Good question. In the automotive sector, as I understand it, the trend is trading down to cheaper models or giving up the vehicle altogether. In boats, on the other hand, it seems that the more expensive ones are still performing well, while demand for cheaper boats (under €100k) has indeed softened. I wouldn’t be surprised if the strong performance in the US was the primary reason that growth remained positive. The current quarter is indeed the most important of the year, and I don’t see any major threats in that regard.

However, I am by no means an expert in the boating industry, so please, others who know more about these things, feel free to comment

I agree with @AnttiM. From a Nordic perspective, the boat market is very volatile, especially in the cheaper category. Nimbus’s strategy is global expansion, particularly in the USA (e.g., the EdgeWater deal). Therefore, I believe that expansion abroad, where target customers generally belong to the Premium category, should reduce the correlation of sales with the general market situation. Actions that I believe provide a credible picture of the strategy include, for example, expansion into a new segment through the new flagship model, the Nimbus 465 Coupé.

On the plus side, I also see a strong order book in the USA, the easing of supply chain challenges, and an expanded global distribution network, meaning sales and profit should be delivered in this upcoming, more important quarter; otherwise, I personally view the current use of cash flows and the dividend cancellation as very questionable.

Following these dealership/representation/whatever opening news, you start to wonder if they’re even worth a stock exchange release anymore. It feels like one new opening a week is already business-as-usual for Nimbus

"Today, Nimbus Group AB (publ) (“Nimbus Group” or the “Company”) has taken possession of the shares in the acquired US company EdgeWater PowerBoats, LLC (“EdgeWater”) in accordance with the terms and conditions communicated by the Company in a press release on March 8 of this year.

As previously communicated, the cash purchase consideration totaled MUSD 9.5 on a cash and debt-free basis (corresponding to approximately MSEK 103). Synergy effects are expected to arise through a stronger market position and access to production capacity in the US as well as more efficient logistics, which is also positive from a sustainability perspective. The acquisition also includes an industrial property.

EdgeWater will form part of Nimbus Group’s US organization and be consolidated into Nimbus Group’s accounts as of the date of transfer of the shares.

The North American motorboat market is the single largest in the world and in terms of volume, it accounts for half of all motorboats sold annually. In recent years, Nimbus Group has made major investments in North America to take advantage of the opportunities offered by the market there.

"The acquisition of EdgeWater is a crucial part of the implementation of Nimbus Group’s defined growth strategy, in which an expansion in the key North American market plays a central role. Owing to our highly goal-oriented strategy in North America, we have successfully increased our sales there in a robust manner over the last year. For the first quarter of the year, we could report that the order book for North America increased 60 percent year-on-year, reaching a new record-high level,” says Jan-Erik Lindström, CEO of Nimbus Group.

EdgeWater was established in 1992 to design and manufacture robust, safe and reliable boats under the EdgeWater premium brand. EdgeWater sells boats to the North American market, and in 2022 sold over 300 boats in sizes up to 37 feet. The boats are primarily salt-water vessels of the center console type used for leisure, fishing and transport. All boats are equipped with outboard motors. With around 165 employees and an experienced management team, EdgeWater had approximately MUSD 47.7 in sales in 2022, an adjusted EBIT of approximately MUSD 3.0, and an adjusted EBIT margin of approximately 6.3%."

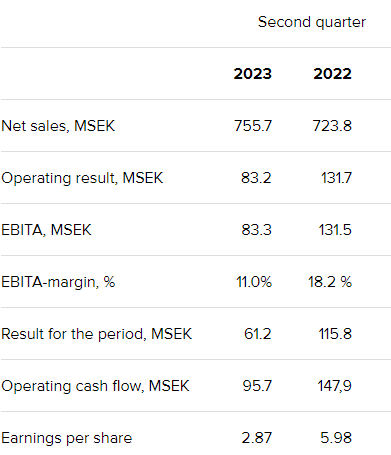

My own expectations were somewhat apprehensive, wondering how much sales had slumped. The result wasn’t quite as bad as I feared, but on the other hand, it was no triumph either compared to a year ago. Sales grew 4% (Organic growth -5.4%), but profit plummeted. Still in the black, however, and EPS was 2.9 SEK. https://www.inderes.fi/fi/tiedotteet/nimbus-group-second-quarter-report-2023

Decent-looking numbers despite the decline in profit. The stock’s valuation is only around P/E 4 based on last year’s figures, so even if the profit were to halve, it still wouldn’t make the stock shockingly expensive. Of course, that won’t stop foolish investors from halving the share price again . I wonder what impact the krona and the Swedes’ knack for bungling it into worthlessness will have on this company as well .

Order book:

The order book totaled MSEK 1,103, up 5 percent year-on-year (1,051).

Regarding North America, which is currently the strongest market:

At the end of the quarter, the North

American order book amounted to MSEK 614 (whereof

EdgeWater MSEK 154) corresponding to more than half of

our total order book. Our major investments in the North

American market in recent years are increasingly appearing

to be a very wise decision and it is obviously gratifying to see

how our strategic initiatives for growing the company are

having the desired effect.

The order book in North America increased by 305 percent

to MSEK 614, corresponding to 56 percent of the total order

book. EdgeWater orders amounting to MSEK 154 are

included in that figure

The market seems to have received the results quite neutrally. (There was a shockingly large spread a moment ago, is it always like this here?)

Optimistically, one could see that the decline in earnings is leveling off. TTM EPS was -44% and it has certainly decreased further from there, but since both Q2 and H1 are both -52%, at least the decline hasn’t accelerated anymore.

But boats aren’t exactly necessity goods, so a possible recession could then do some nasty damage.

You often see a spread of two to three crowns with this one.

The result fell slightly short of my expectations, which is explained by weaker-than-expected demand for smaller boats. Larger boats and especially US sales were positive drivers, as was, of course, the good development of the order book (in recent years, total orders have decreased from Q1 to Q2, but now there is a small increase thanks to the Edgewater acquisition).

I would say that the biggest impacts are already visible in this report, and small boats took a hit in particular. But much depends on general economic development, interest rates (especially SEK and USD), and the exchange rate of the krona.

A couple of relevant quotes from the CEO:

So thanks to long lead times, capacity can be shifted somewhat from small to large boats. Currently, we may well be at the bottom of the cycle for small boats, and for large boats, no major weakening is visible (at least yet). All in all, I would say this withstands a (mild) recession quite well. But let’s see what is said in the webcast.

That is one thing that still worries me here. The sales boost from the pandemic will likely show up in the used market as some of the new boaters inevitably get tired of spring maintenance and such. Recent used boats will then compete with new production.

Disclaimer: I don’t own the stock yet, I’m just considering it and looking for the right timing.

This will surely happen to some extent. One should probably monitor the price levels of used boats and see if there are downward corrections. Historically, boats have held their value somewhat better than cars.

From the webcast:

Poland (small boat) factory closed as part of capacity shifts towards larger boats.

Global market drivers: general wealth on the rise (though inflation brings a setback) + staycation phenomenon favoring local travel and easy & fast vacationing + aging boat fleet (especially in the US, where 46% was built before 2000) + technical development enabling easier boating and maintenance for new boats.

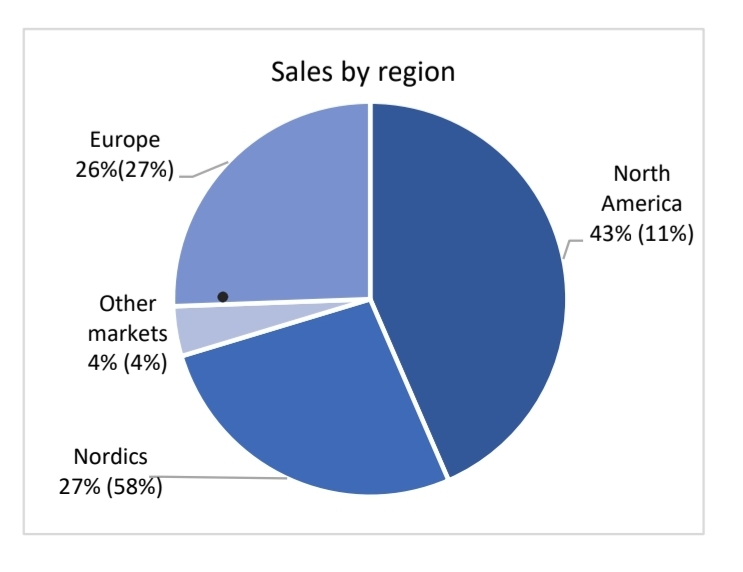

Order book increase mainly due to N. America (+305% y/y). A slight decrease in Northern Europe, but currently a good and steady situation across markets (with a relatively small number of dealers). Stability helps smooth out future (market-specific) fluctuations to some extent.

In sales, N. America has more than tripled. Edgewater’s share of this is about 1x, meaning it would have doubled even without it. Largest motorboat market, 47% of all new boats sold in N. America.

The decline in EBITA is largely explained by increased costs and the weakening of the SEK. Costs can be passed on to prices, but due to long lead times, there is a small (1-2 Q?) delay here.

Financial targets (growth 10%+, EBITA min. 10%, no debt, 30% out as dividends) are still maintained. Note! These are (mid)long-term targets, so missing them likely won’t trigger a profit warning unless the gap is massive.

Still room for growth in the entire market, and we are currently far from the peaks of the 90s(?).

Next interim report coming Oct 25, 2023.

Q&A:

– Edgewater’s profit margin is practically 0.3% (analyst’s estimate). Growth potential is seen here in the future (price hikes, synergies).

– Sale & lease-back of recently acquired Edgewater buildings being considered to increase liquidity.

– The small boat market is roughly 50% of Nimbus’s business. Not completely dead; “a few” are sold every week.

Overall, my own feeling is cautiously positive. Progress in the US compensates well for the sluggish demand (and weak currency) in Northern Europe, and management has been well on top of capacity adjustments. The initial market reaction seemed negative, but I expect it to level out and even turn into a slight rise once the most hasty sellers have finished their trades.

Would any of the followers of this thread have access to Nordea’s or Carnegie’s analyses on Nimbus? For example, a summary and forecasts for the coming years (as well as the target price) would be a valuable addition to the thread.

Apparently, these two (along with the smaller Analysguiden, latest analysis behind the link) are the only ones covering BOAT.

It appears to be a Hold recommendation, and the fair value is given as 57 SEK. Overall, some decline is anticipated for this year compared to the previous year.

Here is a good article about the Finnish boat market:

So it’s been a sharp decline, but one could imagine that the bottom is at hand. On the other hand, Nimbus’s brands have fared reasonably well (read: declined less than the motorboat market as a whole).

I double-checked the above through first registrations (link below), and indeed, Nimbus’s brands seem to be gaining market share in this difficult market Bodes well for the next bull market

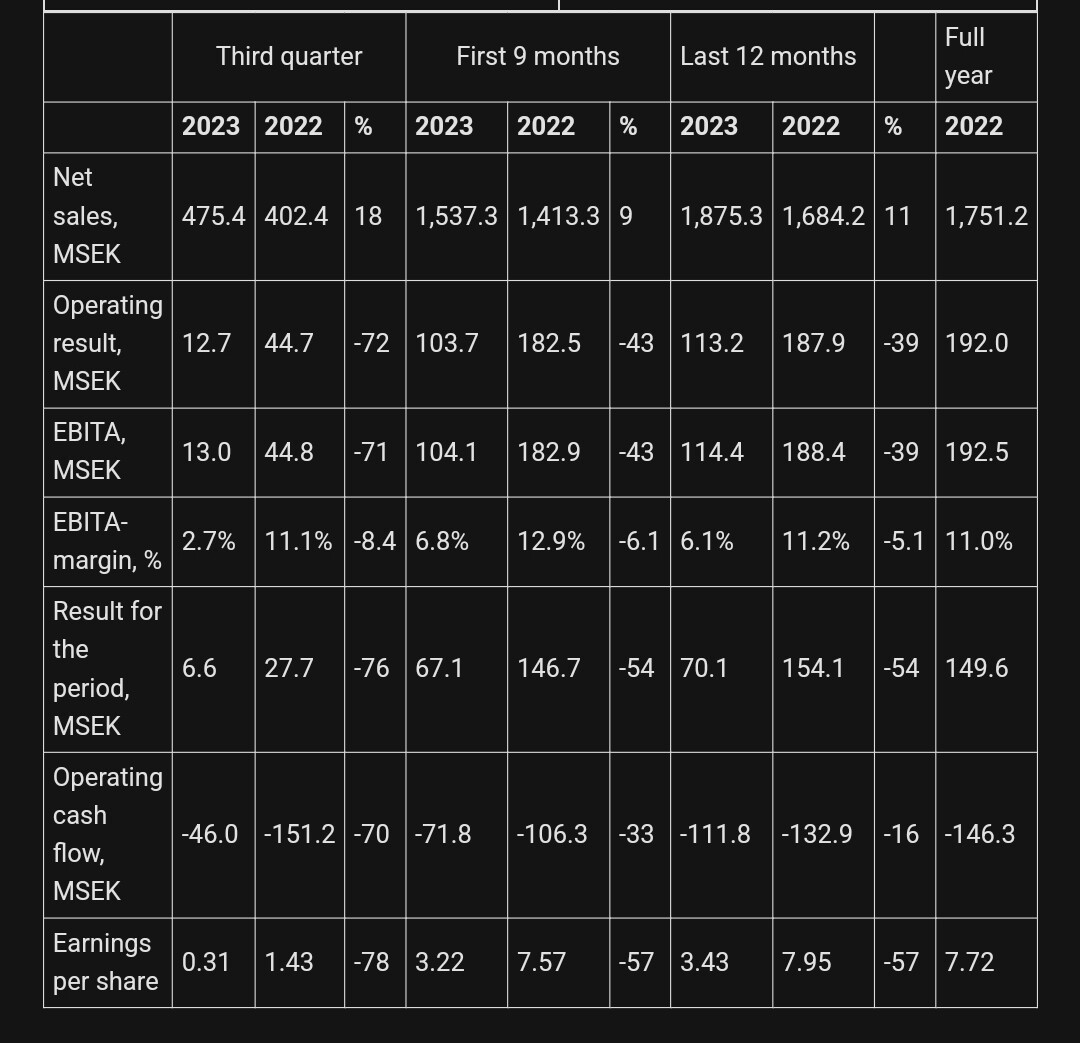

Sales were a positive surprise, profitability a negative one. Apparently, the limits of the company’s pricing power have been reached, and the final quarter of the year is currently expected to be loss-making.

An interesting shift has occurred in the sales distribution (Q3/22 vs Q3/23): US sales have more than tripled, while the Nordics have dropped by half. There must be some involvement of oligarchs’ boat purchases here, which have now ceased completely during 2022-2023 (orders usually take 6-12 months, so changes appear with a delay). Fortunately, replacement demand has been found in the US, otherwise the numbers would be quite grim.

Edit: @Pancake I should clarify that I wasn’t so much wondering about the rise in US sales (which is largely explained by the Edgewater acquisition), but more about the sharp drop in the Nordics, especially when compared to the rest of Europe.

The top line grew, while the bottom line shrank. I wonder how the weakened Swedish krona causes challenges for a company that reports in krona? I would think it would be better for them.

I need to study the presentation and listen to the recording in the evening. The conference call starts at 11:00.

A US acquisition has a strong impact here. The acquired revenue was less profitable, but certainly strategically sound. Naturally, regional sales also shift as a result, and profitability deteriorates, at least temporarily.