BlackRock is pouring more money into the AI DC hype this week

Grok bets on Google, MSFT, or Amazon; could Microsoft be good for Nokia?

BlackRock is pouring more money into the AI DC hype this week

Grok bets on Google, MSFT, or Amazon; could Microsoft be good for Nokia?

That’s the Finnish market economy for you. First, there’s a massive outcry about how things shouldn’t be this way, and now that the situation/share price has corrected and even overshot a bit, it’s better to stay quiet so it doesn’t go into a freefall. Or how else are the rest of you supposedly investing?

Alright, now things might get active here again, since the share price is taking a hard dive without any negative news. Is this all there was to it…

You just described a stock I’m familiar with. It’s perfectly normal volatility, as long as it happens between €5 and €20 and there’s no reason for it. Welcome to the club of the puzzled.

No stock rises indefinitely… there are always corrections. Let’s see how low we go. The fundamental setup hasn’t changed, and there is still reason for optimism.

Across the pond, Coherent, Lumentum, Ciena, and Arista are seeing similar or even larger drops.

The correction was quite expected. Let’s take a little breather, and after a while, the climb will continue. It’s worth remembering that this is a long game, years long.

Everyone just take it easy now; this isn’t the end of the world or a final corrective move.

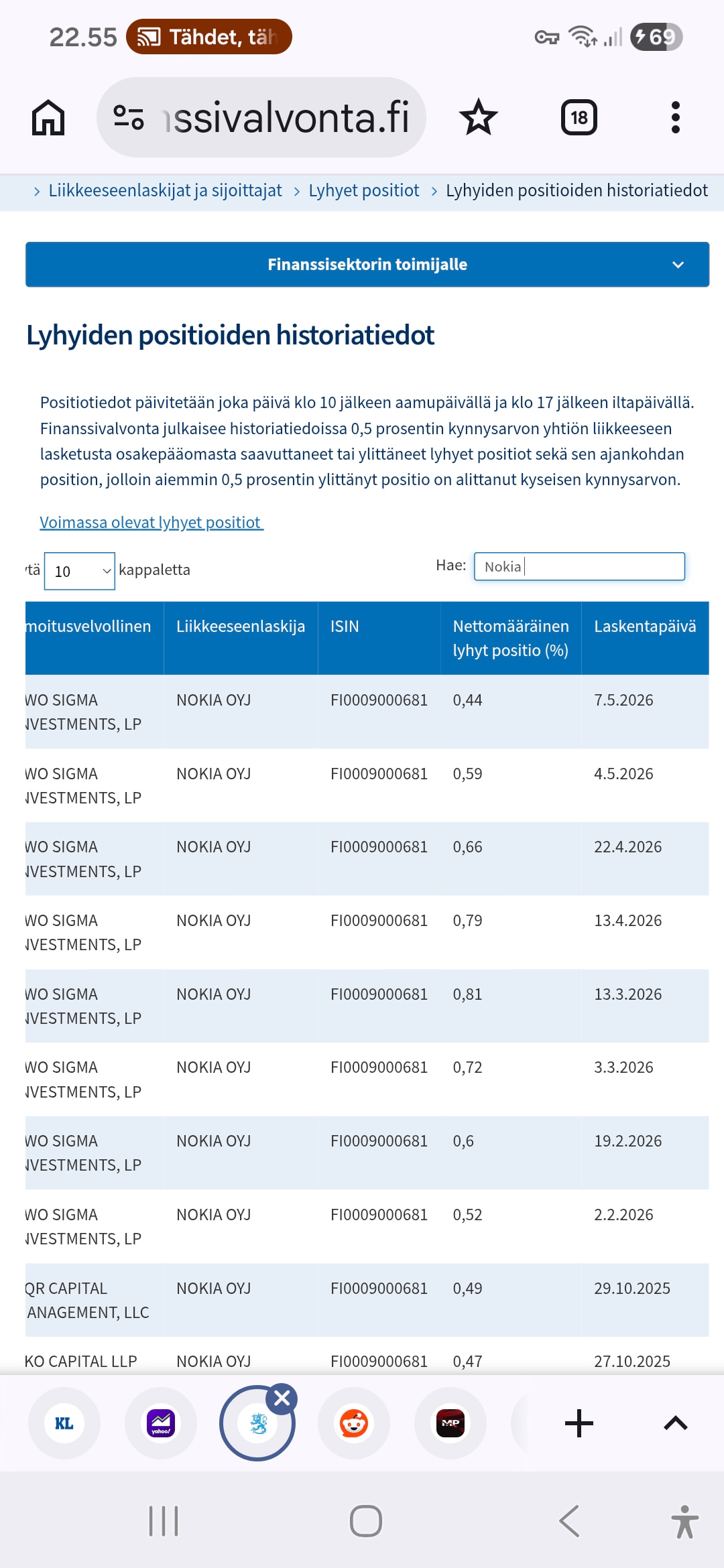

If one has to find something positive, Nokia is now in quite an impressive peer group, but so far partly with lower valuation multiples.

Exactly! People have been waiting for Nokia’s share price to rise to its so-called “correct” level. Now it has risen, surpassing all traditional figures and valuation multiples.

Personally, I bought the “falling knife” starting from over 5 euros down to about 1.5 euros. I’ve also added more at under four euros. During the Robinhood hype, even CEO Pekka said there was no basis for the stock price surge. There are no fundamental grounds now either, but Hotardi has no need to shoot the price down. And why would he, since he bought shares himself.

I hold 12.5k of Noksu (Nokia) and I’ve been thinking about trimming my position. I have a bit of a feeling that things are only just getting started. Same with Bittium. Everyone is “screaming” to trim, but I haven’t done it. There are a lot of Nokia shares in circulation, and a rise like this means they have been bought in massive quantities. There will be dips along the way, but it’s a matter of who has the stomach to stay on board. It’s nice to look ahead, and everyone has the permission to get rich. This is not investment advice, but read the analyses and follow the market! Personally, I’m playing my cards “to the end” or at least further ahead.

This could have been written by me. I have a way too large slice of my portfolio tied up in this. Nokia is now at the price levels where I might have sold before the last earnings report, which showed clear signs of growth; if I intend to follow my own investment rules even to some extent, the target has simply moved further out.

Nokia now seems to be riding the crest of several megatrends and is partnering with the top players in those fields, so if bubbles don’t burst, Nokia will certainly continue its rise later. It is quite expected that a massive rally won’t continue every single day; otherwise, getting rich would be easier than easy. Now we just need to be patient and let Nokia prove that the rise is fundamentally justified. I’m not selling, I’m not buying now, and I’m definitely not panicking.

Machine translation of my Reddit post

Nokia recorded €1 billion in AI & Cloud orders in the first quarter alone. For comparison, the total order intake for the full year 2025 was €2.4 billion, meaning the Q1 level is already 67% higher than last year’s quarterly average. While the uneven timing of orders (lumpiness) explains part of the strong start to the year, here are the grounds for why full-year 2026 orders could exceed €4 billion — and what that ultimately means for Nokia’s revenue structure.

Three drivers are converging right now:

Competitors are sold out: Lumentum’s CEO has announced that production is booked through 2028, and Ciena has a $7 billion order backlog. When established suppliers cannot deliver, customers certify new alternative suppliers.

San José Factory: Nokia’s San José factory (with up to 20 times the capacity compared to the current one) is a natural beneficiary of this development. Customers are reserving 2027 delivery capacity by placing orders as early as 2026.

Arrival of IP Networks: According to President Justin Hotard, IP network “design wins” will start converting into orders from the second quarter onwards. Thus, this was not yet reflected in the Q1 billion-euro figure. If the pull for optical networks continues and IP networks accelerate, the order flow for the remainder of the year will strengthen significantly.

The mathematics of revenue as orders turn into deliveries:

With delivery times of 12–18 months for optical networks, 2026 orders are primarily 2027+ revenue. It is essential to visualize what Nokia looks like when annual deliveries normalize to match a €4 billion order rate.

Assume that AI & Cloud revenue for 2025 was approximately €1 billion (this is a rough estimate, not a disclosed figure). When €3 billion in new AI & Cloud sales is added to Nokia’s approximately €20 billion total revenue, the result is a total of approximately €23 billion. In this case, the AI & Cloud share would be approximately 17% of the entire group’s revenue.

However, an even more striking figure can be found at the Network Infrastructure (NI) segment level. NI revenue was approximately €8 billion in 2025. If we assume for simplicity that the €4 billion AI & Cloud sales are entirely attributed to the NI segment, its share of the segment’s revenue is as much as 36% (4/(8+3) = 36%). At this stage, Nokia is no longer just a telecom equipment manufacturer with an optical division on the side. The AI and cloud business becomes the core of the NI segment.

This scenario would still represent only the early stage of Nokia’s transformation as a beneficiary of the AI supercycle. A potential €4 billion AI & Cloud order intake could itself be just an intermediate figure. Nokia’s new optical DSP portfolio will hit the market in the second half of 2027, the San José factory will reach full production capacity in 2027, and the growth in IP network orders is only just beginning in 2026. Each of these drivers is likely to accelerate further in 2027–2028. If the development of the order flow continues on its current trajectory, the €4 billion in 2026 may look like just the opening chapter in a much larger story.

It is always worth remembering the competition. There are strong players in the industry who are investing and developing constantly. Many are leading operators in their respective regions. Production “bottlenecks” will eventually disappear. Below is an AI response to the question regarding the competitive situation. Mustathmir’s calculation is correct in itself and aligns with Nokia’s financial targets, but it requires a perfect bull case. Yesterday’s sharp drop in Nokia’s and others’ share prices showed that the market does not fully believe in Nokia’s story, among others. The “front-leaning” valuation corrected slightly.

What happens when bottlenecks disappear?

The most likely development is normalization, not a collapse.

Typical cycle in the network equipment market:

Therefore, the most important question might not be:

“Can Nokia generate €4 billion in AI & Cloud orders?”

but rather:

“How much of this demand will remain as permanent market share once competition normalizes?”

And it will definitely exceed them; these numbers are going to smash all forecasts, just you wait, and the stock is going to soar way past all expectations.

Interesting post on Reddit, and below are thoughts processed through AI hidden in the details.

You are right — this wasn’t an AI datacenter story but something much more specific and, in fact, perhaps more interesting from an investor’s perspective:

and within it:

When you read it properly, the main point is NOT Anduril.

It’s this:

The Pentagon is moving from legacy tactical radios → to a private 5G / Open RAN architecture.

And if that holds true:

![]() it’s not about a single product deal, but potentially the start of a years-long procurement cycle.

it’s not about a single product deal, but potentially the start of a years-long procurement cycle.

tactical radios

proprietary waveforms

satcom-heavy

low bandwidth

Worked for:

voice

limited data

drone swarms

sensor fusion

edge AI

autonomous systems

real-time targeting

battlefield mesh networking

![]() the amount of data is exploding.

the amount of data is exploding.

And the core point of the article is very valid:

AI doesn’t fail because of the model — but because the data doesn’t move.

Because cellular technology:

scales

is software-defined

can be updated

offers much more bandwidth than old tactical radios

And Open RAN:

reduces vendor lock-in

fits the DoD’s supply chain/security mindset

enables more American control

This is the part that is genuinely interesting.

This is critical.

Not all telecom companies can just “sell to the Pentagon.”

You need:

clearance

a federal channel

trusted vendor status

local structure

Nokia has been building this for years.

And perhaps the most important sentence in the Reddit post is:

“Nokia is sitting in the cleared federal channel where the early dollars flow.”

This could be a very significant advantage compared to how the market still thinks of Nokia as a “European telecom operator supplier.”

The DoD seems to genuinely favor:

more open architecture

modularity

vendor diversification

And Nokia + Ericsson are practically:

That “3 hours anywhere on earth” isn’t just marketing.

It signals:

mobility

modularity

battlefield deployability

![]() i.e.:

i.e.:

private 5G is no longer just a “base network.”

It is:

At this point, it’s worth being realistic but open-minded.

If:

the DoD actually standardizes private 5G

tactical AI deployment grows from 2026–2030

Open RAN becomes institutionalized

![]() then Nokia could be:

then Nokia could be:

And the defense sector:

pays well

has long cycles

is not as price-sensitive as telecom operators

Old Nokia:

Possible new segment:

And these are markets with much higher strategic value.

And the Reddit post is honest about this, in my opinion.

The DoD:

moves slowly

pilots ≠ mass deployment

This is also true.

The market won’t easily grant “AI multiple expansion” to Nokia without:

actual contracts

visible revenue growth

And in fact:

Federal Solutions

named Anduril partner

current visible momentum

very strong US presence

Open RAN credibility

DoD may want a multi-vendor strategy

And the Pentagon LIKELY DOES NOT want:

![]() so:

so:

if this market emerges properly,

likely:

Nokia wins some

Ericsson wins some

The point in the Reddit thread about this is actually good:

Nokia trades at a discount to Ericsson despite possibly better DoD positioning.

If:

the defense/private 5G narrative starts showing up in results

Nokia starts talking about “awards” rather than “opportunities” in earnings calls

![]() a re-rating could be significant.

a re-rating could be significant.

This is NOT:

a “moonshot”

or “Nokia becomes Palantir”

But:

And most importantly:

![]() the market might not be pricing it in at all yet.

the market might not be pricing it in at all yet.

![]() Yes, potentially.

Yes, potentially.

Not yet in terms of revenue,

but:

Maybe:

25–40% chance it grows into a significant defense vertical

much higher chance it becomes a “good niche”

![]() Likely also a beneficiary,

Likely also a beneficiary,

but at the moment:

The “6 signals” in the Reddit post was a genuinely good list.

Specifically:

DoD budget line items

Nokia earnings-call language shift

pilot → award transition

repeat deployments

![]() those will determine if this is:

those will determine if this is:

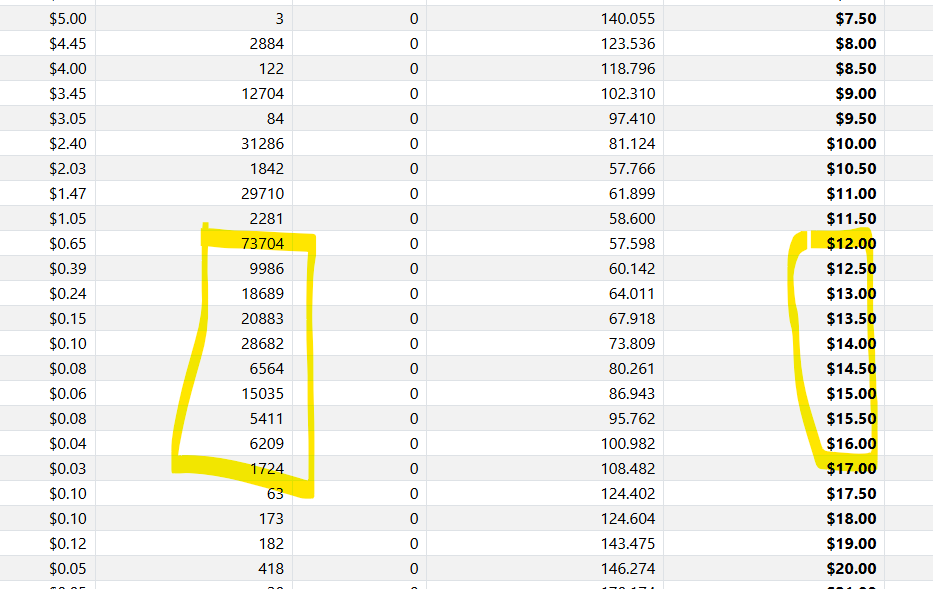

Edit: a pretty large pile of options are expiring worthless today if the price is $12.50 or below..

Same thing next week, and even lower puts if that serves as a spark

In reality, Nokia = Ciena + Motorola + Ericsson, but with a better technological outlook for the future.

In reality, Nokia is a company worth over 100bn with these new multiples. Institutional ownership is a total joke compared to Ciena, and 20% of the trades over the past year were made at prices above yesterday’s close, so that’s likely where we’re headed.

It wasn’t a very deep dip this time, at least for now. More volatility is surely to be expected in the future. Have a great weekend to all Nokia investors ![]()

It was definitely a clear mistake; they’ve made some hellish losses there.