I’ve been so foolish. I’ve been worrying that once the critical mass of data centers is built, sales will start to stall, since the equipment should last once installed. However, AI gives these kinds of figures:

Switches and routers: 5-10 year rip & replace, but this is mainly due to the need for upgrades rather than breakage.

Pluggables: 3-7 year lifespan, averaging 5.7 years.

I encountered a pleasant surprise with pluggables—they are practically consumables. InP (Indium Phosphide) can withstand higher temperatures, but conversely, it breaks down faster in high heat. That might be why they’ve been hyped, and a significantly lower TCO (Total Cost of Ownership) than competitors could matter even more. It’s actually a really good product if it generates recurring revenue due to replacements.

I was worried for a moment about the period following the data center build-out, but I don’t believe optics can be challenged anytime soon, especially in environments that run hot. Perhaps others have realized this already, which is why optics are being hyped, while I, like a fool, was just holding until now without proper justification. Just kidding. This just nudged my personal target price slightly upward.

Outside of data centers, optics do serve for the 10-30 years I had previously imagined. It’s possible that 3-7 years is optimistic after 1.6TB, but fortunately, Nokia is already reacting by packing ports into smaller spaces.

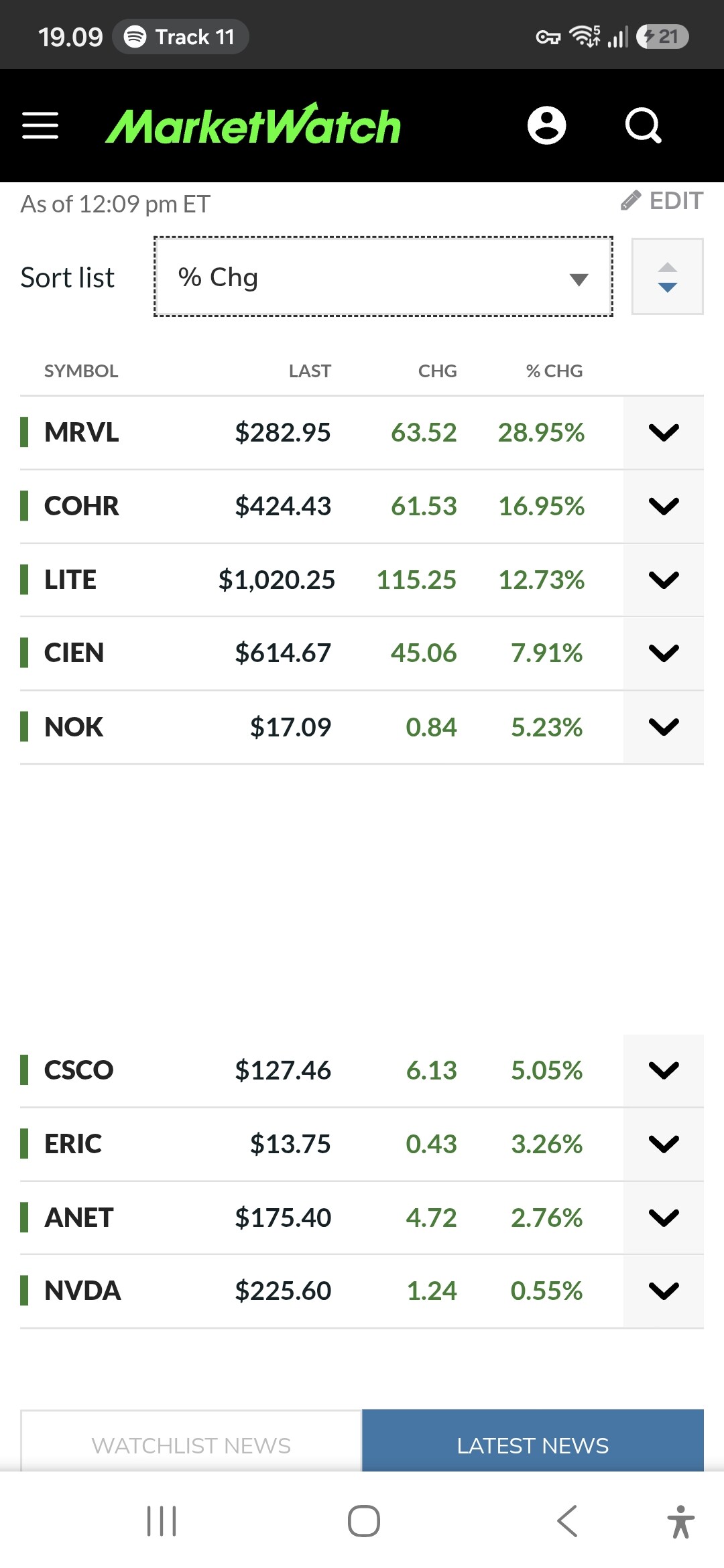

Should we be disappointed with the US session (so far)? Only in 5th place (among the peer group), though at least ahead of the sister (Nokia) and Erkki (Ericsson)

Surely for the sake of the weekend we should make it onto the podium

There are good reasons to believe that Justin Hotard is one of the best, perhaps THE best, CEO that Nokia has had in modern times. There are likely many of us who hope he remains in his position for a very long time.

At the same time, he has a history of moving on quite frequently. For instance, was he even at HPE for a full year? How do the forum’s experts view the risk of him seeking new opportunities again after a short time at Nokia? On the other hand, this is presumably his first CEO post, and there are clearly plenty of ingredients in place for great success, which in itself might motivate him to stay.

The situation at Nokia is certainly encouraging, both professionally and financially. It’s not worth leaving for just any minor role. And the guy seems to be enjoying his time at Nokia. There shouldn’t be any shortage of things to do, either.

A few years ago, Nokia experienced a so-called meme surge, which the company also commented on. Now, the rise has been many times greater, yet the company remains silent. Does this mean the share price looks right even in the eyes of management?

Perhaps, at least this time, Nokia has a leadership that also understands what is in the best interest of the company’s shareholders. They aren’t intentionally shooting down a rally, instead of at the very least keeping their mouths shut.

In principle, matters concerning owners or the share price are not the management’s concern. Of course, owners influence management through the board and general meetings to advance their own interests.

In principle, yes. The company’s management is obligated to act in the best interest of the company, and in practice, this means: increasing long-term value and developing the business in ways that directly benefit the shareholders.

The money-go-round… Nvidia, Coreweave —> Nokia. 5 GW! CoreWeave revenues we’ll be seeing already in Q2: Short-Term Goal: They are on track to double their footprint to 1.7 GW of active power by the end of 2026, funded by a projected $30 billion to $35 billion capital expenditure boom.

If HPE and Dell are raking in the $, no doubt it’s coming. Interesting video…

Background via Gemini:

CoreWeave’s 5 GW expansion plan directly translates into a massive, multi-year financial runway for Nokia. Because CoreWeave has selected Nokia as its global networking backbone partner, CoreWeave’s skyrocketing capital expenditure (CapEx) directly fuels downstream revenue for Nokia’s IP and Optical Networks divisions. With CoreWeave planning to scale from 850 MW to over 5,000 MW (5 GW) by 2030, their annual CapEx is booming—projected at $30 billion to $35 billion for 2026 alone.

Why This Spells Major Downstream Value for Nokia Full-Portfolio Adoption: CoreWeave is not just buying individual components; they are deploying almost Nokia’s entire high-performance network portfolio. This includes 7750 Service Routers (driven by their flagship FP5 routing silicon), 1830 Photonic Service Interconnect (PSI) systems, and the Network Services Platform (NSP) for automation.The Wide Area Network (WAN) Multiplier: Every time CoreWeave opens a new data center campus or adds gigawatts of power, those massive AI clusters must connect to each other across the U.S. and Europe. Nokia is the exclusive architect building out this ultra-low-latency WAN backbone.

The Energy Efficiency Win: A primary reason CoreWeave selected Nokia over competitors like Arista and Cisco was power efficiency. Nokia’s hardware allows CoreWeave to move 30% more data traffic within the exact same energy envelope—a critical advantage when scaling to a massive 5 GW footprint.Long-Term Revenue Visibility: Building 5 GW requires a multi-year construction roadmap. Because hardware, software, and optics must be deployed ahead of the GPUs going live, Nokia secures highly predictable, downstream enterprise revenue over the next four years.