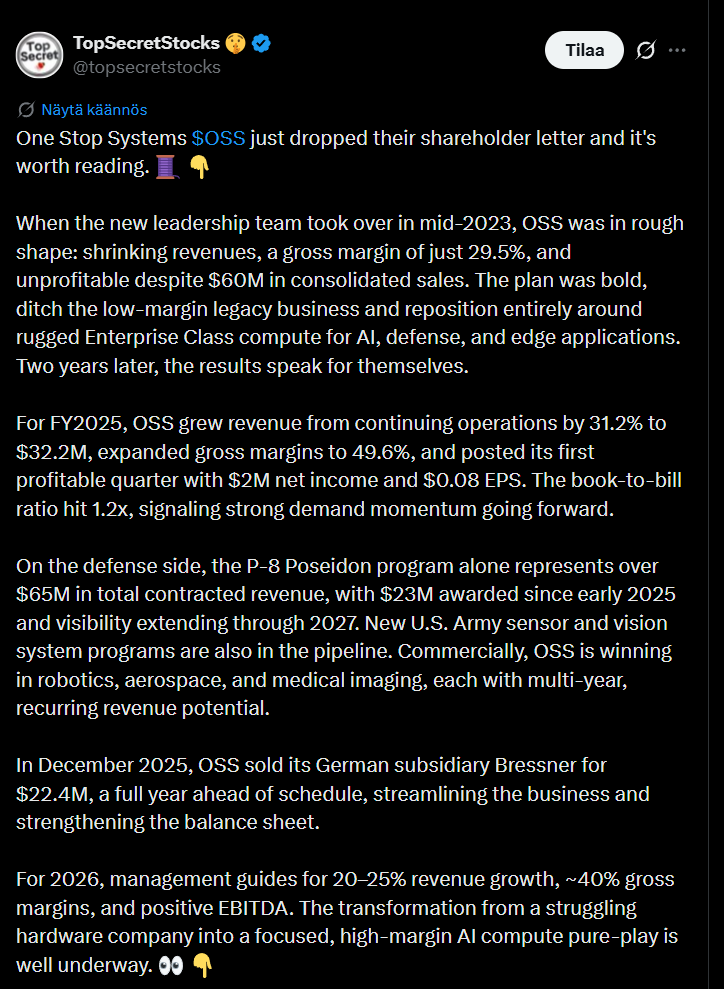

I’ve been thinking about opening a thread for OSS (One Stop Systems), but I’m lazy/busy enough that I haven’t had time before, and my research is still ongoing. Given OSS’s new contract and the ongoing war, now seems like a good time to delve a bit deeper into the company.

Below is a short introduction created by AI:

OSS (One Stop Systems, Inc.) is a US-based Nasdaq-listed company (OSS) specializing in high-performance edge computing and AI-accelerated computing solutions. The company develops and supplies rugged servers, as well as compute and storage solutions, specifically used for AI, machine learning, and sensor data processing in edge conditions (edge computing). OSS products are widely utilized in autonomous systems, industry, aviation, and other demanding environments. The company is strongly involved in the defense sector, having supplied rugged computing solutions to, for example, the U.S. Army and U.S. Navy. Significant collaborations have included:

- U.S. Navy P-8A Poseidon reconnaissance aircraft program (rugged data storage units for C5ISR tasks, which have resulted in over $65 million in orders for OSS)

- U.S. Army combat vehicle modernization (e.g., GPU-accelerated sensor processing and 360° view systems for Stryker, Bradley, and Abrams vehicles)

These defense collaborations highlight OSS’s expertise in extremely demanding military environments, where reliable, compact, and powerful AI computing is required.

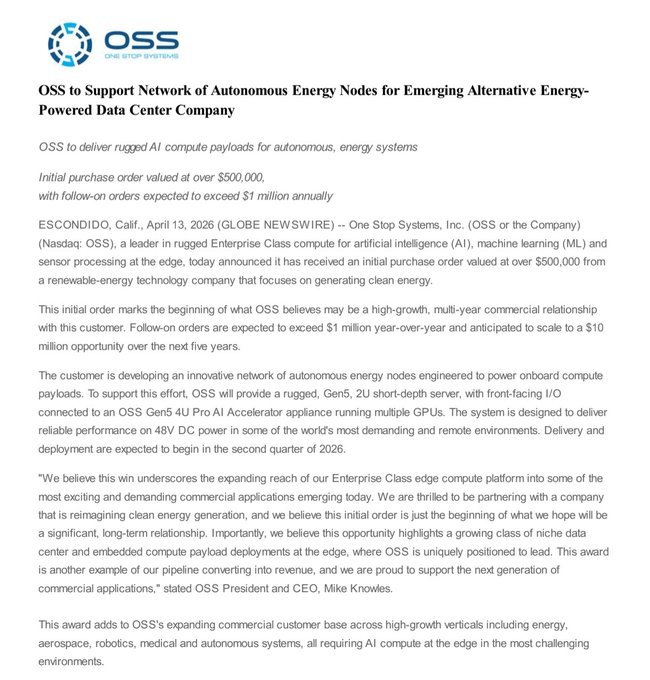

Today, OSS received a new order from a renewable energy technology company, and the expansion of client verticals was well-received by the markets:

The image shows OSS’s customer sectors, divided into two main areas:

Defense Sector. This is a significant growth area for OSS, especially with the US Army and Navy. Products are used in mobile and extreme conditions.

- Planes: Surveillance, reconnaissance, troop support (e.g., P-8A Poseidon aircraft).

- Watercraft: Autonomous boats, threat detection.

- Mobile Radar: On land, sea, and air.

- Vehicles: Autonomous vehicles, 360° situational awareness (e.g., Stryker, Bradley, Abrams combat vehicles).

- Mobile Command: Battlefield and exercises.

- Helicopters: Semi-autonomous systems.

- Submersibles: Autonomous submarines.

- Drones: Swarms and wingman systems.

Commercial Sector. This sector covers growing civilian markets requiring EDGE AI in remote or demanding environments.

- Autonomous Vehicles: Trucks, buses, trains, cars.

- Aviation: Security, networking, and entertainment.

- Commercial Data Centers: AI infrastructure, composite solutions.

- Mining: Mines (autonomous machinery).

- Video Surveillance: Facial recognition, security.

- Medical: Robotics, lasers, 3D scanners.

- Oil & Gas: Underwater oil rigs, remote locations.

- Agriculture: Tractors, combine harvesters (autonomous agriculture).

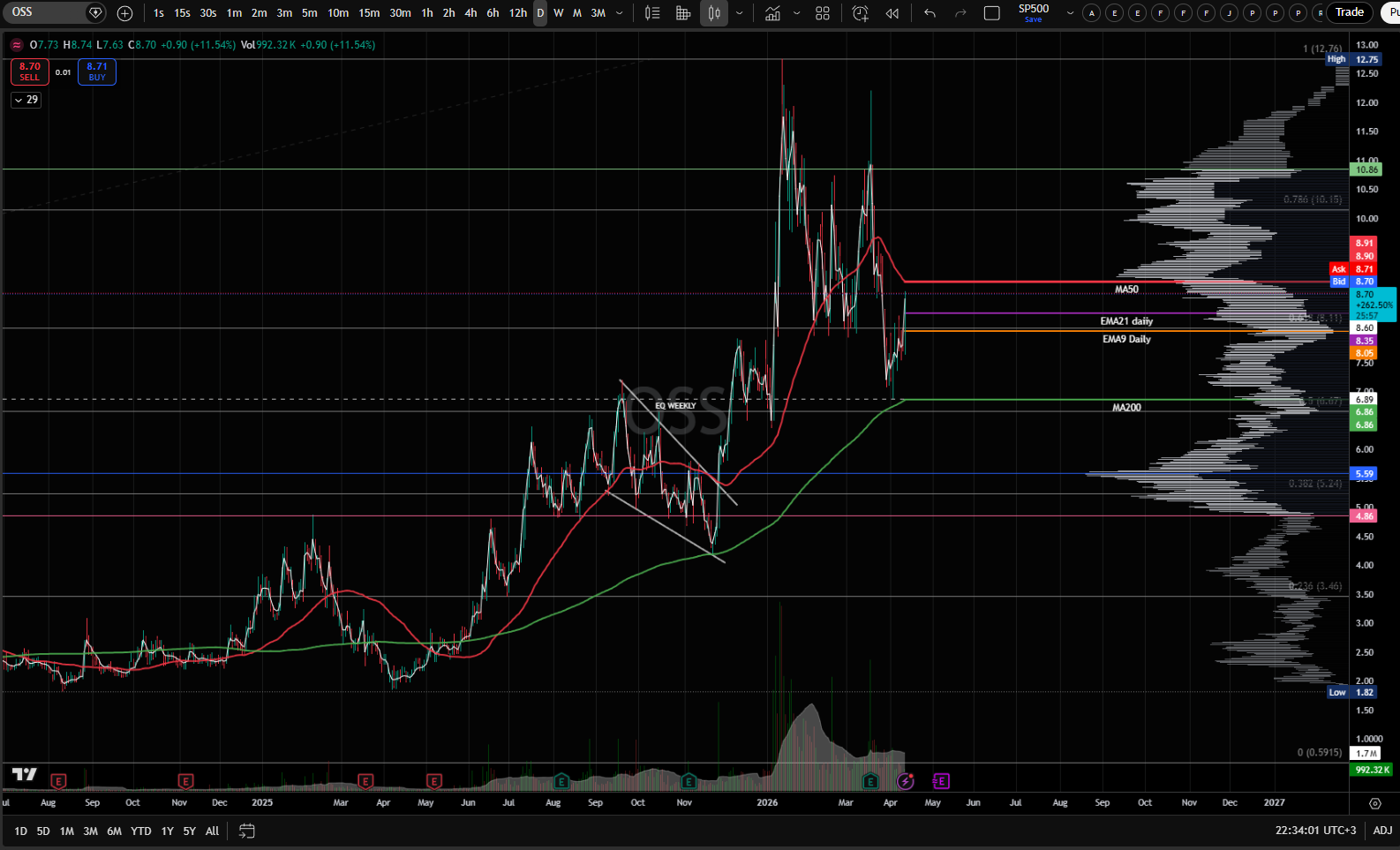

Technically, OSS has dipped with decreasing volume from its annual high by -30-45%, and the stock is squeezed between the descending MA50 and ascending MA200 (daily) moving averages. Over the year, the stock has risen by approximately +330%. The market cap is $215 million.

On OSS’s valuation:

The market has had difficulty pricing the stock due to factors like increased multiples, low market cap/small size, ongoing pilots, modest 2026 growth expectations, and future potential. In my opinion, the stock requires active monitoring. I had intended to increase my position if the stock fell to around $6.65-$6.80 and find clear support there (again). Based on the multiples, momentum could very well be sought deeper than that later in the year, but I don’t believe the institutional investors who have joined will give up all their shares unless there is a clear negative change in the story.

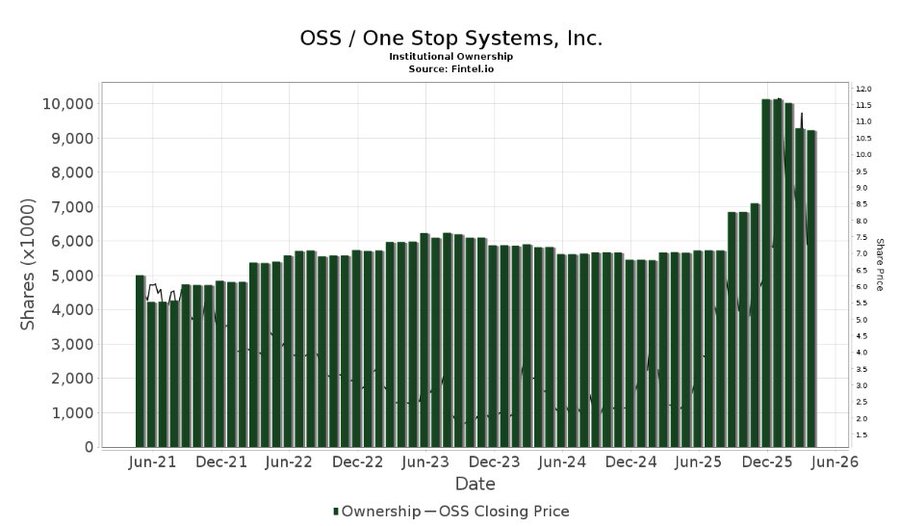

Institutions increased their ownership during the winter and have since slightly reduced their risk:

Finviz:

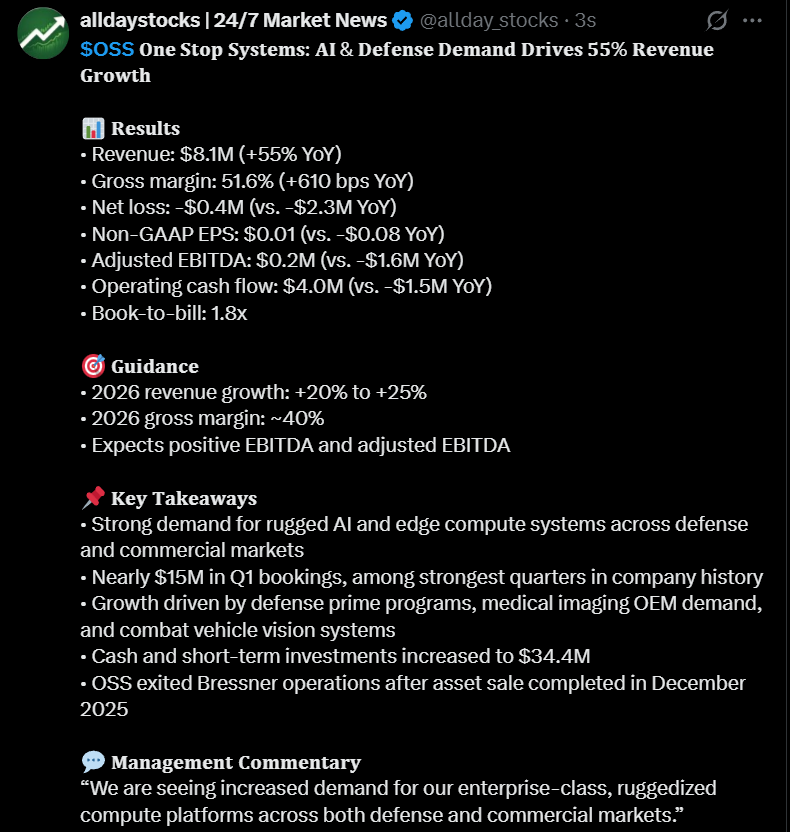

The company’s own guidance for 2026 (given with Q4 2025 results):

- Revenue growth of 20–25% year-over-year (2025 revenue was approximately $32M USD → target approximately $38–40M USD)

- Gross margin approximately 40% (Q4 2025 was exceptionally high at 58.5%)

- Positive EBITDA and Adjusted EBITDA for the full year

- Strong balance sheet: approximately $31M USD in cash, virtually debt-free, and good liquidity

OSS is not cheap this year, and expectations are high (situation in April 2026)

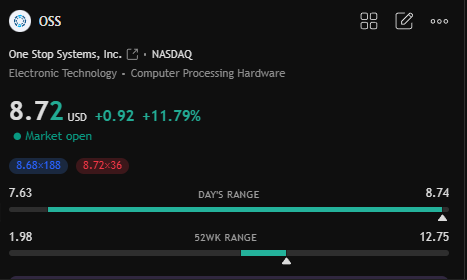

- Market Cap: approximately $215 million USD (share price ~ $8.70 USD)

- P/S (Price/Sales, trailing): 5.6–6.0x (2025 revenue ~ $32.2M USD)

- P/E (Trailing): approximately 34–45x (TTM EPS ~ $0.23 USD)

- Forward P/E: extremely high (over 100–450x) because analysts still expect modest earnings in 2026

- P/B (Price/Book): approximately 4.2x

- EV/Sales: approximately 5.1x

- EV/EBITDA: not meaningful (negative or low)

Key drivers in expectations:

- Growing demand from the defense sector (U.S. Army/Navy) for rugged edge AI computing

- Renewable energy data center contract (over $500k USD initial, potential for $1–10M USD, new sector)

- Better margins due to higher value-added products

- Book-to-bill ratio of 1.2x in 2025 → order backlog supports growth

Analyst expectations and consensus:

- Consensus rating: cautious Buy / Buy (3–4 analysts)

- Average target price: $10.00–$12.67 USD (potential upside of +16% – +55% from current price)

- Highest target: $13 USD

- Lowest: $9–12 USD

The company is valued significantly higher than the average tech/hardware company, as the market is pricing in strong growth potential in EDGE AI and the defense sector, which I believe is partly justified. The small size and low free float of shares cause volatility, and jumps can be exaggerated, declines painful, and volatility high.

Compared to the industry average (P/S often 1–3x), OSS looks expensive, but the high multiple reflects expectations for a turnaround in revenue and profitability. Future prospects are interesting, and the stock has been on my watch list for about a year. I opened my first position at €5.70.

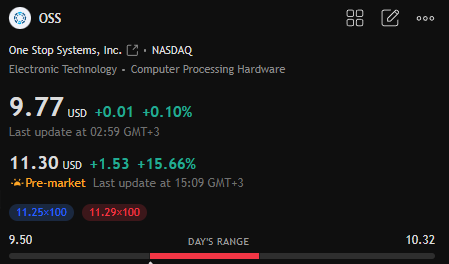

The stock usually jumps sharply on new order news, as it did today:

I will update this thread when I have more time and when more news becomes available. One definitely worth following tidbit at the end, which could be a significant driver especially towards the end of the year:

The Pentagon’s autonomous warfare unit, DAWG (Defense Autonomous Warfare Group), is seeking a considerable budget increase for 2027. In 2025, DAWG’s budget was $225 million, while the budget proposal for 2027 is 240 times higher, at $54.6 billion. This sum represents approximately 15% of reconciliation funding and will be used to acquire USV vessels, develop the “Hellscape” strategy, form drone swarms, and build other Autonomous Warfare Command entities.

If the budget proposal is realized even partially (it is indeed a proposal that can be heavily cut), major defense contractors such as LM, GD, RTX, and several drone companies will receive a significant portion of the orders. However, it also means immense demand for rugged EDGE AI computing and potentially for subcontracting firms like OSS, which already have US Army/Navy and pilot contracts underway.I would venture to estimate that even successful pilot agreements can offer significant follow-on contracts for a company wrestling in the microcap category. The market has, of course, already priced this in quite fairly within a year and continues to do so, but the realization of the massive 2027 budget proposal and the significant contracts it brings have not been fully priced in. The stock could be an excellent investment, especially if it were to drop sharply in late 2026 and the 2027 DAWG budget proposal were to pass in its magnitude. Due to its size, OSS has plenty of room for growth, even though multipliers often remain at the pain threshold for good companies throughout their growth.