A good amount of froth has been cleared from the share prices. As I understand it, this is partly because data centers aren’t being pushed out as fast as expected, and partly because there isn’t yet enough demand for capacity to justify building them just to sit idle. Here are some reasons generated by AI:

| Company | What happened | Main reason |

|---|---|---|

| Microsoft | Paused/slowed some self-build campuses and lease commitments | Rebalancing capacity, construction sequencing, power availability, waiting for next-generation AI clusters (SemiAnalysis) |

| Amazon Web Services | Delayed some colocation leasing discussions | Better match supply with expected demand; trade/supply uncertainty rather than weak AI demand (LinkedIn) |

| Meta Platforms | No broad slowdown; instead exploring renting excess GPU capacity (“Meta Compute”) | Temporary surplus in some clusters while continuing record capex (Tom’s Hardware) |

| Some projects delayed by permitting and power constraints | Grid connections and construction bottlenecks, not announced demand cuts (The Wall Street Journal) | |

| Oracle | Continues aggressive expansion | Still capacity constrained due to AI cloud demand (Barron’s) |

| OpenAI / SoftBank (Stargate) | Timelines remain fluid | Massive power and construction complexity rather than cancellation (Latitude Media) |

Here are the worst bottlenecks, again generated by AI (it is a shareholder’s ethical duty to create demand):

| Rank | Bottleneck | Severity | Why it matters |

|---|---|---|---|

| 1 | Grid connection & substations | Utilities often need years to add transmission and substation capacity. | |

| 2 | Electrical equipment | Transformers, switchgear, breakers, and high-voltage gear still have long lead times. | |

| 3 | GPUs | Availability has improved, but cutting-edge AI accelerators remain constrained. | |

| 4 | Cooling systems | Dense AI clusters require advanced liquid cooling and specialized infrastructure. | |

| 5 | Skilled construction labor | Experienced electrical and mechanical crews are in short supply. | |

| 6 | Fiber/networking deployment | Large-scale optical networking still takes time but is generally less constrained than power. |

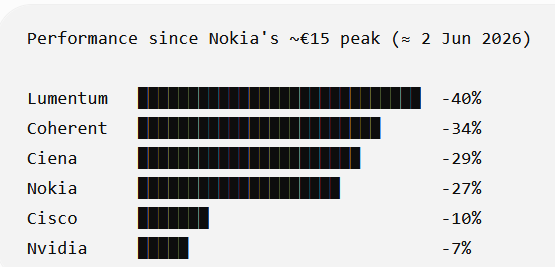

In my understanding, the bottlenecks on the electrical side give fully booked optical firms (Lumentum, Coherent, Ciena) extra time and the opportunity to play around with inventories—effectively overselling the future if it’s already known that projects will be delayed anyway. On the other hand, it also gives Nokia time to join the game, so the situation could turn into a win in the long run. Nokia’s new product family and additional capacity won’t be on the market until next year, and hyperscalers will surely take this into account when considering what products are available for future projects.

A slowdown is not an advantage for quick wins, but since we are coming from behind, it’s only good if we get more time to catch up. In 10 years, there will be an x-amount of data centers regardless, and if these delays lead to even a few wins, then in my opinion, it just means more profit over those 10 years + the references and potential new partnerships this could mean for the future.

If we drop below €10, I might consider adding to my position again for the first time in a while. Even at that price level, the near future is priced with significant multiples, but all things considered, it’s okay for me at this point. As a final lighthearted note, here is the “hindsight AI” tier list:

[details=“Hindsight AI list”]| Sector | Sub-segment | Top 3 competitors | Nokia position |

|----|----|----|----|

| DATA CENTER | AI Ethernet switching (800G/1.6T fabrics) | Nvidia, Arista, Cisco | #4–5 |

| DATA CENTER | Network OS (switch OS) | Arista, Cisco, Juniper | #3–4 |

| DATA CENTER | Fabric automation / AIOps | Cisco, Juniper, Arista | #4 |

| DATA CENTER | Data center routing | Cisco, Juniper, Arista | #2–3 |

| DATA CENTER | AI data center interconnect (DCI) | Nokia, Ciena, Cisco | #1–2 |

| DATA CENTER | Cloud-native network platforms | Red Hat, VMware (Broadcom), Wind River | #4–6 |

| DATA CENTER | Network APIs (hyperscaler cloud APIs) | AWS, Microsoft Azure, Google Cloud | Not Nokia domain |

| DATA CENTER | Digital twin / network simulation | Cisco, Juniper, Nokia | #3 |

| INFRASTRUCTURE | Optical transport (DWDM/OTN) | Nokia, Ciena, Cisco | #1–2 |

| INFRASTRUCTURE | Metro optical networks | Nokia, Ciena, Cisco | #1–2 |

| INFRASTRUCTURE | Long-haul optical | Nokia, Ciena, Cisco | #1–2 |

| INFRASTRUCTURE | Subsea cables | SubCom, NEC, Nokia | #3 |

| INFRASTRUCTURE | Carrier IP routing | Cisco, Nokia, Juniper | #2 |

| INFRASTRUCTURE | Fiber access (PON) | Nokia, Adtran, Calix | #1 |

| INFRASTRUCTURE | Microwave backhaul | Ericsson, Nokia, Ceragon | #2 |

| INFRASTRUCTURE | Enterprise campus networking | Cisco, HPE Aruba, Juniper | #5–6 |

| INFRASTRUCTURE | Routing silicon | Broadcom, Cisco, Nokia | #3 |

| INFRASTRUCTURE | Network automation software | Cisco, Juniper, Ericsson | #4 |

| MOBILE | 5G RAN | Ericsson, Nokia, Samsung | #2 |

| MOBILE | Massive MIMO | Ericsson, Samsung, Nokia | #3 |

| MOBILE | Open RAN | Samsung, Ericsson, Nokia | #3 |

| MOBILE | Small cells | Ericsson, Samsung, Airspan | #3–4 |

| MOBILE | 5G Core | Ericsson, Nokia, Mavenir | #2 |

| MOBILE | IMS / voice core | Ericsson, Nokia, Oracle | #2 |

| MOBILE | Private LTE/5G | Nokia, Ericsson, Celona | #1–2 |

| MOBILE | Mission-critical networks | Motorola Solutions, Ericsson, Nokia | #3 |

| MOBILE | Fixed Wireless Access | Ericsson, Samsung, Nokia | #2–3 |

| MOBILE | NTN / satellite integration | Ericsson, Qualcomm ecosystem, Nokia | #3 |

| MOBILE | Microwave transport | Ericsson, Nokia, Ceragon | #2 |

| MOBILE | Space / lunar LTE | Nokia, NASA partners, ESA ecosystem | #1 |

| DEFENSE | Private 5G (military bases) | L3Harris, Thales, Ericsson | #3–4 |

| DEFENSE | Public safety LTE/5G | Motorola Solutions, Ericsson, Nokia | #3 |

| DEFENSE | Secure government networks | Cisco, Thales, Ericsson | #3–4 |

| DEFENSE | Critical infrastructure comms | Cisco, Siemens, Nokia | #3 |

| DEFENSE | Secure optical transport | Nokia, Ciena, Cisco | #1 |

| DEFENSE | Quantum-safe networking | Nokia, Cisco, Juniper | #1 |

| DEFENSE | Drone / field connectivity | Ericsson, Qualcomm ecosystem, Nokia | #3 |

| DEFENSE | Space / defense comms integration | Lockheed Martin, Northrop Grumman, Nokia | niche |

| FUTURE | Network APIs (telco exposure / CAMARA) | Ericsson, Nokia, Google | #2 |

| FUTURE | Telecom exposure platforms | Ericsson, Nokia, Amdocs | #2 |

| FUTURE | SaaS network management | Cisco, Juniper, Ericsson | #4–5 |

| FUTURE | AIOps / automation | Cisco, Juniper, Arista | #4 |

| FUTURE | Edge computing platforms | AWS, Microsoft, Ericsson | #3 |

| FUTURE | Cloud-native telecom stack | Ericsson, Nokia, Mavenir | #2 |

| FUTURE | Quantum-safe cryptography | Nokia, Cisco, IBM | #1 |

| FUTURE | Digital twin networks | Cisco, Juniper, Nokia | #3 |

| FUTURE | Network OS evolution (SR Linux) | Arista EOS, Cisco NX-OS, Junos | #3–4 |

[/details]

2.5 billion extra in R&D, partnerships, improved focus, and restructuring can significantly improve positions as early as 2030. Infinera only joined Nokia last year, and quite a lot has already happened. Have a good weekend.