And an updated report:

13 Likes

Hydroline and Hydoring achieved positive results despite a decrease in turnover.

Hydroline has learned from its experiences, and the new CEO has taken charge; the results are visible.

Hydoring consistently delivers solid results and seems to have also made cautious investments with an eye on the future.

3 Likes

Those financial figures are clearly a turn in a positive direction.

Now we just have to wait and see if there’s enough momentum for the autumn to manage loans and fixed costs. Competitors are also making their own moves.

If we have to get by with just traditional methods, then growing the necessary and sufficiently profitable additional volume can be challenging.

2 Likes

Here are also Pauli’s comments on Norrhydro, regarding its orders and future, etc. ![]()

*We reviewed the order development of key customers in Q2, and overall we note that demand has developed favorably for Norrhydro. The data points support our forecasts, according to which Norrhydro Group’s revenue growth will accelerate in the second half of 202

9 Likes

The CEO continues dumping. This time, a large holding of 26,896 shares was reduced. Is there a price for the stock where the selling would stop? €1.26 was the lowest selling price.

7 Likes

Pauli met with Carl Mattson, the business director, who presented the digital business and the company’s solutions. ![]()

Topics:

00:00 Introduction

00:19 Business Director introduces himself

01:09 Digital business and Tampere unit

01:37 Digital multi-chamber cylinder

03:11 Energy-efficient electric cylinders

04:13 Commercialization

05:11 Synergy benefits in product development and sales

06:33 Electric cylinder presentation

15 Likes

I visited Norrhydro’s Tampere unit yesterday, where they focus on developing digital solutions. The products seem advanced and offer significant benefits to customers. However, anticipating commercialization paths is challenging, but it appeared that there is enough activity in that area and the focus has shifted specifically to the sales side. The weak demand situation in many customer sectors has partly slowed down the adoption of new technologies.

Attached are images and brief descriptions of the MCC and EMA solutions. The pieces shown in the images are intended for exhibition use, meaning they differ from the actual products, for example, in size.

NorrDigi MCC digitally controlled multi-chamber cylinder

The multi-chamber structure of the cylinder is visible through a hole made in the side of the sample piece

- Four-chamber structure enables 16-stage power adjustment

- In addition, energy can be recovered into pressure accumulators

- Together, these offer significant savings in fuel consumption

- Digital control improves accuracy

- Development of the MCC solution for Volvo excavators is in the final stages. Customers are testing the solution, and features are being refined based on customer feedback.

NorrDigi EMA electric cylinder

![]()

- High demand for cylinder electrification to eliminate oil spills

- Digital control enables extremely precise operation and programming of movements, which can be utilized, for example, in the development of autonomous machines and robotics

- Norrhydro focuses on large and challenging environment cylinders, where competition is low

28 Likes

Norrhydro surprisingly published Q3 figures? The company publishes figures semi-annually, but now a simplified Q3 review was released, showing revenue for the 9-month period up by 19.3%. We have a full-year growth forecast of 15%, and the stock is at an all-time low.

Norrhydro’s revenue grew by 19.3% during the period 1.1.-30.9.2025 compared to the previous year. The company’s revenue growth is clearly greater than the general market growth. With the growth in revenue, the company’s profitability improved. We continue measures for profitable growth in the company. During the financial period, we have continued to invest further in the development of Digital Norrdigi technology, as well as in sales and marketing. Operational activities have also continued at an excellent level.

27 Likes

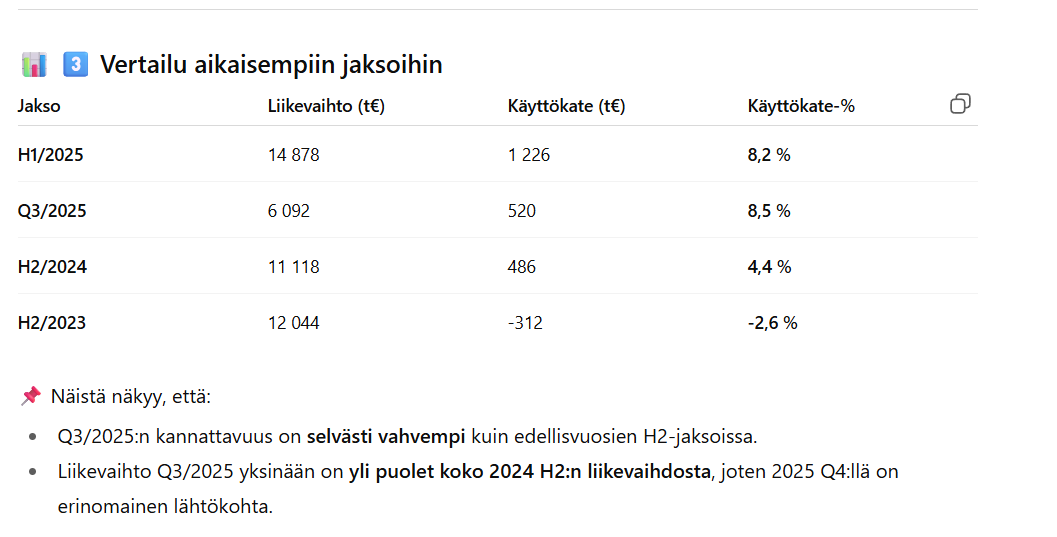

A somewhat surprising reaction, the Q3 result turned negative when H1 was positive, and revenue also seemed to decrease compared to Q1 and Q2. I can’t say about seasonal variations.

4 Likes

Decrease?

I got the following figures: In the third quarter of 2025, Norrhydro’s revenue grew by approximately 36%, which is clearly faster than the 13.5% growth in the first half of the year. In any case, a strong start to the second half of the year.

Paul’s forecasts for H2 were 16.7% growth.

7 Likes

H1 revenue was 14.9 million, 7.4 million/quarter. Q3 revenue was 6 million, which is almost 20% below the Q1 and Q2 average.

1 Like

I have previously owned Norrhydro, but I believe I realized a 30% loss perhaps two years ago when the direction didn’t seem to turn around at all. It’s great if there’s now demand for the products after challenging years.

From what I quickly glanced at the press release, unfortunately, the balance sheet is still very tight, and financing costs are unpleasantly eating into the bottom line. There’s a mere 119,000 euros in cash and 1.4 million in short-term receivables. Accounts payable and other short-term debt are significantly higher, around 5.6 million. Although long-term debt has decreased, it’s a slight concern that short-term debt has increased correspondingly. With such an empty cash register, it seems they might have had to use a credit line to keep operations running.

I’ve been wondering if it’s time to jump on the Norrhydro bandwagon, as the product is certainly necessary. However, that moment is not yet here, even though there was a small glimmer of light now. That amount of debt will continue to significantly erode return on equity in the future, and a lot of risk is baked into the stock.

5 Likes

Pauli has made a new company report on Norrhydro after Q3 ![]()

Norrhydro’s clearly stronger-than-forecast growth and profitability development in Q3 led to significant forecast upgrades for the coming years. This supports the strengthening of the balance sheet in addition to earnings-based valuation. The valuation, taking into account NorrDigi’s growth investments, already looks quite attractive, although it must be noted that estimating the long-term return on NorrDigi’s investments is very difficult. We raise our recommendation to Add (previously Reduce) and the target price to 1.60 euros per share (previously 1.40 euros).

Quoted from the report:

NorrDigi products, in turn, offer potential for rapid growth and, as operations scale, also better profitability due to higher sales margins. In this new segment, competition is at least for now limited. Significant uncertainty is associated with the realization and timing of NorrDigi’s growth.

15 Likes

@Pauli_Lohi interviewed CEO Yrjö Trög regarding the figures announced yesterday! ![]()

Norrhydro reported figures on business development for the January-September period, which showed strong growth and profitability development in Q3. CEO Yrjö Trög commented on the company’s updates in an interview with analyst Pauli Lohi.

Topics:

00:00 Start

00:24 Why did Norrhydro report in Q3?

01:20 Revenue growth

02:34 Momentum in different customer industries

03:07 Earnings development for the rest of the year

03:58 Guidance

04:50 Balance sheet utilization

05:29 Commercialization of Nordic

12 Likes

At least this surprise publication got the stock moving. Insiders got more liquidity.

https://www.inderes.fi/releases/norrhydro-group-oyj-johtohenkiloiden-liiketoimet-3

12 Likes

We might be at the beginning of a turnaround, but these two consecutive events (surprise Q3 report and stock sale) do not inspire confidence in the management, at least not in me. It was not a well-thought-out action.

10 Likes

I don’t know if this is idle speculation, but… Economica Yrityspalvelut Oy owns 34.86% of Norrhydro’s shares. Was it the case that Economica is wholly owned by Norrhydro’s CEO?

Trög was born in 1963, meaning he is 62 years old this year. So, about three years until the official retirement age. If I were that close to retirement age myself, I would certainly try to gradually reduce my ownership stake in the company. It would feel strange to still own a large share of the company when retiring.

On the other hand, though… if entrepreneurship is a way of life, one can continue as an entrepreneur even at 75 and beyond, as my uncle, born in the 40s, has done… But would one voluntarily do that at one’s own risk when one’s age starts with a seven? Hardly.

2 Likes

What if it was thought out? To me, that’s what it looks like more.

1 Like

It seems so.

For the undersigned, at least, the good Q3 numbers were acceptable. It feels a bit like Yrjö is pretty much all-in on this, and funding just has to be obtained from this for some other target x.

Oh, @Blackparta nicely listed the same thoughts below ![]()

![]()

1 Like