This looks too good in terms of numbers. I have to suspect there’s a catch here. The analysis linked above states the following:

“We believe OMSE trades at a discount to peers for four reasons: (1) investors’ unfamiliarity with the platform, (2) rising concerns of a recession in the second half of 2025, (3) potential exposure to tariffs, and (4) the platform’s relatively small size compared to industry peers. Currently, oilfield technology companies trade at a forward EV/EBITDA multiple of 7.2x, while oilfield services companies trade at a forward EV/EBITDA multiple of 6.3x. In contrast, OMSE trades at a forward EV/EBITDA multiple of 4.2, based on our estimated CY2025 EBITDA of $54.38 million.”

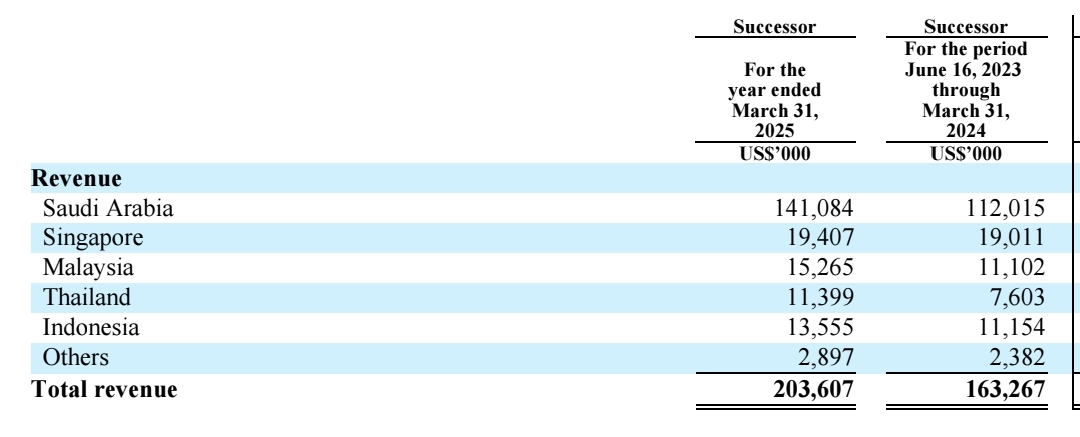

In addition, most of the revenue comes from a few customers. Saudi Aramco accounts for a whopping 67% of revenue, meaning the company is completely at their mercy.

“• Customer Concentration Impact. OMSE’s top ten customers accounted for 91% of total sales in FY2025, up from 88% in the prior year. Saudi Aramco alone contributed 67% of total revenue in FY2025, making it by far the single largest customer and a critical factor in the company’s financial results. While the company is proactively diversifying its customer base, the customer concentration will persist as a risk in the near term. Nevertheless, Saudi Aramco provides a robust validation of OMSE’s capabilities, critical to winning new customers.”

Time will tell if the company succeeds in holding onto these large customers. An attractive stock. Does the management have any connections to the Saudis?

I don’t mean it’s a scam, but that there are some risks here, which is why the valuation is so low. Risks that I, at least, don’t recognize.

edit: Well, that dependence on Aramco is quite a big risk. If they were to lose the contract for some reason, the whole case would lose its foundation.

Let’s calculate it this way: if that Saudi Aramco contract ended and all revenue from Saudi Arabia was lost. With this, the operating margin percentage would drop to 22% and still at today’s share price. The EV/EBITDA multiple would be 8.21. Of course, this would be a huge loss for the company, but there is still a margin of safety in this investment. In addition, those other markets have still been growing.

I’m not saying it’s a scam or that I personally find anything particularly suspicious about the company, other than the fact that I haven’t had time to delve into it yet, but Nordea immediately issues a pump-and-dump warning when pressing the buy button.

Perhaps it’s because it’s a stock that has fallen sharply and into the penny stock category, and has started to surge again.

OMS Energy Technologies inc and OMSE as the ticker. This is what Nordea’s trading platform says. It came as a surprise to me too. Or maybe I’m on a watchlist, even though I don’t easily go for lottery tickets

It seems to apply to all US stocks valued under $5. The limit might be something other than $5. I’ve encountered it, but I don’t remember with which stocks.

OMS Energy Technologies Inc. (NASDAQ: OMSE) announced that its subsidiary OMS Oilfield Services (Thailand) Ltd. secured a Technical Service Partner Contract with a Thai oil and gas operator. The contract covers technical consultancy, gauging management and hardware services.

The Singapore-based company manufactures surface wellhead systems and oil country tubular goods for the oil and gas industry. OMS Thailand operates two facilities in Songkhla and Sattahip, providing connection threading, repair and maintenance services for oil country tubular goods equipment.

The Songkhla facility has operated for over 20 years, while the Sattahip location has provided services for more than 10 years. Both facilities hold licenses to support the region’s oil country tubular goods sector across equipment from various manufacturers.

“We’re proud to expand our collaboration with a respected, major player in Thailand’s oil and gas industry, deepening our presence in this fast-growing region,” said How Meng Hock, Chairman and Chief Executive Officer of OMS.

OMS operates 11 manufacturing facilities across the Asia Pacific, Middle Eastern and North African regions. The company provides surface wellhead systems and oil country tubular goods to onshore and offshore exploration and production operators, along with premium threading services.

The information is based on a company press release statement.

My investment decision was based purely on numbers and cheapness. In short: a quality business, share price at the time of investment $3.58, cash approx. $2.25 per share, and EPS for the coming years approx. $1. So, with these multiples, the probability of losing money is small.

This stock sees big movements; it worked out quite well for me when I sold off my week-old shares on Tuesday. Mainly because, even though this looks really good in light of the numbers, my gut feeling tells me there’s something in the shadows. The largest owner’s “lock-up period” probably ended at the turn of the month, so for a while, I’ll calmly watch what that brings, if anything. Additionally, the unclear website and the CEO’s interview left a bad taste.

This joke came to mind when I was wondering about the stock’s undervaluation:

Two economists are walking down the street and pass by a hundred dollar bill without picking it up. A little while later one turns to the other and asks “was that a hundred dollar bill on the ground?” To which the other replies “nope, if it was someone would have picked it up already.”

I’m not really sure how to interpret that - as a defensive victory? Earnings and gross margin weakened, but the company defends this by stating that Saudi Arabia had an exceptionally high number of orders in early '25. Today at 2 PM Finnish time, a conference call is available on the company’s website.

According to the company, profit and revenue declined due to the normalization of “call-off” orders “The decline was primarily due to normalized call-off order timing versus unusually high volumes from a major Saudi Arabian customer in the prior year period.” A call-off order is, for example, when a K-store owner’s freezer breaks down unexpectedly, requiring someone to be called to repair it or bring a new one as soon as possible, as opposed to predictable ordering of spare parts or maintenance in advance/according to a maintenance program.

In my opinion, the good points were: Still good margins and strong cash flow, a new three-year contract with PTTEP, new contracts in Angola and Pakistan, and “activity” in Indonesia, Egypt, Oman, and the UAE → Reduces customer risk in the future (SaudiAramco is a very large customer).

According to management comments, the decreased result is not a consequence of weakening demand or OMS Energy’s business, but rather a “timing issue” with those call-off orders.

Great, I guess this will also bring my portfolio down by -15% to -20%, joining Evolution, Intrum, and Verve. Bad numbers, but it’s going well. Last year was just SOOO good that it can’t keep up for two years in a row.

Well, jokes aside. I haven’t properly read the report yet, but at the headline level, it’s neutral or negative. It’s not ruined by a high PE, but when revenue drops 50% from a year ago, even low multiples start to grow rapidly. Let’s hope that a broader customer base enables long-term and profitable growth. And that the CEO doesn’t dump their shares on the market despite the lock-up period ending.

This year we are likely to remain around ~$0.65 if the rest of the year goes similarly. For the six months ended September 30, 2025. Basic and diluted EPS. Basic and diluted earnings per share were $0.33. However, the company itself forecasts that it would reach around a dollar. “The company has projected an EPS of $1.0 for FY2026 and $1.09 for FY2027, with expected revenue of $220.75 million and $234.25 million, respectively.”

EDIT: Clarifying the above, the company is currently in FY2026, so the forecast is despite the name. And FY is apparently April → end of March. Confusing. The Q3 quarterly report was thus H1 2026.

There is plenty of cash, perhaps even a bit too much, unless there are some larger investment needs. Cash flow is also pleasingly in order, unlike with hype companies. “$26.4 million of net cash provided by operating activities for the first half of 2026”.