Larger companies deduct the change in inventory directly from material costs, so that it is not even shown as a separate line item in the income statement. If a similar change in presentation were made to Norrhydro’s income statement, then material and service costs would decrease for January-September 2025 and would increase for the comparison period. In this case, it would be seen that the costs attributable to the period grew significantly less than revenue.

5 Likes

Products are made from materials, so yes, they are also closely related to finished and work-in-progress products. The change in inventory is a crucial factor in evaluating the income statement.

A startup company starts from scratch. The progress of the period is monitored in real-time, day by day.

Day 1: Company is established

Revenue 0

Change in inventory 0

Materials 0

Other expenses 0

Operating profit 0

Cash 0

Inventory 0

Equity 0

Liabilities 0

Day 2: A metal bar is bought on credit for a hundred

Revenue 0

Change in inventory 100

Materials -100

Other expenses 0

Operating profit 0

Cash 0

Inventory 100

Equity 0

Liabilities 100

Day 3: A machinist makes a cylinder from the bar, which incurs a cost of ten, and the value of the inventory increases by the same amount

Revenue 0

Change in inventory 110

Materials -100

Other expenses -10

Operating profit 0

Cash 0

Inventory 110

Equity 0

Liabilities 110

Day 4: The cylinder is sold for 200 euros. The money from the sale is used to pay off debts

Revenue 200

Change in inventory 0

Materials -100

Other expenses -10

Operating profit 90

Cash 90

Inventory 0

Equity 90

Liabilities 0

In practice, we are more cautious, and after 3 days of machining, the inventory could be valued at 105 euros. In this case, the change in inventory would have been 105 and the operating profit -5. Similarly, the metal bar could be valued at a lower amount than its purchase price after acquisition.

7 Likes

Sales continue. Units sold 4000 + 43247 = 47247 pcs.

8 Likes

Volvo is setting up a new excavator plant nearby. Hopefully, we’ll get digital products into production there, or at least more demand for traditional cylinders.

6 Likes

It would be great if this were the case, so that one doesn’t have to go all the way to Malmö’s CEES unit to install NorrDigi.

But can someone answer, in what style Volvo (or some other company) sells excavators; how precisely customized for the customer?

-

Are they sold to known customers with the technology and accessories the customer wants? That is, does a potential customer contact Volvo, and then when deals are being negotiated, Volvo asks at some point, do you want the excavator with NorrDigi or with more traditional technology? And then when the customer has ordered a certain number of excavators with NorrDigi, does Volvo manufacture exactly that number for exactly that customer?

-

Or are excavators made more in such a way that a certain number of them are produced in advance - some with NorrDigi and some with more traditional technology - and then the customer chooses an excavator from the ready-made products, either with NorrDigi or without it?

If that factory is meant to produce 3500 excavators a year, then I would imagine at least some of them are manufactured in advance before a customer is known, and then NorrDigi would probably also be installed in some of the excavators already? But tell me if I’m wrong.

At least in Finland, machine sales are made with equipment chosen by the customer. That is, when ordering, you choose the equipment and wait for the machine to arrive. In North America, the customer drives into the yard, chooses a machine from a row, and takes it with them immediately. A very different style. In Finland, machine dealers keep small quantities of stock and demo machines, in the most popular size classes. Accessories are roughly determined by the export countries. So, if Volvo builds a factory in Sweden, intended to serve the Nordic countries and Europe, it is most likely that the standard equipment and accessory selection will include many things favored in the Nordic countries. For example, an auxiliary heater does not interest British and Central European manufacturers. Volvo probably had it as standard or had installation readiness as standard. The equipment list and standard features come from customer requirements, and that’s why Swedish manufacturers suit Finland, as they work in the same conditions and in the same style. Machine manufacturers for whom exports to the Nordics region account for 5% of their turnover are not very interested in whether they work in frost or how many work lights there should be.

I would guess that if NorrDig’s added value is a real customer benefit and there is customer demand for it here, it will quickly come from the production line. In sales, it is a big advantage that the standard product is the most suitable option for the customer.

6 Likes

Norrhydro appears to be a quintessentially Finnish company in all the negative aspects that almost invariably characterize the businesses and business ideas of this sullen and gray nation. It’s a domestic top product, and as a result of extensive R&D, a solution with competitive potential has certainly been achieved. However, the product’s sales are not invested in to the same extent as, for example, Swedish engineering companies do. The company has globally identified about twenty customers who could integrate NorrDig, and through that, the company could easily generate revenue.

The problem with this sales culture is the belief that a neutrally tested and validated product information brochure automatically handles the sales work, and that it has been perfectly executed once the 1-2-3 steps with the customer have been completed and the Salesforce ladder climbed up to the submitted offer.

In international integration trade, one has to burn several, several millions for a breakthrough. Finnish companies rarely have the desire or even the resources for this. Money must be spent almost like bribes, entertaining genuine influencers/decision-makers in international and high-earning organizations, just to even find the beginning of the path leading to a deal.

In NorrHydro’s situation, the best thing would be for an international private equity investor to buy the company and install a CEO in Trög’s place who would have new energy, risk-taking ability, and resources to overhaul the sales organization and shift gears. By announcing a rights issue, the company is jumping straight into the grave, waiting for the gravediggers to arrive and cover the pit.

15 Likes

I also came to the same conclusion some time ago. The lesson doesn’t come for free… The technology seems genuinely good, but the management/(owners) lack the drive to make a breakthrough. A similar company in the US with slightly more “Musk-like” management was 10x more valuable. And has made offerings this year too…

6 Likes

Trög also mentioned in the latest Inderes interview that NorrDigi’s revenue would still be around 10% next year. I don’t recall what targets were previously given for this, but it feels quite low, considering a large production facility was built in Rovaniemi with IPO funds.

The balance sheet is very tight, and surely some offering will still come to strengthen the cash position. I don’t know, but perhaps it would have been wiser earlier to make, for example, a directed issue to a large investor with the intention of properly commercializing NorrDigi. Now the share price has hit rock bottom, and perhaps for good reason, so money cannot be raised as effectively. If an offering comes now, it will likely just go towards continuing operations without a clearer change in strategy on how this innovative product could actually be commercialized. Surely there would be demand if the product is really as good as they say.

7 Likes

Norrhydro visited Pirkanmaa shareholders to introduce themselves. About an hour-long session and good information.

12 Likes

Good video! I’ll also highlight the slides from there separately regarding the commercialization of NorrDig, as it has been discussed. As someone following oil, the oil and gas industry seems like a lost cause, as oil prices are predicted to have a terrible run for the next couple of years.

The products seem excellent and competitive, but commercialization is progressing slower than an investor would like, and the cash reserves don’t allow much room for additional sales investments ![]()

18 Likes

Thanks for the video on my behalf too, I’ll raise a couple of thoughts from the video.

Positives:

- Yrjö commented on his share sales. He wants to lighten his ownership, but intends to remain the largest owner. I’m not concerned about his commitment to the company.

- ‘Eggs are not in one basket’: Six different categories were presented (see @Pohjolan_Eka’s previous message), which lowers the risk regarding sales success.

Concerns:

- At the 30-minute mark, it’s mentioned that the goal is to establish a global sales network within a few years.

- Even though ‘eggs are not in one basket’, quite a few categories are in testing or have had individual deliveries –> no guarantee of a breakthrough.

Considering the above points, it’s challenging to see rapid revenue growth from NorrDigi. Hopefully I’m wrong ![]()

9 Likes

Quite a positive video. If one wants to consider the interests of the company and shareholders, children should certainly not be taken onto the board. The role of the board is absolutely crucial for the success of the company, and every board member should have something to contribute in that role. That board cannot be a training ground for shareholders or family members, or it can be, but it can be costly for shareholders. Instead of having a relative learning on Norrhydro’s board, there could now, for example, be an experienced international marketing professional bringing added value. For the future of the company, it sounds good that the composition of the board will be re-evaluated.

11 Likes

Over a year ago, an agreement was made with the American company Aberdeen Dynamics for the exclusive right to represent NorrDigi MCC technology in the US oil and gas industry. On Aberdeen’s website, Norrdigi is prominently featured right at the top: https://www.aberdeendynamics.com/

How has this progressed, given that the last earnings report made no mention of the cooperation or revenue streams? If the product brings significant savings, one would think it would be sold even in a weaker economic climate.

5 Likes

Isn’t it quite clear in the materials above that oil and gas investments are practically frozen in the USA until prices rise?

1 Like

Actual oil production is at its peak, but investments in drilling equipment do not need to be made, as there is sufficient capacity available on that side, and service sector companies do not foresee a new boom or abundant cash flow, because the current oil price does not encourage a large number of additional drillings. Service-side companies are rather going bankrupt globally, including in the United States.

An easier comparison for Finns to understand would be, for example, the sale of a new innovative paper machine solution to Finland over the last 10 years. Not even a good solution helps if new investments are not necessary.

13 Likes

Indeed, that particular partner is exceptionally aggressive in an American style when promoting Norrhydro’s solution, so in this case, a large market was opened with quite moderate investments. Norrhydro does not have oil and gas industry professionals, so it’s probably not worth taking any overly strong market views there when such a good opportunity presented itself.

Just in time, a new comprehensive report ![]()

17 Likes

Iikka and Pauli chatted about Norrhydro, inspired by a comprehensive report. ![]()

Topics:

00:00 Start

00:14 Events after listing

01:46 Commercial development has been slow

04:31 Norrdigi EMA

06:13 Distribution agreement to the United States

07:30 Q3 was good

09:58 Recommendation is ‘add’, but risk is high

4 Likes

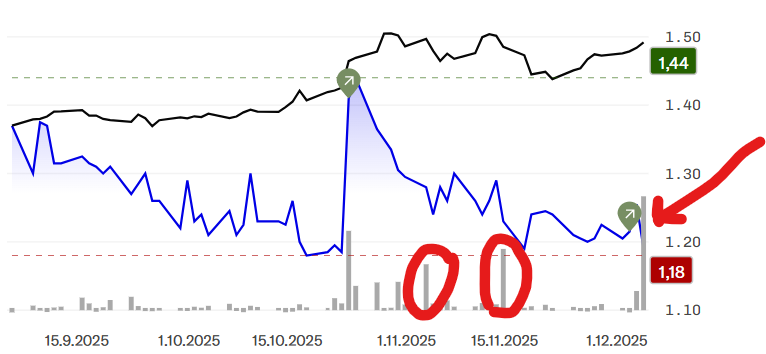

I don’t know for sure, but in previous trading spikes, Trög sold (and the stock price plummeted). And yesterday was the most traded day ever, if the IPO is not taken into account.

Could you clarify what this “good opportunity” is? Aberdeen Dynamics is a relatively small outfit that serves 10+ different industrial sectors, with oil and gas being just one of them.

I’ve mentioned this before, but it seems that the potential of these new technologies is quite heavily overestimated (even on this forum). Forum participants remember to praise the energy efficiency of the solutions, the growth potential of productivity, etc. (information, of course, comes from the company) without knowing more precisely how significant these factors are when the end customer makes their investment decision.

8 Likes

The high P/E doesn’t concern me as much due to weak earnings, but the somewhat high P/B does. Norrhydro’s P/B ratio is 1.6. This feels a bit high, as in my opinion, one shouldn’t pay over one for this due to the lack of demonstrated performance and also the high risk. A better “margin of safety” would be obtained by buying below book value, e.g., P/B 0.8, which would be a 50% lower price from about €1.2 → €0.6.

It wouldn’t be surprising if we get a stock exchange release in the coming days stating that Yrjö Trög has sold more shares, and this was the reason for the decline.

4 Likes