I’ve been following Panoro Energy’s journey for a while now. I recommend reading a very insightful article from the investment forum by the user Xrtainvestor. It recaps events since 2013 and also covers these recent developments, which are why I’ve increased my position.

I’ll try to add some value to that article with a few figures for those who appreciate numbers.

I’ve been involved since ancient times, following the company’s transformation and survival, partly by luck (seriously, read that link now). The board and CEO who started in 2015 have demonstrated their ability to make the right decisions. They have experience in the oil industry, as well as ownership in the company. In 2018, deals were made for Tunisian fields, and just before Corona in 2020, a “farm-in” was agreed for Block 2b in South Africa.

I increased my ownership during the COVID dip last spring, around 8 euros. But this was more about investing in the sector than specifically increasing my position in Panoro. Panoro was an easy choice in the sector, as the company was already familiar, my faith in management was solid, and the company’s debt situation was well under control. They had also hedged part of their production (was it about ¼?) at around $55/bbl. This was initially viewed with skepticism. Then came the pandemic, which highlighted how sensibly and experienced the company was managed.

Now to the main point: about a month ago, a bomb was dropped. In summer 2020, deals were being negotiated with oil prices around $40/bbl. Tullow Oil divested its 10% stake in the Dussafu field, which it had acquired through a “back-in right,” and at the same time, deals were shaken on two other African fields belonging to Tullow.

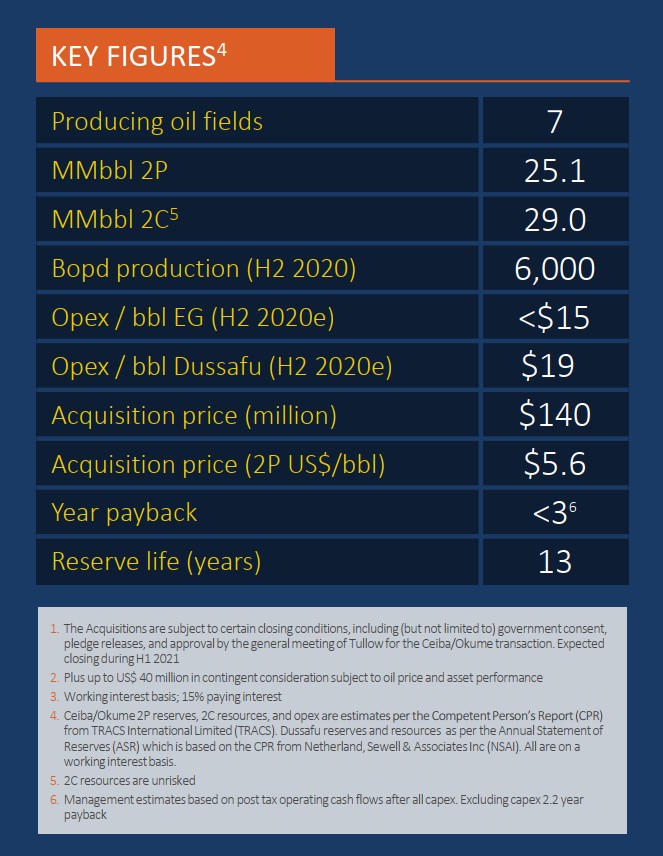

The deals are structured so that once all approvals are received, Panoro will effectively step into Tullow’s shoes from July 1, 2020. This will result in approximately $27 million in additional earnings in H2 2020, according to my calculations. Panoro has not yet published its 2020 financial statements precisely for this reason. The numbers will change once the deal receives all confirmations. Tullow’s general meeting approved the deal last week. The purchase price is $140 million, with an additional $40 million contingent on future revenues and oil prices. The financing was arranged by taking a $90 million loan and a $70 million directed share issue.

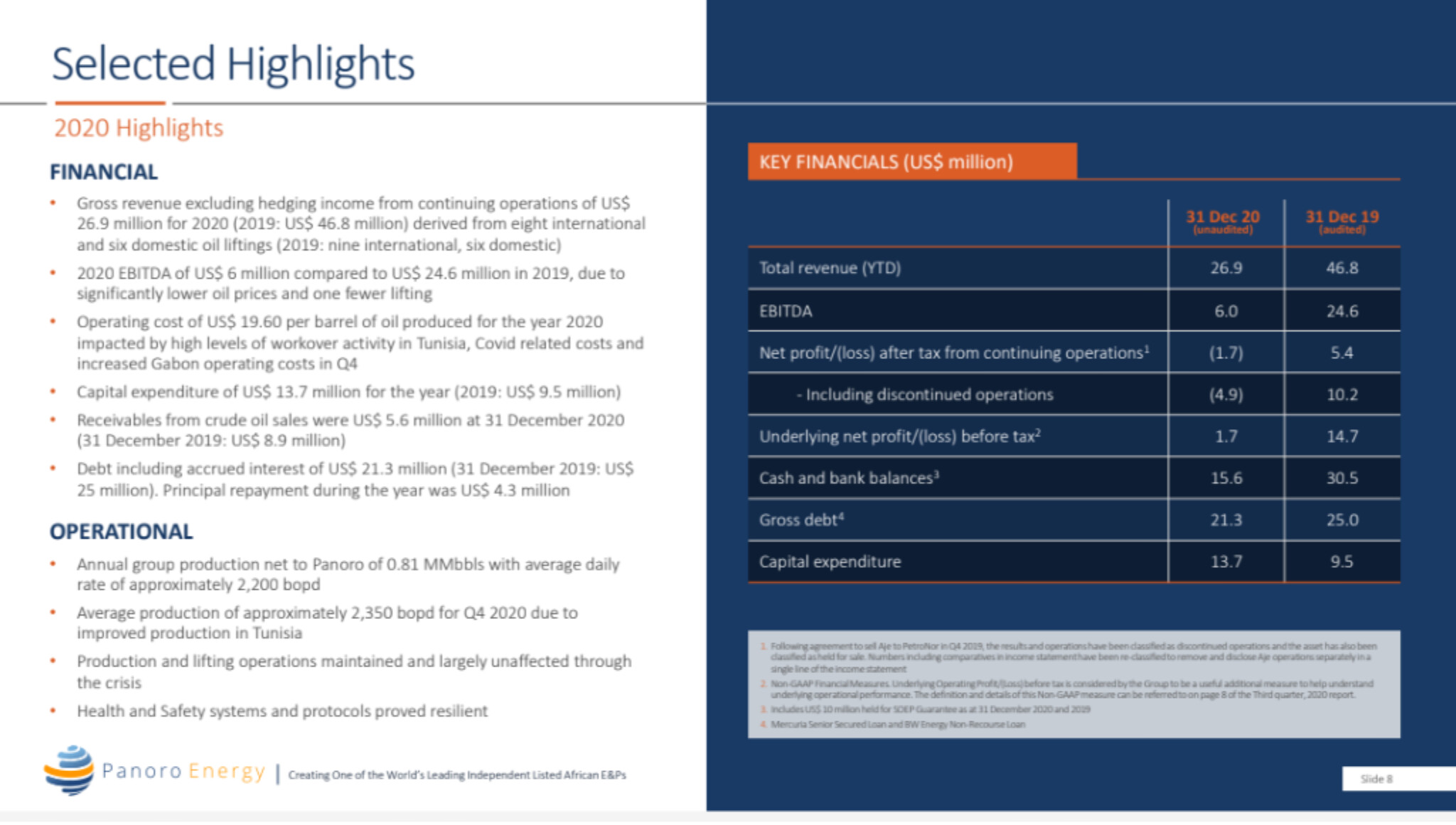

From the 2020 trading statement (while awaiting the financial statements), here are figures on acquisitions:

EDIT: Here is also a link to the 2020 trading statement presentation and the numbers only, which was published instead of the financial statements. For some reason, it hasn’t found its way to the website. The financial statements are indeed awaiting confirmation of the deal so that revenues from July 1st can be counted as Panoro’s sales.

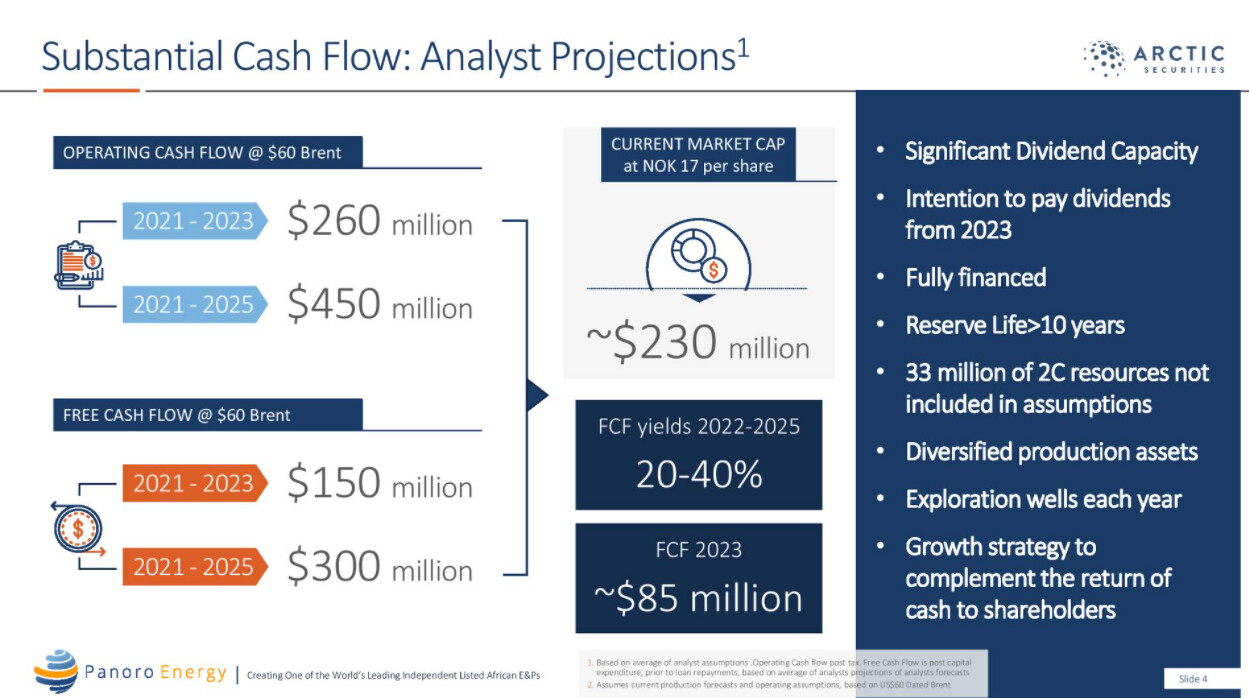

This slide first piqued my interest when I was going through the M&A presentation, especially the free cash flow section. $110 million in cash by 2023:

Latest public appearance from Friday. A short 15-minute chat that I encourage you to listen to.

The stock price is now around 20 NOK, or about 2.3 USD. Target prices from marketscreener.com from four analysts. Lowest $3.54 USD / 30 NOK, highest $4.74 USD / 40 NOK, average $3.85 USD / 33 NOK.

The CEO has repeatedly stated that the company will be ready to pay dividends in 2023. Net debt is $86 million.

Let’s calculate the 2021 P/E. I’ll try to use conservative estimates, as is typical for the company. 2 scenarios: Brent $60 USD and $50 USD.

(oil price $60 USD - tax 20% - OPEX $17 USD) * 9000 bbl/d * 365 - CAPEX 2021 $43 million / shares 113 million = $0.52 USD / 4.5 NOK / share. The price has been hovering around 20 NOK, P/E 4.5.

(oil price $50 USD - tax 20% - OPEX $17 USD) * 9000 bbl/d * 365 - CAPEX 2021 $43 million / shares 113 million = $0.29 USD / 2.5 NOK / share. The price has been hovering around 20 NOK, P/E 8.

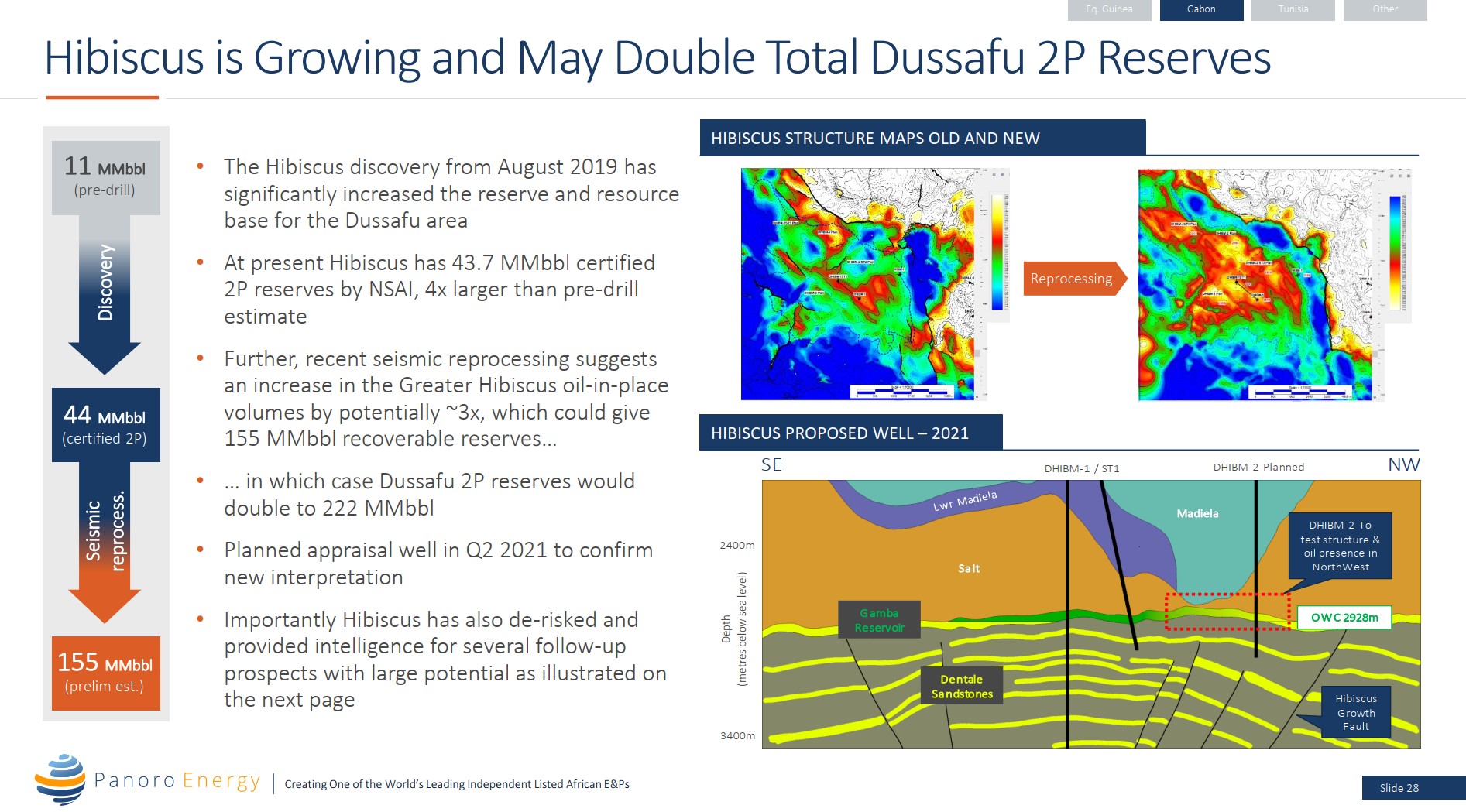

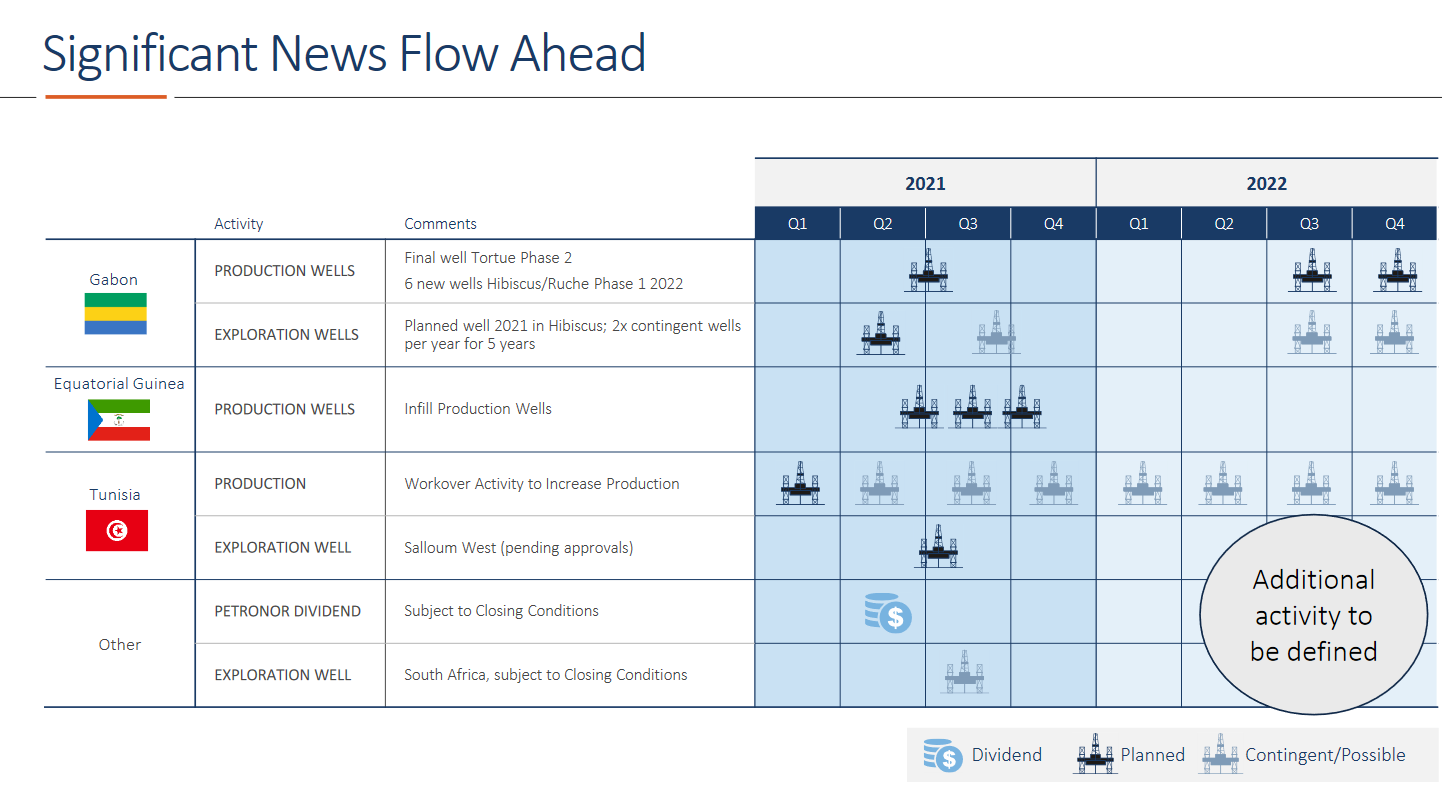

For 2023, the daily production is estimated at 12-13,000 bbl/d. In addition, potential increases in reserves or new discoveries could boost the share price. Exploratory drilling is set to begin in Dussafu very soon. According to seismic data, the existing Hibiscus field could be significantly larger than currently known.

The calculations clearly show the risk involved. The price of oil is everything. Of course, Panoro has a low OPEX. If oil drops back to the $40 USD level, they will still be profitable, but dividend plans will certainly be put on hold.

edit: added link to the 2020 trading statement presentation.