One picture says more than any press release.

23 Likes

Pressi:

Nokia upgrades Symphony Communication’s MCT subsea network to deliver advanced connectivity across Southeast Asia

18 Likes

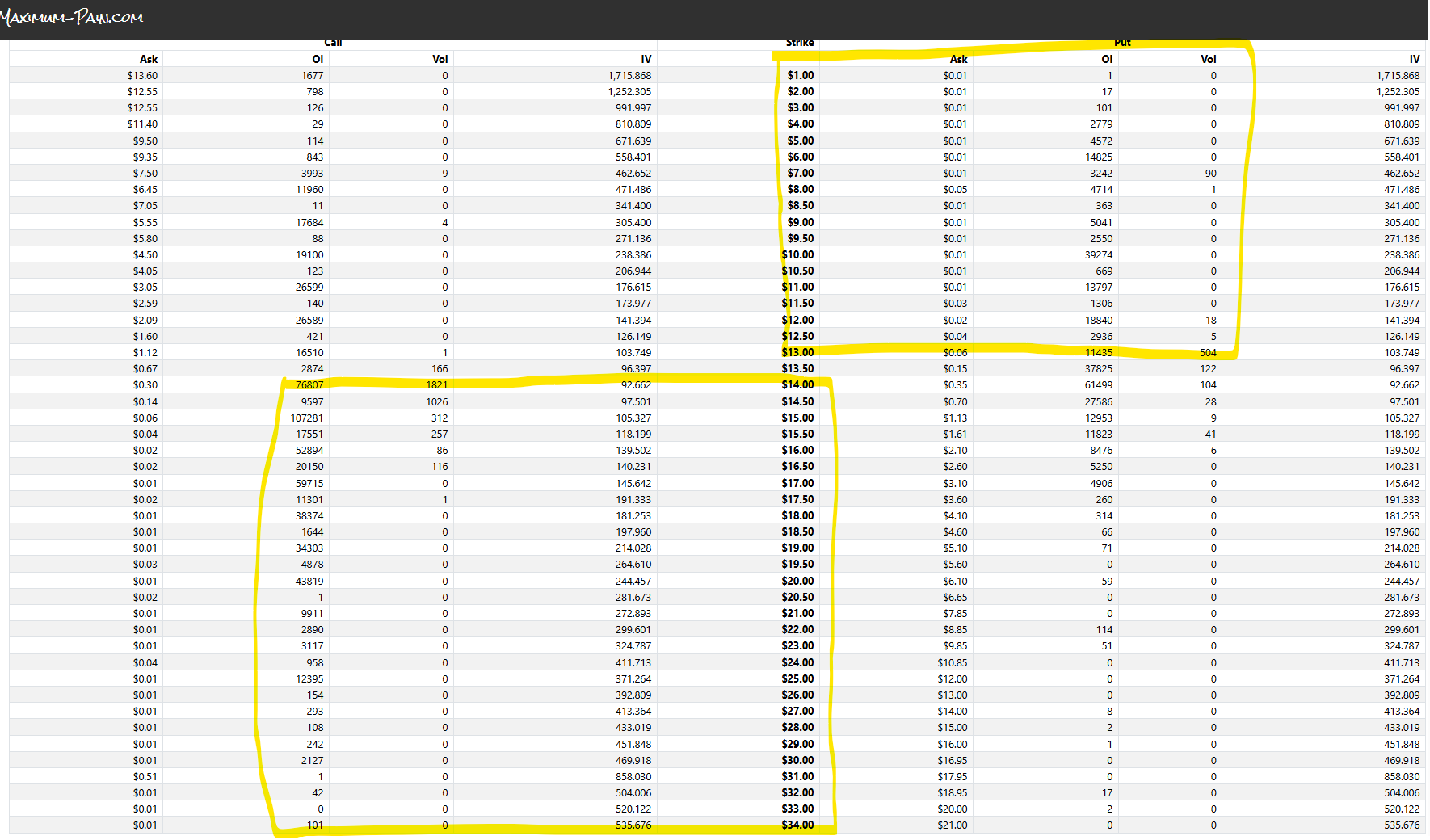

Friday saw quite large volumes in options, meaning we won’t be rising before the weekend (as the US open perhaps suggested ![]() ). It really looks like some MM (Market Maker) activity right now; a large portion of puts and calls are being rendered worthless.

). It really looks like some MM (Market Maker) activity right now; a large portion of puts and calls are being rendered worthless.

There are 510k calls at $14 or above, which corresponds to 50m shares ![]()

![]()

There are 225k puts at $14 or below, equivalent to 22.5m shares.

11 Likes

Some fear a negative profit warning, while others hope for a positive one. This is what was stated in the Q1 report:

We now expect Network Infrastructure revenue to grow by 12–14% for the full year 2026, and the Optical Networks and IP Networks businesses to grow by a combined 18–20%. We are increasing our investments in the Optical Networks business to maximize our opportunities in this rapidly evolving market.

As a result of these, our comparable operating profit currently appears to be settling slightly above the midpoint of our 2.0–2.5 billion euro guidance range for the full year.

The more investment in production capacity, the weaker the operating profit this year and the greater the profit potential in the coming years. 2026 is the year when growth is being prepared for the following years. Last year’s capital expenditure (Capex) was 606 million euros, while the guidance for this year is 900–1000 million.

As I have stated, orders from AI and cloud customers are the most interesting thing to watch this year, rather than sales or profit, as the latter are still in the acceleration phase. Speculating about positive or negative profit warnings might be interesting, but it is quite futile considering that 2026 is a year of significant growth investments.

6 Likes

It would be nice to see a poll about that here in the community.

This showed up: Nokia kasvattaa 6G- ja puolustusverkkojen tuotekehitystä Suomessa Business Finlandin tukemana

15 Likes

3 Likes