Alkusana

Foorumilta puuttui lanka Nordic Semiconductor:sta eli tuttavallisemmin Nordicista tai NS. Ei hätää, korjaan asian. Nordic Semiconductor on mielestäni hyvin mielenkiintoinen firma monellakin tapaa. Siinä yhdistyy korkea teknologia, merkittävä markkina asema sekä pohjoismainen kasvutarina. Onkohan kukaan täällä foorumilla tutkinut firmaa enemminkin?

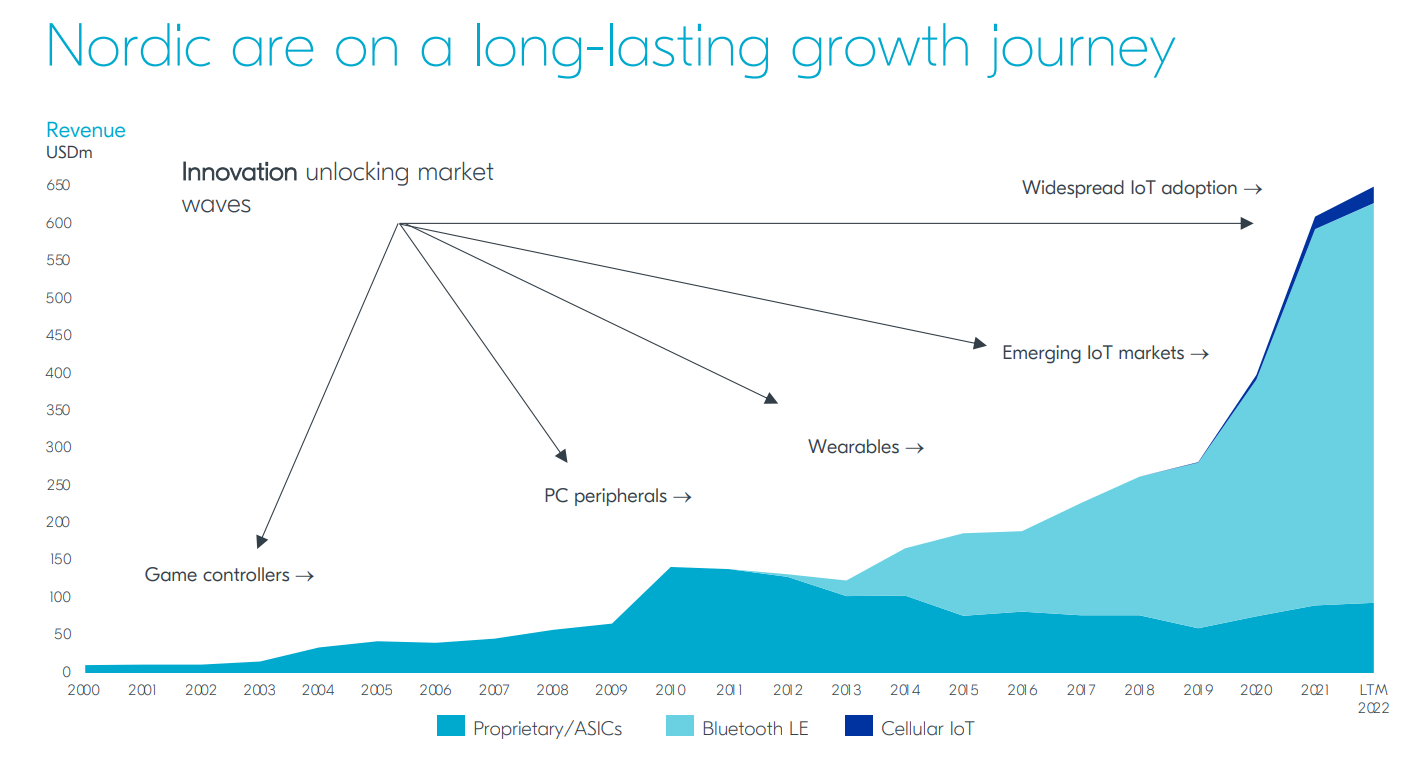

NS on yksi pienistä-suurista MCU valmistajista. NS ei ole lähelläkään suurimpia valmistajia kuten NXP:tä, TI:tä tai ST:tä absoluuttisessa metriikoissa mitattuna. Kirjotittamisen hetkellä NXP:n marketcap on ujo 40 miljardia, ST:n 24 miljardia ja NS:llä reilu 2 miljarida. NS:llä on kuitenkin ässä hihassaan: poskettoman hyvä radio-IP joka on jalostettu maailman luokan Bluetooth radioksi ja sitä kautta tuotteistettu nRF51, nRF52 ja nRF53 mikrokontrollereiksi. Tämä on johtanut markkinatilanteeseen jossa NS:n kokoisella firmalla on 42% markkinaosuus BLE (Bluetooth Low Energy) MCU markkinasta. Ei tarvi olla nero huomatakseen että jotain on tekeillä kun alan pienellä toimijalla on leijonan osa markkinasta, jonka povataan kasvavan raketin lailla seuraavan vuosikymmenen aikana.

NS tuoteet

NS:n tuoteportfolio jakatuu 5 osaan.

-

Propietary ASICs:

Historiallisesti custom radioratkaisut olivat NS:n syömähammas noin 10v sitten. Nykyään tämän kategorian tuotteet ovat suhteellisen pieni osa koko yhtiötä. Usein tälläiset ratkaisut eivät ole julkisia referenssejä, mutta ymmärtääkseni Logitech Unified Receiver kuuluu tähän kategoriaan (Noric siellä on sisällä, mutta onko custon ASIC vai geneerinen radioratkaisu on kyseenalasita). Kyseessä on siis laite jolla Logitechin langaton hiiri tai näppis yhditetään tietokoneeseen pienellä tapilla joka laitetaan tietokoneen USB porttiin kiinni. -

BLE:

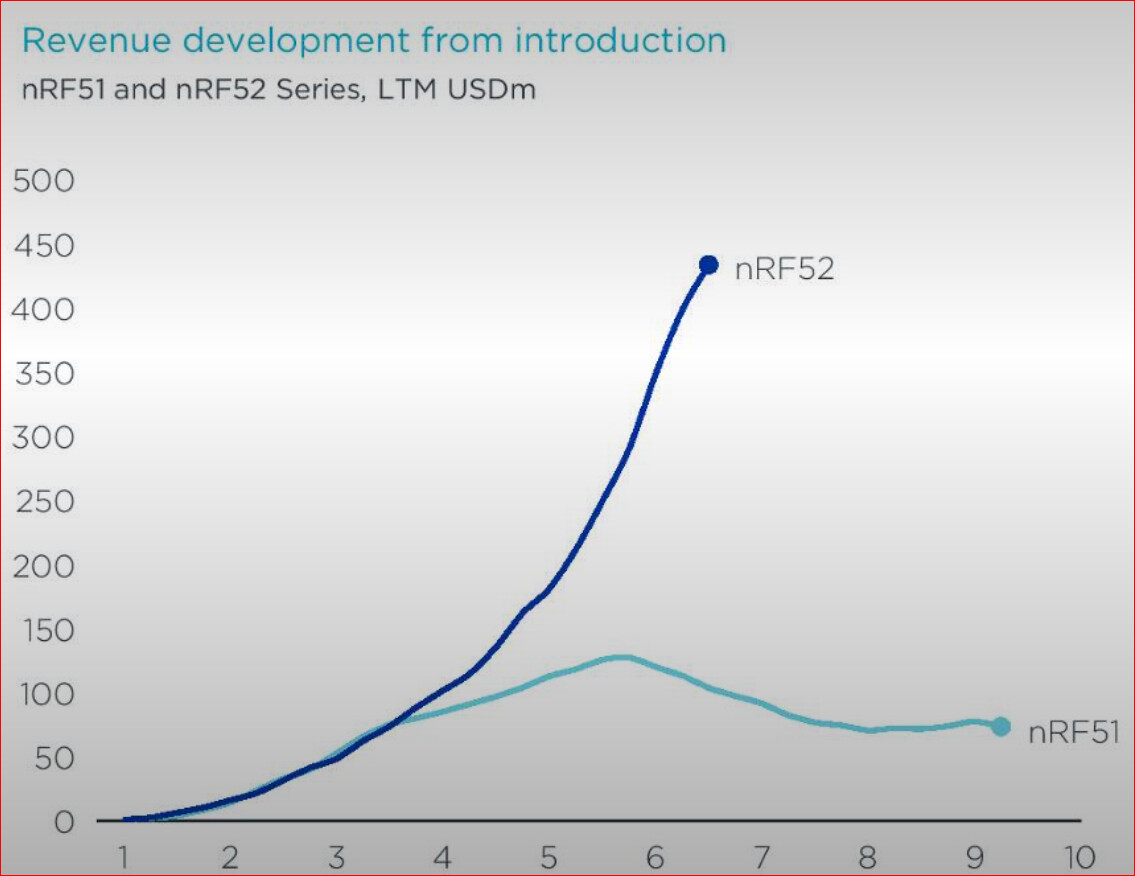

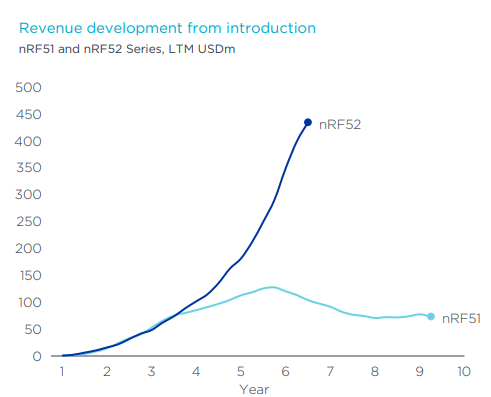

BLE on NS syömähammas ja merkittävin kasvun lähde. Nordicin ensimmäinen BLE tuote oli nRF51 sarja. Tuote toi NS kehittäjien tietoisuuteen ja aloitte luottamuksen rakentamisen kehittäjien ja NS:n välille. Tuote oli aikoinaan merkittävä sillä se yhdisti yhteen pakettiin kyvykkään mikrokontrollerin ja peripheraalit, matalan virrankulutuksen sekä BLE radion. nRF51 oli ensimmäinen julkaistu tuote ja sitä seuraava nRF52:ää voidaankin pitää matureteetin saavuttaneena parempana nRF51:nä. nRF52 on isompi, tehokkaampi ja vähävirtaisempi kuin edeltäjänsä. Molemmissa piireissä on yksi ARM ydin jonka päällä sekä radio että aplikaatio pyörii. Laite kaipaakin toimiakseen softdevice eli software devicen osaksi binääriä. SD pitää sisällään nimeomaan radiocoren. Koska radio ja applikaatio jakavat prosessorin johtaa se mielenkiintoisiin tilanteisiin kehityksen kannalta. Varsinkin kuinka muisti ja Flash jaetaan. Myöskin debuggerilla koodin steppaaminen riviriviltä BT:n ollessa päällä kaataa laitteen ennemmin tai möyhemmin. nRF52 ei ole täydellinen mutta pirun hyvä kompromissi monen asian suhteen. Varsinkin ultra-low-power segmenttiin se soveluu hyvin sillä muutamalla AA paristolla laite toimii BT beaconina vuosia. Suomalaine RuuviTag käyttää nRF52 piiriä. Siinä on läjä sensorita ja BLE. Valmistaja lupaa useamman vuoden toiminta-aikaa yhdelle paristolle. Toki * merkin kanssa. mRF-sarjan uusin jäsen nRF53 sen sijaan on merkittävästi erinlainen kuin edeltäjänsä. nRF53 sisältää omat prosessorit radiolla ja applikaatiolle. Applikaatio core on myöskin hieman tehokkaampi kuin nRF52:ssa. Piiri on vielä melko uusi markkinoilla ja sen myyntitilastoista ei ole vielä luotettavaa dataa.

Allekirjoittaneella on reilu vuosi aktiivista työelämäkokemusta nRF52:sta. Nykyään nRF52 toimii harrastehommissa päätoimisena alustana. Tästä tulee joskus Gittirepo jonnekkin kuhan projekti on sellaisessa tilassa että sitä viitsii näytellä. Saa sieltä sitten kurkkia miten nRF52:lle tehty koodi ja arkkitehtuuri näyttää.

Kuten kuvaajasta näkee on nRF51 ja nRF52 myynnit selkeästi kehittyneet ja nRF52:n tuoma maturiteetti on vastaanotettu hyvin markkinoilla.

-

Cellular IoT:

Cellular IoT on tulevaisuudessa merkittävä kasvava trendi. NS julkaisi nRF91:n viime vuonna. Tuote on kuin nRF53, mutta BLE radion sijaan siinä onkin LTE radio. Laite saavuttaa samat vähävirta ominaisuudet kuin BLE verrokkinsa. Tulevaisuudessa NS:n arvostuksesta suuri osa on cellular IoT:tä. -

PMIC:

NS julkaisi viimevuonna nPM1100 PMIC:n (Power Manager IC). Kyseessä on varsin kyvykäs DC-DC PMIC joka on suunniteltu toimimaan juurikin muiden NS:n tuotteiden kanssa. Piiri on suunniteltu mataliin virtoihin ja hoitaa myös mahdollisen akuston lataamisen sekä sopii hyvin älykkääseen USB-linjaan. NS:n tavoite tuotetta suunnitellessa oli kasvataa NS:n komponenttien pinta-alaa piirilevyllä. Tuote on ns companion tuote aikaisemmalle portfoliolle. -

WLAN:

WLANsta on paha sanoa mitään kun sen julkistus pitäisi olla tänä vuonna H2:n aikana. Eli about kohta. NS osti Intialaisen WLAN designiin erikoistuneen suunnitelutalon jokunen aika sitten. Kysessä olisi ensimmäinen tuote joka tulee tästä hankinnasta ulos. Olettaisin että NS haluaa kierrättää vanhaa IP:tä, jolloin arvioisin kyseessä olevan nRF53/nRF91 klooni mutta niin että radio on WLAN radio. On tosin myös riski että Intialainen firma käyttää siinä enemmän omaa katalogiaan jolloin lopullinen tuote olisi jossain määrin erinlainen kuin NS:n muut tuotteet. Aikoinaan NS tunnisti bisnesmahdollisuuksia ja tämä oli eniten sopivassa kulmassa siihen nähden.

Markkinaympäristö

NS:n markkinympäristö on mielenkiintoinen. Suoraa verrokkia NS:lle ei mielestäni ole. On olemassa muutamia jotka ovat tarkistelemisen arvoisia:

-

Espressif ESP32:

ESP32 on Kiinalainen MCU perhe joka EI käytä ARM corea vaan sen sijaan heidän omaa RISC-pohjaista prosessori arkkitehtuuria tai nykyään muutamassa uudessa tuotteessa RISC-V ydintä. Kiinalaisissa siruissa on globaalisti ajateltuna hieman riskiä tietoturvan, geopolitiikan ja maineen kannalta. Lisäksi nämä piiriet eivät ole kamalan virtatehokkaita eli eivät sovellu paristo/akkutoimiseen sovellukseen kuten esimerkiksi langattomiin kuulokkeisiin. Näitä piirejä löytyy vaikka ja mistä Kiinalaisista kulutuselektroniikan laitteista. Nopeasti ainakin Roboroc robotti-imureissa on ESP32-piirit. Roboroc on Xiaomin tytäryhtiö. Xiaomi on valtion ohjauksen alainen firma. Espressif on melko samaa kokoa kuin NS. Selkeästi juniori alalla. -

Texas Instruments

TI:llä on läjä erillaisia BT radioita. Näistä en tiedä kamalasti. Tiedän että jotain mallia käytetään Libre 2:ssa. Lisäksi TI julkaisi hetki sitten melko lähellä NS:n katalogia olevan CC12405R:n. TI:stä merkittävä huomio on että talo ja sitä kautta puolijohdeportfolio on massiivinen ja laaja tehotransistoreista prosessoreihin, instrumentaali vahvistimiin ja MILSPEC komponentteihin. Suorastaan jättiläinen. Ison talon on vaikea vastata kaikkiin vertikaaleihin. TI:tä kannattaa seurata jatkossa. -

STMicroelectronics:

ST:n BLE tuoteperhe on nimeltään STM32WB. Se on muutamasta mallista kooostuva mallisto joka on hyvin samankaltainen nRF53:n kanssa sillä WB sarjan prosessoreissa on kaksi ydintä. Yksi applikaatio ydin ja yksi radioydin. Huomioitavaa on että ST:n BLE radio ei ole heidän oma vaan se on ostettu IP blokki (muistaakseni) Infineolta joka puolestaan on ostanut hyvän osan tästä (muistaakseni) Muratalta. Tämä johtaa ikävään tilanteeseen jossa kommunikaatio tapa applikaatiotilan ja radiotilan välillä on kovin rajoittunut tehden siitä hieman bugisen kokonaisuuden varsinkin kehittäessä. ST on suuri general purpose MCU valmistaja varsinkin teollisiin kohteisiin. Mikäli itse suunnitelisin piirilevytoteutuksen joka ei vaadi BLE radiota valitsisin STM32-sarjan prosessorin 9 kertaa 10:stä. Noin vuosi sitten oli huhua että ST saattaisi ostaa NS:n. Se homma ei siitä sen koomin kehittynyt. -

NXP:

NXP:stä en saa hirveästi sanoa. Heillä on jonkinnäköinen BLE portfolio. Heillä on samat haasteet kuin ST:llä ja TI:llä että ovat jättiläisiä eivätkä voi tai kykene hoitaa jokaista vertikaalia. Joku voisi auttaa NXP:n tutkimuksen suhteen mikäli mielii.

Muista huomion arvoisia asioita:

-

NS on ns. fabless yhtiö ja valmistutaa piiristä TSMC:llä ja käyttää ainakin nRF52 sarjassaan 55ULP teknologiaa. Muutkin luultavasti käyttävät joko samaa tai ehkä generaation pari uudempaa versiota. Tämä tarkoittaa että NS ei itse hallitse erikoistilanteissa omaa tuotantoaan. Varsinkin koronan aikaan ja jälkeen tämä on ollut ilmeistä.

-

NS:n tämänhetken arvostus perustuu jäätävään kasvukertoimeen ja siten muuttuvassa macroympärsitössä on kovin paljastettu suuriin muutoksiin käyvässä kurssissa.

-

NS:n päämarkkina on asset tracking, person tracking, consumer electornics ja beacon markkina. Internet on täynnä erillaisia maksullisia analyyisejä kuinka markkina kasvaa. Usean tuhannen euron maksumuurin takana nämä ovat melkoisen kallis tiedonlähde. Yritin dippatyötä tehdessä puhua itselleni kopion eräästä raportista. Matalin hinta jonka tarjosivat oli 500e. Tässä esimerkki eräästä: https://www.verifiedmarketresearch.com/product/bluetooth-chips-market/?utm_source=Designerwomen&utm_medium=016. Jos joku haluaa laittaa verotuksessa ammatikirjallisuuteen rahaa niin joku tämmönen on varmaan aika hyvä siihen