseni niiden kumulatiivista kehitystä. En ottanut kaikkia pelejä huomioon, vaan nyrkkisääntönä käytin vähintään ~1000 Steam-pelaajaa lähivuosilta.

Marraskuussa hypättiin uusiin kaikkien aikojen huippuihin:

Siitä voi yrittää arvioida suhteellisia osuuksia, mutta en jaksa itse niitä nyt analysoida. Tuota kokonaiskehitystä kuitenkin visualisoin nätimmin:

Eli marraskuun pelaajamäärien ATH:n lisäksi 3-kuukauden liukuva on myös hyppäämässä kaikkien aikojen huippuihin. Pitää vielä odotella joulukuun luvut, niin pystytään analysoimaan Q4:ää paremmin.

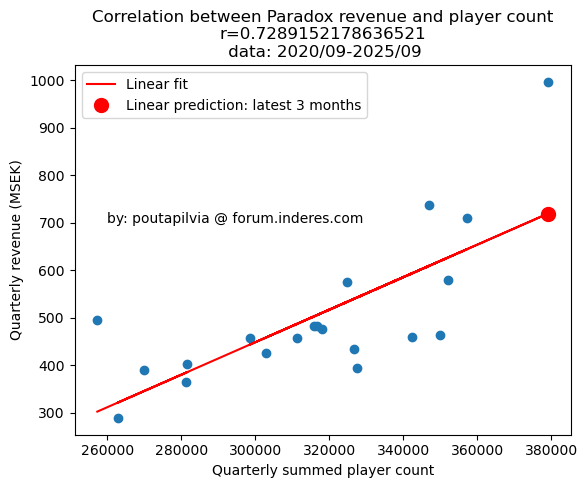

Lopuksi vielä Paradoxin kvartaalikohtaisen liikevaihdon ja vastaavien kuukausien pelaajasumman korrelaatiosta. Tein lineaarisen ennusteen viimeisimmästä kolmesta kuukaudesta (marras+loka+syys), ja niiden perusteella liikevaihtoa kertyisi noin 700 MSEK. Pitää tämäkin laskea uudelleen, kun joulukuun luvut saadaan kasaan, jotta voidaan veikkailla Q4:n liikevaihtoa.

16 tykkäystä