For hardware manufacturers, the AI market is currently equivalent to at least the 90s mobile phone market and the building of those networks. In that sense, talking about a bubble is misleading, as data centers are actually being built at an accelerating pace, meaning equipment suppliers’ order books are genuinely swelling; therefore, this is not a bubble comparable to the dot-com era.

Of course, a period like this creates AI hype in marketing, so an “advanced AI” label is slapped onto everything possible, even if the company is just one AI user among many.

1 Like

Nokia is fortunately on the right side of the earnings chain. However, looking at the financial development of Amazon and Google, I can’t help but wonder how they are allowed to operate at this level of risk. Either it is absolutely certain that this is a winning recipe, or otherwise, they are headed for trouble. And even if this is a winning tactic, it’s somewhat baffling how such a gold rush is happening or being allowed to happen. The money is running out. And now they are trying to shift the bill to retail investors—I wouldn’t be surprised if smart money has started moving to the sidelines or at least reduced risk levels (and they are laughing, for example, when some pay a 2 trillion valuation for SpaceX). Phew. Not everyone is a winner when a rush occurs.

Out of these hyperscalers, Microsoft looks the healthiest to my eye, at least regarding cash flow. For the others, cash flows are screaming a red warning. Of course, Microsoft is also starting to have a fair amount of debt, though not relative to its market cap. ![]() The money issue is very critical right now; perhaps the markets are now waking up to it. The SpaceX IPO seems to me like one more cynical way to transfer wealth. And it’s becoming an essential factor in this plot. If I understood correctly, even Google made a big deal with SpaceX, but the contract has an option to terminate very quickly as early as October. Well, well—doesn’t that smell a bit!? And the same capacity was sold to Anthropic with an even bigger deal. Hmm..

The money issue is very critical right now; perhaps the markets are now waking up to it. The SpaceX IPO seems to me like one more cynical way to transfer wealth. And it’s becoming an essential factor in this plot. If I understood correctly, even Google made a big deal with SpaceX, but the contract has an option to terminate very quickly as early as October. Well, well—doesn’t that smell a bit!? And the same capacity was sold to Anthropic with an even bigger deal. Hmm.. ![]() No signs of trouble starting to show? Google, Amazon, and others will still double their current investments in the coming years? I’ll believe it when I see it. But regardless, Nokia is indeed on the right side of the earnings, and eventually, that money will come in. But it’s worth keeping a critical mind when hearing all this “trillion” talk.

No signs of trouble starting to show? Google, Amazon, and others will still double their current investments in the coming years? I’ll believe it when I see it. But regardless, Nokia is indeed on the right side of the earnings, and eventually, that money will come in. But it’s worth keeping a critical mind when hearing all this “trillion” talk.

17 Likes

Probably not the same kind of bubble. But now, data center builders obviously have to build for the future. If capacity is, for example, undersized in 3 years, then the winners will be those with the most data centers. But if it is oversized, then nothing will be built again for a while. So, who can correctly estimate what the actual need is? And even if there is demand, some bottleneck could prevent them from being built at an accelerating rate. For example, ultimately energy—if data centers cannot get enough power, then there will be no need for memory either.

4 Likes

Google has been building data centers for twenty years now. They must have a very clear picture of the growth in the volume of data globally, so it’s unlikely they are increasing capacity at this rate based on faith alone.

1 Like

I don’t know, the scale is completely different now. I suppose everyone is relying on estimates at least to some extent.

2 Likes

@Lexus, you have brought up an excellent point! In today’s world, debt has become a tool that triggers the movement of capital, and it is indeed interesting how retail investors are increasingly being targeted as the ones to foot the bill. Creating a narrative and hype are part of the lure, promising grand futures—much like in pyramid schemes. With this, I am certainly not criticizing @Mustathmir’s posts, through which he has provided insight at many different stages. But has, for example, the specific perspective presented by Lexus remained in the dark?

I must admit I am still involved in Nokia with a position that is far too large for my liking, but I will continue to hold for now and see how this game develops.

5 Likes

Data Center construction has so far mostly been a matter of moving money from one company to another within a closed circle. This is reflected in the fact that the companies doing the building have become indebted. Nokia has also participated in this financing and has received business in return. This is the so-called Nvidia model.

It now appears that the money within the circle is running out, or financial ratios are starting to show weakness, or perhaps the markets have been so hot that it was thought bills could be passed on to retail investors without issues. It seems this might not go through quite so smoothly. Most amusingly, SpaceX probably revealed this. Money has to flow out from somewhere first for there to be enough for that IPO. Problems pile up when someone or some parties demand cash. That is the situation right now.

Indeed, as I said, Nokia’s position here is good, if not very good. However, as of late there have been increasing announcements—with companies even supporting or boosting one another—of assumptions regarding annually growing CAPEX levels… so it may be that this pattern won’t go quite so rosily in the coming years. Debt money was further pressured by rising inflation, and no wonder Trump doesn’t want any bombs in the sky or further escalation. As long as inflation runs (elevated oil prices), there is a mega-scale problem for data center construction. It partly drives capex down in the form of increased interest rates. Indirectly, that is. That’s how I see it. Oh, and potentially a worse problem for those in the circle would be a drop in share prices, as it could also hit earnings, and cash flows would become more prominent. This could be one motive behind executives’ calls to buy shares.

But still, a very positive view on Nokia in the long term. The short-term picture is overheated. And as previously hinted, I might be a stubborn mule. But perhaps I’m a bit bad at keeping quiet, and on top of it all, possibly wrong. ![]()

21 Likes

The risk of infrastructure overcapacity is entirely real, and history (railways, the 2000 dot-com bubble) has shown that too much capacity is always built during the early stages of a new technology.

When the market corrects itself and valuations stall in pure “compute hardware” (GPUs/servers), the winners will likely be those who offer efficiency, energy savings, and the sovereignty required by regulation. For this reason, Nokia’s optical portfolio may be exceptionally well-protected for an investor, even in the scenario that the hyperscalers’ major AI bubble bursts.

Jensen Huang today in South Korea compared the significance of AI to the intranet—perhaps prophetically? We may now be at the stage of the AI cycle where the internet was before the year 2000: hardware and fiber are being bought with eyes closed. But when the dust settles and capex discipline kicks in, the ultimate winners of the AI cycle will not be those who sell the most basic servers, chips, memory, and basic networks, but those ‘content creators’ and platform companies whose AI agents run the global economy.

As “training capacity” begins to exist in excess, the importance of intelligent edge networks and energy-efficient optics will be emphasized. Thanks to Infinera and its new technology platforms, Nokia is excellently prepared for this transition as well.

14 Likes

What would typically be Nokia’s theoretical acquisition price for a potential buyer at the moment? I assume a significant premium would need to be added to the current share price to secure a possible deal? The recent share price development has shown a fairly steep upward slope, and the ownership is, after all, quite fragmented.

Nokia among the financiers,

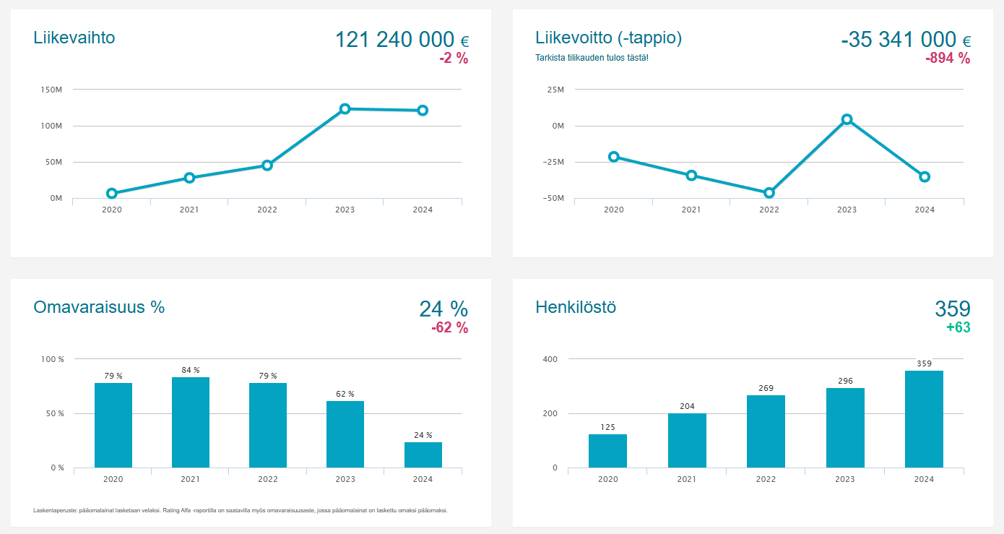

Huge funding for Iceye – Valuation rose to 10.5 billion | Kauppalehti

Nokia’s press release on the same (different topic)

Nokia today announced the launch of Nokia Deepfield Genome Shield, the industry’s first security automation system that facilitates proactive, always-on DDoS protection for telecommunications providers, hosting companies, internet exchange points, and cloud builders in the AI era. Genome Shield addresses the fundamental shift in DDoS threats driven by the emergence of residential proxy botnets, which now comprise approximately 200 million compromised devices worldwide.

9 Likes

I am not familiar with the company and I don’t know what happened in 2025, but there seems to be strong confidence considering this valuation as well.

I guess everything in space turns into gold.

It also crossed my mind that SpaceX apparently advertised “minesweeping” in their IPO prospectus—meaning they have the capability to neutralize space mines and offensive satellites. The value of this is obviously at its peak since it’s a relevant threat the day after tomorrow, if not tomorrow. ![]()

In all seriousness, it’s really great that high-tech new companies are emerging from Finland. The valuation does cause a bit of a cough, though—perhaps it’s just a sign of our times that all the old-timers (jäärät) don’t understand.

8 Likes

Nokia launches DDoS protection for the AI era

today at 10:11 AM ∙ Finwire

Nokia ADR

Telecommunications company Nokia is launching Deepfield Genome Shield, an automated security system for proactive DDoS protection aimed at telecommunications operators, hosting companies, internet exchanges, and cloud service providers. This was stated in a press release.

The solution is designed to counter the growing threat posed by AI-powered attacks and botnets based on hijacked consumer devices. The system utilizes continuous threat intelligence from multiple sources and automates security measures across the entire network.

The operator Reddot is one of the first customers to deploy Genome Shield.

Additional features are expected to be launched progressively throughout the year.

8 Likes

J.P. Morgan analyst Sandeep Deshpande maintained a Buy rating on Nokia today and set a price target of €12.00.

9 Likes

BofA raised its Nokia price target to 14.40 euros (from 10.70 euros) and reiterated its buy rating

The bank justifies its view primarily through the strong growth outlook for optical networks, data center switches, and AI infrastructure. Particular attention is given to 800G coherent pluggables, the new InP (Indium Phosphide) fab in San Jose, and upcoming 1.6T–3.2T optical modules.

BofA estimates Nokia’s adjusted operating profit to rise to 3.68 billion euros in 2028, exceeding Nokia’s current target range of 2.7–3.2 billion euros. In the report, the Optical & IP Networks business is valued at a 35x EV/EBIT multiple based on 2028 forecasts, reflecting a view of its position in the AI infrastructure market.

This is already the second significant price target hike within less than two months (€6.87 → €10.70 → €14.40).

A more extensive version with the source article can be found on Reddit.

28 Likes

This is amusingly illogical when the price target is set at 12.00, yet the recommendation is to buy at a price above 12.00 euros.

2 Likes

BofA’s new valuation is based on a sum-of-the-parts model . The bank applies a multiple of 35 times EV/EBIT to the Optical and IP Networks business based on 2028 estimates, and a multiple of 10 times EV/EBIT to the rest of Nokia.

Using this methodology, BofA estimates an enterprise value of €58.009 billion for Optical and IP Networks and €20.227 billion for the rest of Nokia. Adding net cash of €4.323 billion, it arrives at a capital value of €82.559 billion and a target price of €14.40 per share.

Optical and IP rocking at 35x, and the rest of the business, meh, at 10x. And calculations are based on 2028 forecasts—why even bother thinking about 2026 and 2027 anymore. They really found the “right” multiples there. ![]()

Looks like this update came out yesterday, so the biggest impact was likely seen then.

10 Likes

Nokia is now securing AI and cloud orders (€1 billion in Q1), which will be reflected as sales partly in 2027 and partly not until 2028. Therefore, 2026 is clearly a transition year compared to the following ones.

4 Likes

It’s definitely a gap year, and in a way, last year was too.

And it’s a peculiar situation when they dig into the valuation mothballs to use projections a couple of years ahead as justification. One might imagine that there is still some uncertainty regarding the year 2028. Apparently enough uncertainty that Nokia hasn’t updated its guidance (or targets), even though they likely know they are no longer valid.

10 Likes

A 10x EV/EBIT valuation seems quite cautious for a leading AI-RAN developer, especially when the market is expected to open up in '27-'28. One would also assume MXIE to be somewhat more valuable, not least on the Defense side.

Nokia once again showed strategic foresight by acquiring a stake in ICEYE; as Hotard stated: “Modern defense increasingly depends on combining trusted connectivity with real-time visibility. Nokia and ICEYE bring complementary strengths.” The Americans might not fully grasp this, as it caters more to the growing demand for European defense investments: data sovereignty and situational awareness combined with critical communications infrastructure.

11 Likes