Proprius Partners’ review from yesterday. You can get them by simply joining the mailing list https://proprius.fi/ Copying is prohibited, so I am only summarizing.

The title of the letter is “buy the dip earnings season.” Nokia is discussed: “A new page turns… the dip on earnings day was recovered within a few days and it has risen higher… guidance… nicer to surprise positively… AI… valuation is only slightly elevated… by gradually reaching growth targets, one can expect an improving result, a classic buy the dip…”.

So they have been reading the thread. Validation.

The last time in the thread was “Mr. Market’s turn to speak” written by Viitikko from Proprius 2 years ago (let bygones be bygones…)

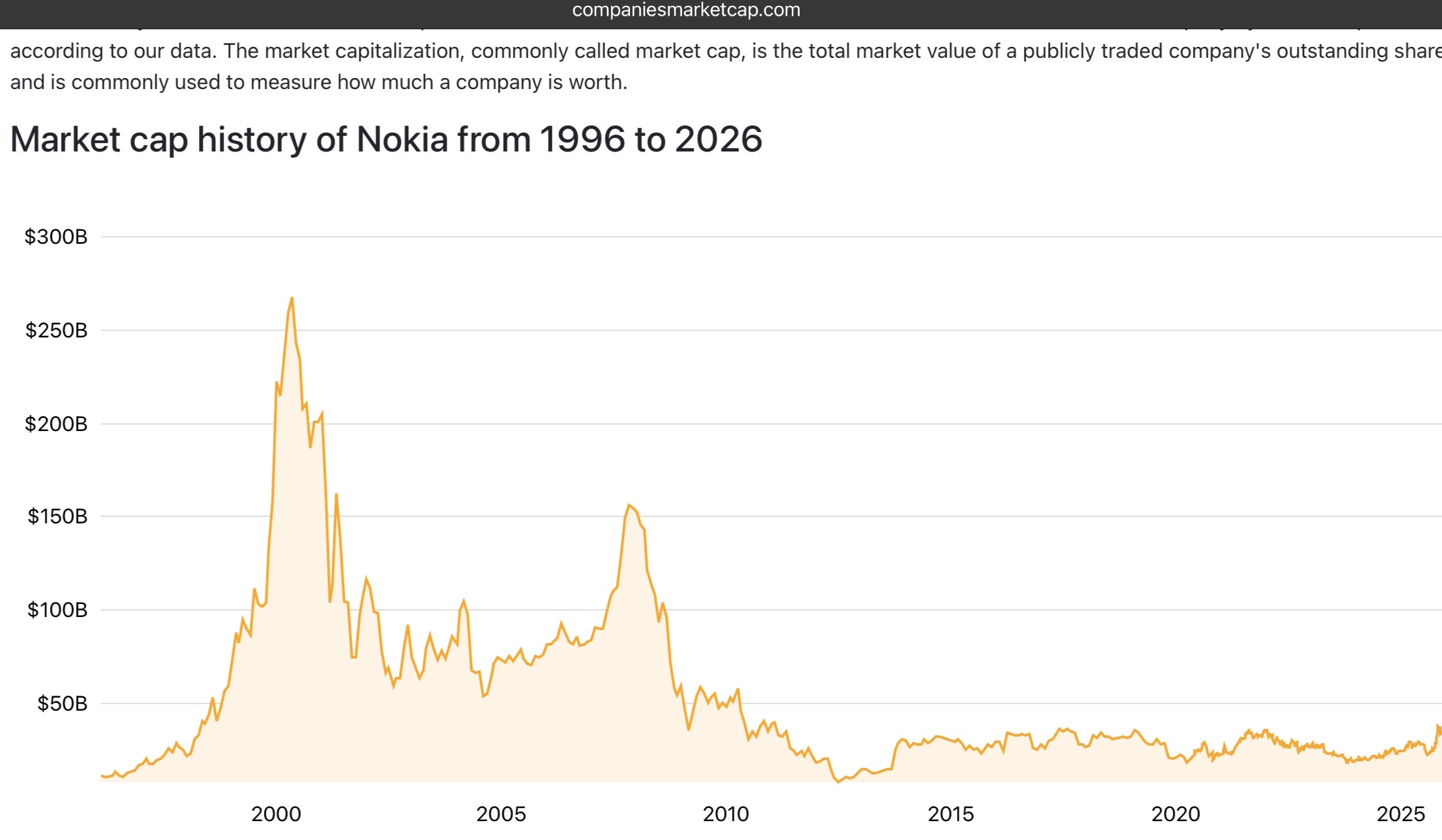

Nokia (19 billion euros)

“The Finnish record (SE) for kicking the can down the road is approaching, but there is a risk of stepping on the can. Finnish tech companies… perhaps not the most vibrant place to be. Valuation is cheap – yeah, I was listening to the same chatter even when Apple started to truly displace Noksu. I remind you that in tech firms, looking at valuations leads to stepping into such value traps that 5G cycles won’t help much. And anyway, these new Gs are of no use to these hardware firms – all the money is sunk into R&D (T&K) and you never get it back.”

The new article doesn’t actually say that it is in a dip anymore. We are currently at the same price levels as in 2014-2016. The phones had been sold, the Alcatel-L deal was made, and the number of shares likely increased significantly, so the market cap (m-cap) is probably higher now. The impact of inflation in the comparison is offset by dividends, which also had to be canceled in some years, and that is when buying opportunities arose because things were so miserable.

But it is perhaps misleading to compare the numbers, because we are a different company than 10 years ago and than 25 years ago.

Signed, on board for longer than 10 years.