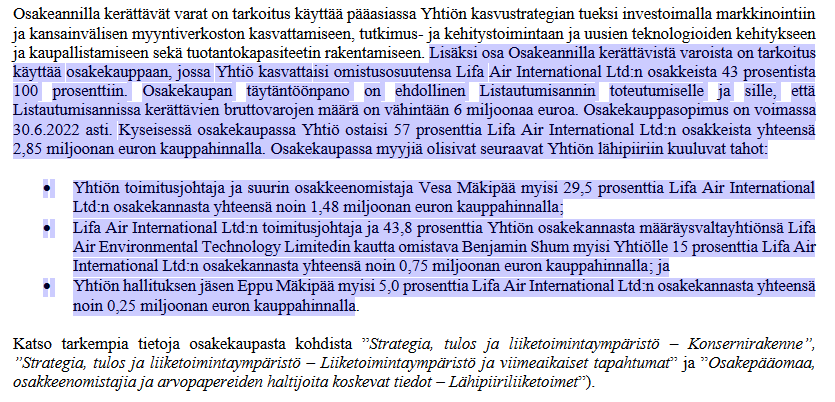

Isn’t an IPO practically always done precisely in the interest of the old owners? The company is owned by its owners, and the decision to list specifically represents the owners’ view; the “company” is not independent of its owners. Even if there was no sale by old owners involved, but purely the collection of funds for the company for acquisitions, the goal is still to increase the value and wealth of the company (i.e., the ownership of the old owners).

For the sake of reputation and PR, it is often worth considering the interests of future owners during an IPO, but participation in IPO subscriptions is always voluntary, and the “terms” are stated in the IPO prospectus. This was also the case here, and the possible subsidiary maneuvering was clearly explained and discussed on this forum as well.

This might be a bit off-topic, but when participating in IPO subscriptions, it’s always worth considering why the company is listing at that particular time and under those terms. If the current owners could maximize their own benefit by keeping the company private, the company generally would not list (regardless of the flowery phrases in the IPO roadshow). Listing means that the old owners are somehow seeking a favorable outcome for themselves, and new potential owners must evaluate for themselves whether it is worth joining at the specified price and terms. The traditional “old owners not selling” vs. “cash grab offering” distinction is, of course, a bit too black and white.

Regarding those wild future revenue targets versus past numbers, the company itself has quite clearly stated that they are based on an (IMHO) “double or nothing” strategy, meaning a sudden commercial breakthrough of something new. That is, a similar leap as came from the pandemic would be replicated with a new commercial breakthrough. The probability of this can, of course, be assessed either optimistically (the company’s own target) or realistically.

Lifa Air aims for an average annual revenue growth rate (CAGR) of 25–30 percent in the medium term. The company’s goal is to achieve a revenue of approximately 60 million euros by 2026. In the medium term, Lifa Air aims for an EBITDA margin of at least 20 percent and an equity ratio of 40 percent.

The company’s revenue target is mainly based on a commercial breakthrough of portable personal air purifiers and the expansion of the air purifier product segment into a more affordable price segment.

(Source: https://sijoittajat.lifa-air.com/lifa-air/taloudelliset-tavoitteet/ , bolding above is mine)

And as a disclaimer, I did not participate in the offering myself and will not touch this otherwise unless they truly demonstrate the ability for profitable growth without accidental pandemics. But I also don’t subscribe to hints that the company somehow defrauded those who participated in the IPO.