The same thing happens day after day. The so-called baseline price level just seems to be a little lower all the time. Whenever the Helsinki exchange (Hesuli) closes, the price usually claws its way back up.

2 Likes

At least we are no longer tracking Ericsson ![]() There is no sense in sliding down along with Ciena or Lumentum either, given such a different horizon. Hopefully, it will drop back to the safe €5 range in the earnings report and stay there for a while, as a large amount of cash will be freed up for me at the beginning of next month. Based on my own calculations and estimates, I might dare to start buying at this price, even though I’ve been reserved about those €13–15 price levels.

There is no sense in sliding down along with Ciena or Lumentum either, given such a different horizon. Hopefully, it will drop back to the safe €5 range in the earnings report and stay there for a while, as a large amount of cash will be freed up for me at the beginning of next month. Based on my own calculations and estimates, I might dare to start buying at this price, even though I’ve been reserved about those €13–15 price levels.

Nokia would need a comparable operating profit of ~€5 billion for €15 to be justified, with a P/E ratio of about 20, though one can always ask if a P/E of 20 is justified in either direction. I think we can all agree that the comparable operating profit for 2028 will be in the €3–3.5 billion range. Not quite enough.

2029? The expansion of San Jose and the potentially exponentially growing Cloud + AI demand will start to be seen more broadly. Orders received in 2027–2028 can be booked as operating profit in 2029. Defense will have time to generate more demand starting in 2027 when the first version of the world’s best edge AI is released to the market, perhaps seasoned with NestAI. Likewise, AI RAN will hopefully start selling by then, starting in 2027. Radios hung on masts in 2020 will be reaching the end of their service life in 2027–2028, so perhaps we will at least see orders. Operating profits for 2029?

After 5G arrived, both Ericsson and Nokia saw an operating profit growth of over €1 billion when comparing 2018 and 2022. Taking inflation and likely lower 6G demand into account, could we be at similar figures by 2032? Or perhaps even earlier, if operators are convinced by both the Nokia and Nvidia narrative and Nokia’s dual-purpose radio for the 5G->6G transition phase. I like the partnership mostly because the market machinery of a company the size of Nvidia will be supporting the sales of Nokia’s radios in the future.

The prospects for the future are quite good, in my opinion. If the share price rises from €10 to €15 over 3–4 years and you get dividends on top of that, isn’t that pretty good already? And of course, the potential for positive surprises from Defense and other smaller projects is in the background, adding spice to the stock’s performance. And we shall see when the market realizes that Nokia is no longer a HW (hardware) house on the mobile side. For better or for worse.

9 Likes

Declines of at least 4%: Nokia, Ciena, Arista, Lumentum, Micron, HPE, Dell.

It’s not just about Nokia.

10 Likes

What sets Nvidia apart from the aforementioned? They all supply components to the AI/Data Center sector, but Nvidia doesn’t drop significantly…![]()

3 Likes

Nvidia’s 2026 P/E is just over 23, which is low for AI chips. Additionally, the stock’s rise this year has been moderate, at just over 13%. These are superficial observations; then, of course, there are reasons related to the company’s business, which I don’t know well enough to comment on.

Regarding Nokia’s decline:

When peers are also falling, it is positive that Nokia is not seen as a bad company, but rather that this is a sector-specific correction that will eventually stop and change direction. Nokia has lagged behind, and its price, often perceived as expensive, is explained by the fact that its strongly growing AI and cloud order book has not yet had time to materialize into sales and profits. For Nokia, 2026 is a transition year during which the AI and cloud order book will take center stage; next year, both orders and sales will be in the spotlight.

7 Likes

Nvidia+Nokia= “radio networks are turning into global AI supercomputers” Quite well put.

3 Likes

Nokia’s future outlook has changed radically even compared to a couple of years ago, when people were still speculating whether they might have a shot at entering the data center market. The acquisition of Infinera cannot be overstated. I hope the synergy benefits have been underestimated—and perhaps they have—since the combined package of Nokia + Infinera in the optical space, to be released next year, is precisely that synergy, and AI+Cloud is growing faster than anticipated. And then there are the potential market share gains you noted, driven both by competitive products (InP, ICE-D, etc.) and by our competitors’ bottlenecks. And, on top of that, the end-to-end data transmission advantage that might one day materialize.

My gut feeling is that Nokia’s valuation, when calculated as the sum of its parts, is roughly accurate compared to its competitors. However, Mobile is still seen as dead weight on the cusp of a renewal cycle and 6G. Of course, there is a significant risk in pitching a new strategy to conservative telecom operators, but let’s see what happens when Nvidia’s salespeople start wedging their faux-leather shoes into the operators’ doors. I wrote earlier that Nokia’s approach from a defensive standpoint is the only correct one, at least in my opinion.

We are indeed living through a transition year. I wouldn’t celebrate even in 2027 yet, at least not in these markets. By 2028, we should start seeing more than just orders and future visions on the bottom line. I believe and hope that there is faith and demand for the future visions of Nokia—and Nvidia—from the buyers of the products as well. Right now, both Mobile and a large portion of future investments are leaning on the same vision as, say, IoT back in the day, when it inflated the markets with its hype. In the 6G era, that should be possible again, but no one talks about it anymore. Let’s see if everything goes well or if we all return to our roots and apologize to our bosses for our cheeky early retirement plans once the champagne bottle has been emptied.

7 Likes

Nokia is a late bloomer in the AI market; a high P/E does not automatically mean overvaluation

Nokia’s rise in relation to AI is a relatively new phenomenon, and its stock has not multiplied from its 12-month lows anywhere near the levels of its AI infrastructure peers. This slow start is an advantage in terms of upside potential: while other AI stocks have already reached high levels of AI sales relative to total revenue, as a latecomer, Nokia is only just getting up to speed.

As Nokia’s order backlog related to AI and cloud services grows, the resulting revenue and earnings will materialize primarily in 2027 and beyond. This delay makes Nokia’s P/E ratio for this year look high on paper, even though both revenue and earnings are on a very encouraging trajectory.

Furthermore, Nokia reported in its Q1 earnings call that its AI & Cloud segment’s target market is growing at a 27% annual rate (CAGR), which means the market will double every three years. At the same time, many of Nokia’s early-mover competitors are increasingly suffering from supply constraints. This industry-wide capacity bottleneck paves the way for a well-positioned latecomer like Nokia to secure market share and gain significant ground as AI investments continue to grow, according to a recent Morgan Stanley study.

Markets price in future earnings, not current ones. As a company enters a new growth phase, the share price often adjusts before the associated profits are reflected in reported earnings. This temporarily pushes the P/E ratio higher.

Nokia thus arrived late to the AI party, and its P/E is elevated as a result. Once AI-related sales have grown sufficiently, the P/E will also settle at a more moderate level. At this stage, Nokia almost necessarily must have a relatively high P/E ratio to reflect its strong momentum. A price drop in line with more mature and much higher-valued AI companies is not a necessity, provided that Nokia’s growth story stays firmly on track.

10 Likes

Picked from Kauppalehti’s “protest list”:

“Nokia briefly arrived at the AI party, even though 90 percent of it is something other than AI.”

My response to that: In Q1 2026, Nokia’s AI and cloud orders were one billion euros, while net sales were just under 4.5 billion. Let’s do a quick calculation: 1000 million / 4497 million = 0.22237. In the first quarter, the ratio of AI and cloud orders to sales was 22.2%.

As I have said, Nokia’s AI growth will only show in sales and profits with a delay. This year, the number of orders is what counts.

13 Likes

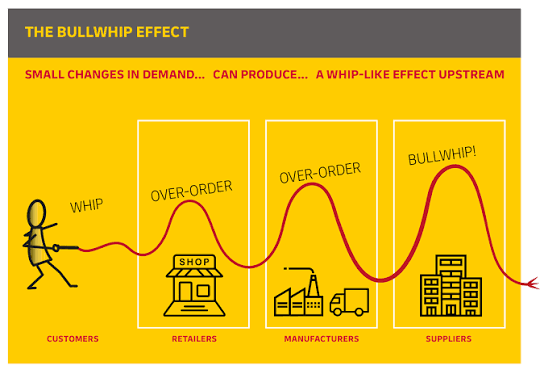

In my opinion, a classic case of inventory stockpiling caused by speculation is forming in the AI sector. In inventory speculation, the Bullwhip effect manifests at the end of the value chain as an initial rapid growth in orders, as every link in the value chain tries to ensure the availability of components and orders goods to their inventory just in case. It is better to pay too much for the goods than to be left without them entirely. However, demand based on speculation has a way of collapsing.

The further along you are in the value chain, the greater the fluctuation up and down, because the growth in demand caused by speculation compounds throughout the chain. Nokia is likely not in the worst position, but it is quite far along in the chain. Chip manufacturers are likely the biggest targets of this speculation. A year from now, warehouses will be overflowing with chips that have no use. This is a prediction, and I am accepting beer bets to see the results in 07/2027.

6 Likes

Here are Atte’s comments on the AI-RAN solution ![]()

Nokia announced on Wednesday that it is releasing the industry’s first commercial AI-native radio access network (AI-RAN) solution. The announcement is an expected step, as the company had previously disclosed its collaboration with NVIDIA in this area. Put simply, the new solution makes mobile networks smarter and helps operators squeeze more data capacity out of the spectrum they already own, without the need for constant hardware upgrades. If successful, the software-based subscription model would bring more stability to Nokia’s Mobile Networks business instead of the large investment cycles seen previously. The solution is expected to be commercially available in 2027, and realizing its benefits will require a significant amount of development work. However, it will only be clear in the long term how broadly operators are ultimately willing to invest in AI-based radio networks, and whether the products can be made sufficiently competitive in terms of costs and energy efficiency.

8 Likes

“Billion-euro AI and cloud orders should not be compared directly to one quarter’s revenue, because orders are recognized over several quarters or even several years. However, they do indicate demand and future revenue. Therefore, regarding Nokia’s AI growth in 2026, the most essential factor is specifically the order intake – its impact on sales and earnings will be seen with a delay.” (AI included in the formatting)

At this stage, no one can estimate whether the order intake in the billion or over-a-billion range will continue in the future. Only then could one consider that 22% share of sales. At the moment, the realized share of revenue is likely what was presented by Kauppalehti. Director Hotard will surely tell us in a week where things stand.

2 Likes

Opinions are nice and all, and even nicer when they are based on more than just gut feeling. This article might have been posted here already, but repetition is the mother of learning:

“Optical component manufacturers are expected to expand production capacity by approximately 12 times between 2025 and 2030, yet supply will remain roughly 50% below demand through the end of the decade, according to Rosenblatt’s proprietary supply and demand model.”

5 Likes

As an additional comment, in the previously linked Light Reading interview, Nokia representatives (Atkinson and Mahajan) promised that GPU-based products will remain competitive in terms of cost and power efficiency compared to the current Marvell-based ones, without any additional cost or power consumption. Furthermore, Atkinson described the transition as the final architectural decision for the baseband (custom chips are ending, ABIP is the last one), while radio units (Habrok) will continue to use Marvell, although their future is still open regarding the 2028 generation.

Finally, the importance of this matter, both technologically and commercially, can be emphasized so that Nokia’s low-margin radio networks can achieve a much more profitable business model. According to Hotard, AI-RAN is “the biggest innovation in the radio industry in decades.”

@Old_Baker The change is exactly as radical as I summarized above. From the article:

This all seems to mean the time is nearly up for Marvell as a vendor of custom silicon for Nokia’s central units and distributed units – the appliances and servers responsible for baseband. “We are making now the final pivot from a custom silicon baseband strategy to a merchant silicon baseband strategy,” said Atkinson. “So, ABIP will be the final custom silicon product which we will bring to market.”

9 Likes

Let’s see if this is enough for the market:

“The world’s largest manufacturer of physical processors, TSMC, posted record results in the second quarter, beating already high analyst forecasts. TSMC’s net profit was 706.6 billion New Taiwan dollars, or approximately 22 billion US dollars. Analysts had predicted a profit of 623.7 billion New Taiwan dollars.”

3 Likes

Today, 06:18

Share

DNB Carnegie downgrades Nokia to sell (hold), reiterates price target of 8.40 euros

Finwire News Agency

6 Likes

Yesterday brought good news, yet the stock still went down. I thought it would probably correct itself today, especially since it seemed to recover a bit in the US towards the end.

I saw that Iltalehti news piece and was wondering if it would be up by 4 or 5% today. Well, it’s down. People seem to be in quite a panic. I guess there’s no faith that Nokia will benefit from the nVidia deal at all, seeing as we’re almost back to the share price at the time the deal was signed. ![]()

7 Likes

Looking at Yahoo Finance right now, it doesn’t look like a pleasant opening in the US for Nokia and other AI stocks. Let’s hope that we are nearing the end of this downturn soon, otherwise it might get just as boring as previous years.

2 Likes

Results don’t seem to be affecting AI stock prices right now. Tomorrow, however, a large pile of options for many companies will expire. Max pain levels are generally higher for all of them, but who knows about these things…

3 Likes