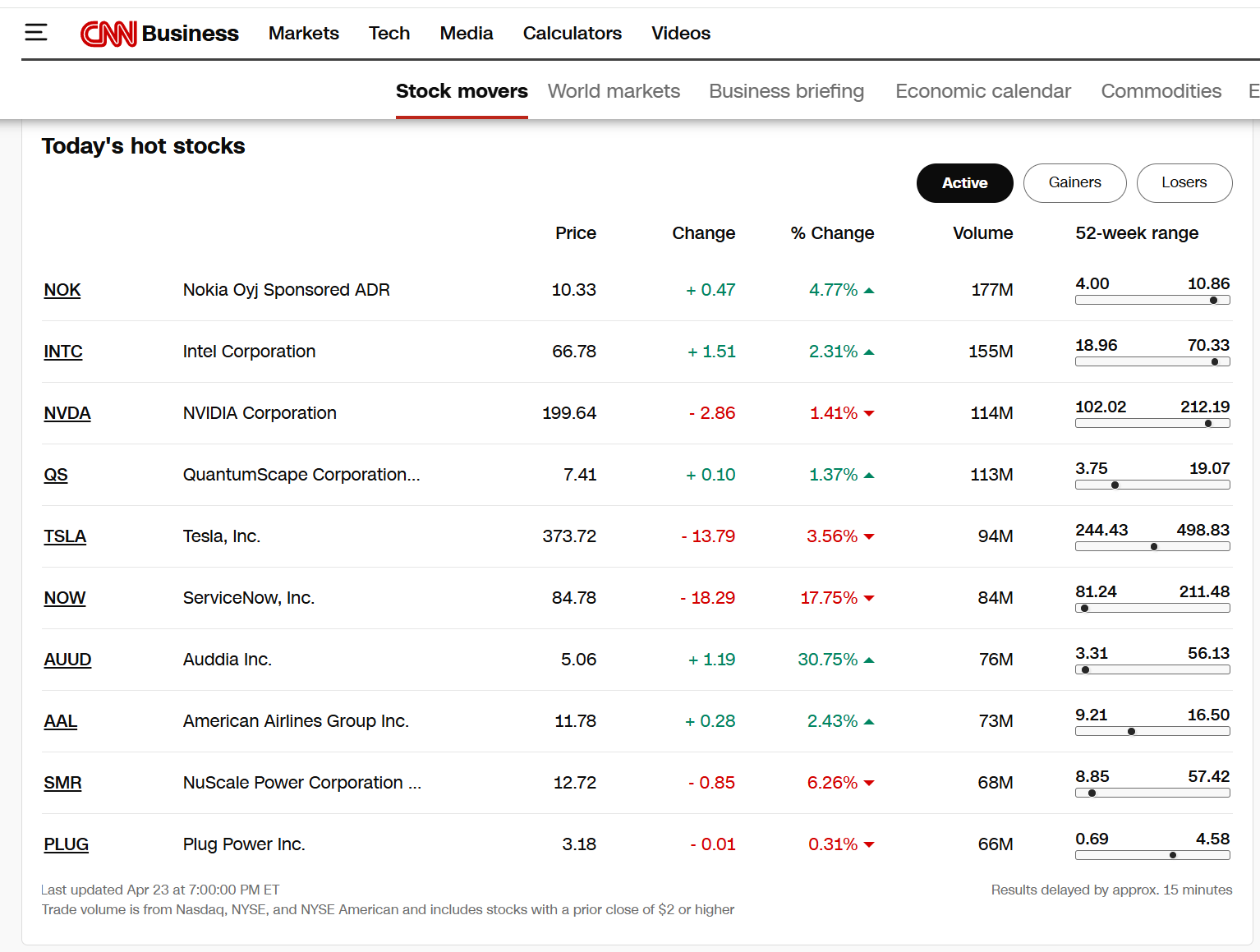

The stock price dropped like a stone at the NYSE open. I personally expected even the opposite reaction, but I wonder what the reason is. It was great to watch that 11% rise, and then bam, it dropped to around 2-3%.

4 Likes

Q1 results have been analyzed in the US, and Bank of America raised its target to $12.7 and reiterated its BUY recommendation. The previous target price was $12.4.

Investing.com - BofA Securities raised its price target on Nokia (NYSE:NOK) to $12.70 from $12.40 while maintaining a Buy rating on the shares. The stock has surged 90% over the past year and currently trades at $10.23, near its 52-week high of $10.69, according to InvestingPro data.

Nokia raised its Optical & IP Networks fiscal 2026 growth guidance to 18-20% from 10-12% organic growth. The company expects data center switch revenue to ramp significantly this year alongside continued strength in Optical Networks growth.

The data center design wins are predominantly with hyperscalers for U.S. data centers, indicating Nokia is penetrating the large but competitive market. BofA Securities had previously assumed penetration mainly in the smaller European Union sovereign data center buildout.

BofA Securities raised its fiscal 2027-2028 revenue estimates by 2-4% and increased operating expense estimates. The changes result in -0.6%/-0.2%/+3.2% adjustments to fiscal 2026/2027/2028 EBIT estimates.

The new price target is based on sum-of-the-parts valuation. BofA Securities noted that operating leverage may not be fully realized in the short term as new products ramp.

In other recent news, Nokia reported its first-quarter 2026 earnings, surpassing expectations with an earnings per share (EPS) of $0.0586, which exceeded the forecasted $0.0446 by 31.39%. However, the company experienced a slight shortfall in revenue, reporting $5.27 billion against the expected $5.32 billion. Despite this revenue miss, Nokia’s stock demonstrated strong investor confidence. Additionally, Nokia secured €1 billion in AI orders during the quarter, adding to the €2.4 billion of AI orders from 2025. Raymond James responded to these developments by raising its price target for Nokia stock to $12.00 from $7.00, maintaining an Outperform rating. These recent developments highlight Nokia’s growing influence in the AI sector and its solid financial performance.

26 Likes

CFRA nosti tavoitehintansa Nokialle 16 dollariin 6,50 dollarista

CFRA, an independent research provider, has provided MT Newswires with the following research alert. Analysts at CFRA have summarized their opinion as follows:

We upgrade our rating to Buy (Hold) and raise the target price to USD16.00 (USD6.50) by rolling forward valuation metrics to 2027 and shifting to P/Sales (P/S) from EV/EBITDA. We apply a 3.25x P/S multiple based on Optical Network peers’ five-year average on higher contribution from Optical Networks, stronger AI & Cloud demand visibility, and a more durable growth profile beyond the telecom cycle. The re-rating reflects improving earnings visibility and a structural shift in demand toward AI-driven infrastructure. While Q1 2026 results were in line with expectations, we raise 2026 revenue forecast to EUR21.5B (EUR21.1B) and 2027 to EUR23.3B (EUR22.6B) on higher Network Infrastructure growth guidance, improving supply visibility, and stronger order momentum. This also incorporates early backlog conversion and improving execution in Optical Networks. Hence, we increase 2026 EPS to EUR0.32 (EUR0.31) and 2027 to EUR0.39 (EUR0.37) on revenue mix improvement, with margin expansion expected as scale benefits materialize.

KOMMENTTI: Selkeästi korkein tavoitehinta tähän mennessä. Tavoitetta nostettiin peräti 146% kertalaakista.

37 Likes

Atte has published a new company report on Nokia in the wake of the Q1 results. ![]()

We reiterate our Sell recommendation for Nokia and raise the target price to EUR 6.0 (previously EUR 5.2). The highlight of the Q1 report was a clear upgrade in the growth outlook for optical and IP networks, reflecting a significantly strengthened market demand outlook in recent months as AI investments accelerate. Based on the report, we raised our earnings forecasts for the coming years by 6-7% and now forecast Nokia’s comparable operating profit (2028e EUR 3.15bn) to rise to the upper end of the company’s target range. Despite this, the stock’s valuation (2028e adj. P/E 21x and EV/EBIT 15x) looks stretched. At the current valuation, the investor thus has to bear risks regarding both the realization of earnings growth expectations and the sustainability of high valuation levels.

9 Likes

And here is an AI-generated summary of OP’s update.

Nokia – Demand is strong, but the price has gotten out of hand

Nokia’s market value has risen sharply in April (approx. EUR 11 billion), which has driven the stock’s valuation to a very demanding level. Although growth prospects have improved, the share price rise has outpaced the development of fundamentals.

Key observationsRecommendation and target price: Recommendation downgraded to SELL (prev. reduce). Target price raised to EUR 7.00 (prev. €6.30).

Valuation: Market value is approximately EUR 52 billion. Although the valuation multiple (19x EBIT) is reasonable compared to peers (such as Ciena), it is absolutely expensive relative to the return on capital (ROCE <10%).

Q1 result: Operating profit (€281 million) exceeded expectations by 12 percent. However, the quality of the result was mixed: the beat came from Mobile Infrastructure, while the strategically important Network Infrastructure fell short of expectations.

Outlook: Nokia significantly raised its growth estimates for Network Infrastructure for this year (new estimate 12–14%). Especially Optical and IP networks are driving demand.

Forecasts: The operating profit forecast for the current year is EUR 2.28 billion. The target for 2028 is set at EUR 2.9 billion, which corresponds to the midpoint of Nokia’s own target range.

Summary conclusion

Nokia is riding a strong wave of demand for optical networks, but the stock’s sharp price rise has already baked in a large part of future earnings growth. The valuation is currently too stretched relative to performance over the coming years.

15 Likes

Raymond James significantly raised their price target following yesterday’s earnings report;

Raymond James: 7usd (Outperform) → 12 usd & Outperform

Meaning at an exchange rate of 1:1.17, approx. 10.25 eur

The firm cited Nokia’s first-quarter 2026 results, which were largely in-line with expectations. Nokia added €1 billion of AI orders during the quarter, adding to €2.4 billion secured in 2025.

AI and Cloud represented 8% of quarterly sales compared to 4% in the first quarter of 2025. Optical and IP segments are leading the improvement.

Raymond James noted that inbound investor interest has trended higher since last fall’s capital markets day. The firm expects the next phase of growth to come from IP switching and routing.

The firm made modest changes to its estimates for Nokia.

15 Likes

As a side note: Finnish research firms are falling behind, and international houses are only making minor adjustments to forecasts but are stretching acceptable multiples quite significantly — like Raymond James above, for example.

18 Likes

It’s funny reading those sell recommendations with a €7 target price when the stock is at nine euros.

I was debating hard with myself about selling at €9 before the earnings report, but when it dropped to €8.50, I held on. It’s a bit of a gamble, after all.

In general, I’m wondering what drivers are moving the stock price. A couple of years ago, when we were grinding at the four-to-five euro level, several analysts were raising their targets to six euros and higher across the board, but the share price reacted in the opposite direction. Back then, it felt cursed. Now the spread in target prices is all over the map, but it feels like we’re riding some kind of wave. It seems that regardless of what the results, figures, and multiples show, as long as they’re hyping Nokia in the US, there could easily be a few euros of upside left. This is purely a sentiment-driven, white-knuckle rollercoaster ride right now.

8 Likes

Inderes raises Nokia’s target price to 6 euros, reiterates sell recommendation

today at 07.48 ∙ Finwire

Inderes reiterates its sell recommendation for the telecommunications company Nokia and raises the target price to 6 euros (5.20).

Following the first quarter, forecasts are raised by 6–7 percent, driven by strong demand for optical and IP networks, particularly from AI and cloud service customers. Growth prospects are raised, but the valuation is considered stretched due to high multiples.

Inderes points to risks regarding both earnings growth and the sustainability of sector valuations, despite the improved outlook.

4 Likes

The traditional Finnish mentality doesn’t easily bend to mindsets where targets are adjusted quite creatively.

Above, CFRA quite simply changed the valuation principle for the “hot” part from EV/EBITDA → P/S, following peer references, resulting in a new target of as much as 16 USD instead of the previous 6.5 USD.

In a way, it’s logical if that’s how the stock market values it today.

The challenge, of course, is for how long they will continue to value it that way…

14 Likes

It’s just as well that for example @Atte_Riikola from Inderes and @OP view Noksu as a non-growth company and keep the acceptable multiples low ![]() , they give others a chance. Goldman Sachs changed the multiples in its analysis at the last minute and shows that Wall Street

, they give others a chance. Goldman Sachs changed the multiples in its analysis at the last minute and shows that Wall Street ![]() understands the value of optical gadgets and knows how to pivot to a new narrative, even if it’s at the last minute.. Generally, domestic analysis firms find it difficult to adapt to the new (Nokia), but easy to stick to the old (surely QT will still rise

understands the value of optical gadgets and knows how to pivot to a new narrative, even if it’s at the last minute.. Generally, domestic analysis firms find it difficult to adapt to the new (Nokia), but easy to stick to the old (surely QT will still rise ![]() ). Without this forum, many would just follow the mindset produced by domestic analysts and what the headlines are written about. Besides, it seems that the technological knowledge and diligence of domestic analysts is on the level of an average retail investor like me, and in that case, it’s better to seek knowledge and background from the wise and from the swarm intelligence.

). Without this forum, many would just follow the mindset produced by domestic analysts and what the headlines are written about. Besides, it seems that the technological knowledge and diligence of domestic analysts is on the level of an average retail investor like me, and in that case, it’s better to seek knowledge and background from the wise and from the swarm intelligence.

17 Likes

Today, 08:13

Share

Nordea upgrades Nokia to Buy (Hold), target price EUR 10.5

Finwire News Agency

20 Likes

Technical analysis Nokia April 24 https://stockinvest.us/stock/NOK

2 Likes

As I said yesterday, everyone is raising their target prices except for those who don’t trust Nokia’s future plans and are too cautious and negative about the stock. Many are already looking ahead to 2027/28, while some are still stuck in the negative cycle that surrounded Nokia in recent years.

5 Likes

The optical side is on everyone’s lips right now, but I personally see the potential of AI-RAN as perhaps an even bigger growth driver. 10 operators have already signed up to test it… which I think shows that there is interest. If the technology breaks through, it could change the market dynamics of the entire industry.

5 Likes

Two Sigma has apparently reduced its short position to 0.66%. This was already done before yesterday.

In Kauppalehti today, 24 April 2026

-

10:47***

Nordea raises Nokia’s target price to 10.50 euros, upgrades recommendation to Buy (prev. Hold)

-

10:47***

Kepler Cheuvreux raises Nokia’s target price to 10.50 euros (prev. 8.20 euros), reiterates Buy recommendation

-

10:47***

Danske Bank raises Nokia’s target price to 9.50 euros (prev. 7.50 euros), upgrades recommendation to Hold (prev. Sell)

-

10:47***

Svenska Handelsbanken raises Nokia’s target price to 10.20 euros (prev. 7.80 euros), reiterates Buy recommendation

8 Likes