I think the same, but it requires flawless execution. Below is a draft of a post that I had translated from English.

Ciena vs. Nokia – Repricing of AI Infrastructure

Ciena (CIEN) has risen from around $90 (August 2025) to over $335 (Feb 20, 2026) – representing approximately +270% in six months. The market has effectively repriced Ciena as a pure-play winner in AI optical infrastructure.

It tells us one thing: the AI super-cycle isn’t just about GPUs – it’s about optical transport capacity and energy-efficient data movement.

What sets Nokia apart?

Ciena is a specialized optical company. Nokia’s Network Infrastructure (NI), on the other hand, is optics + IP routing + fixed networks.

In 2026, the competition will shift from the question of “who was first in 1.6T” to “who can deliver the most efficient comprehensive solution at scale”.

1) Speed Parity

Nokia lagged behind Ciena in 800G shipments. Now, Nokia’s PSE-6s engine brings the company into the same 1.6T class. 800G transport over 2,000 km has been demonstrated – meaning it’s no longer just a laboratory feat, but actual long-haul traffic between AI data centers.

2) Integrated Stack

Nokia also designs its own routing chips (FP5/FP6). When optics and routing are designed together (“coherent routing”), the goal is significantly better power-per-bit than with standalone solutions. Energy is currently the true bottleneck for AI data centers.

3) Industrial Leverage – San Jose Fab

Nokia is the only Western optical player with its own InP (Indium Phosphide) chip fab in the United States.

A California state document describes a project where PIC (Photonic Integrated Circuit) capacity is being increased tenfold. This has an impact on supply security and Nokia’s cost structure.

The transition from 3-inch wafers to 6-inch is designed to improve production volumes per run and aims for a significant cost-per-bit improvement, provided yields are successful. In other words, once production is ramped up, the cost structure of optical networks will lighten significantly, which will have a margin-boosting effect.

Valuation Perspective

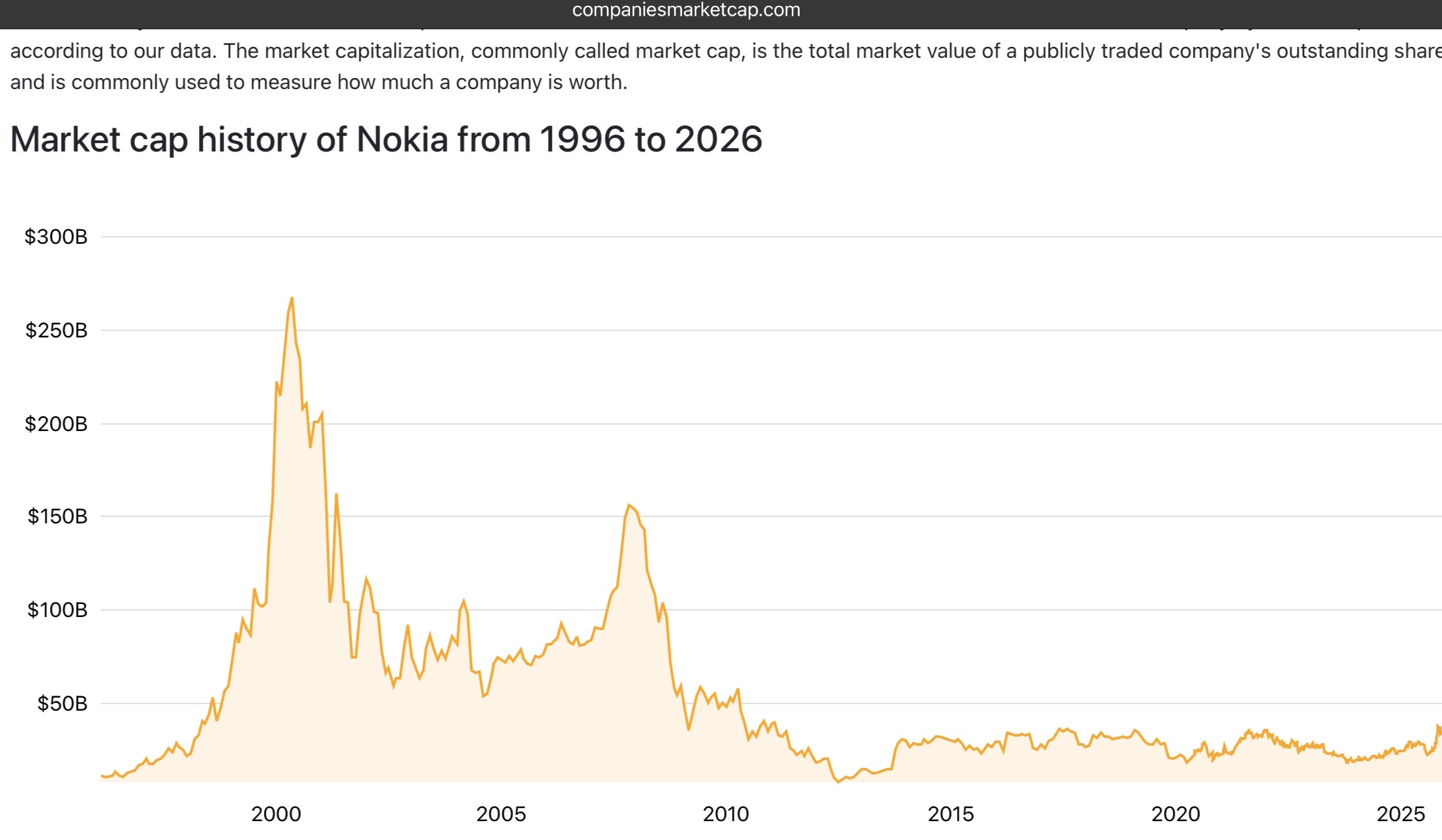

Ciena’s market capitalization (~$45–47 billion) has risen to a level that approaches or exceeds the entire Nokia Group (~$42 billion). This means the market is effectively valuing a specialized optical player higher than Nokia’s entire NI + patent portfolio + mobile networks combined.

If the AI build-out is a multi-year cycle and if NI can demonstrate:

- recurring hyperscaler demand

- margin expansion towards the 13–17% target range

- the appeal of IP routing alongside optics

the market could very well conclude that the current valuation gap is not structurally sustainable. We may have already begun to “hear” the prelude to a valuation correction recently.

So, it’s not a question of whether Nokia is “fully priced” right now – but whether the repricing of AI transport infrastructure is only just beginning for Nokia as well.