Mielestäni tämäkin saksalaislähtöinen firma ansaitsee oman ketjunsa. Itsellä ensimmäiset muistikuvat tästä juontaa juurensa vuoteen 2015 kun kotimainen Solibri myytiin Saksaan Nemetchekille.

Yrityksen historia menee kuitenkin hieman pidemmälle. Professori Georg Nemetchek perusti yrityksen nimeltä Ingenieurbüro für das Bauwesen (engineering firm for the construction industry). Yritys keskittyi rakennesuunnitteluun ja oli ensimmäisiä yrityksiä, jotka hyödynsi tietokoneita sekä ohjelmistoja suunittelussa. 1980-luvulla yritys julkaisi 1. ohjelmiston, joka mahdollisti tietokoneavusteisen suunnittelun tietokoneissa.

1989 nimi muuttui Nemetschek Programmsystem GmbH ja 1980-luvulla lähti kansainvälistyminen käyntiin. 1996 Nemetchekillä oli tytäryhtiöitä kahdeksassa Euroopan maassa. Ensimmäiset yritysostot tehtiin 1990-luvun lopulla ja pörssilistautuminen tapahtui 1999. 2000-luvulla on tehty lukuisia yritysostoja: Diehl Graphsoft (nykyisin Vectorworks, Maxon Computer, Graphisoft, SCIA Internatinal, Data Design Systems, Bluebeam Software, Solibri, SDS/2, dRofus,RISA,MCS Solutions ja lukuisia muita. Pelkästään tämän listan luettua tulee melkoinen ähky.

Lyhyen alustuksen jälkeen on hyvä kahlata yrityksen oma presentaatio läpi.

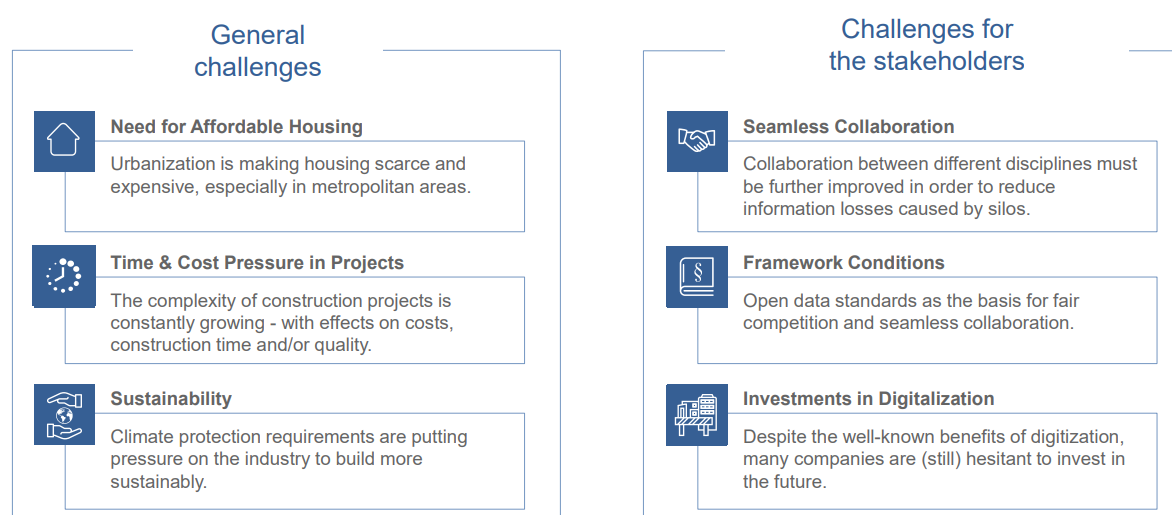

Rakennusalan ongelmat ovat erittäin tunnetut ja nämä tuskin tulevat yllätyksenä. Digitalisaatio on viime vuosikymmeninä ottanut harppauksia eteenpäin, mutta matkaa on vielä kuljettavana runsaasti. Lisäksi uutena haasteena on rakentamisen hiilijalanjälki ja sen pienentäminen.

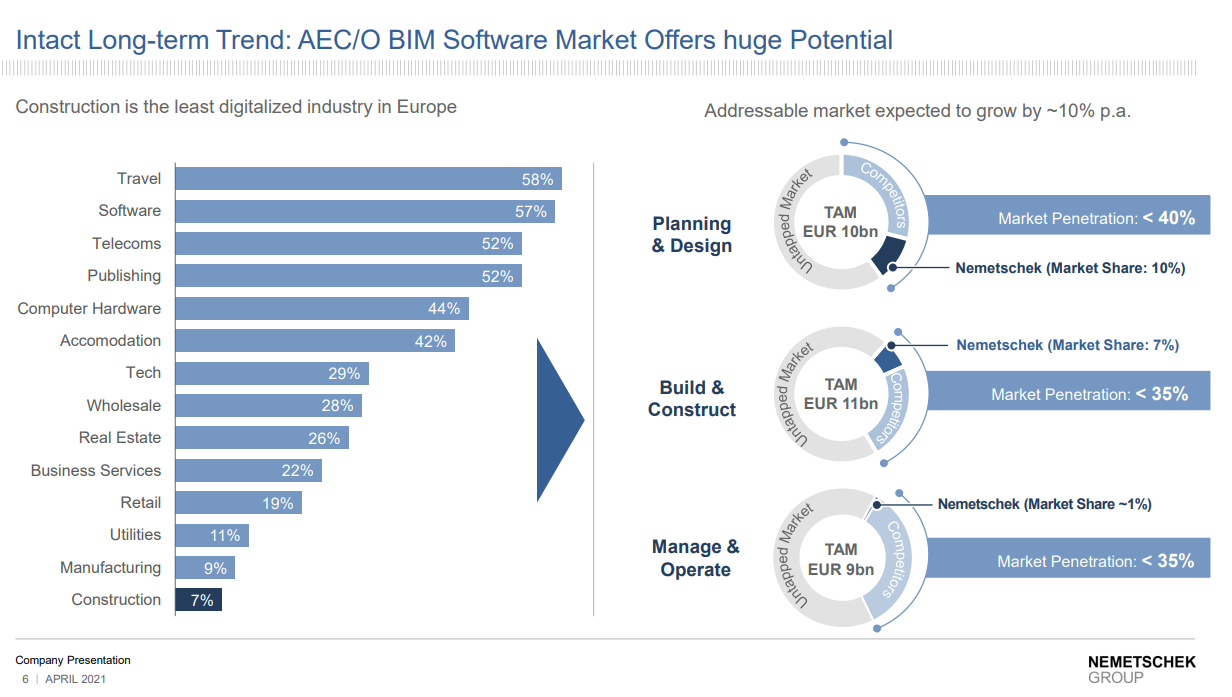

Yrityksen oma lyhyt esitys (vuodelta 2021): https://ir.nemetschek.com/download/companies/nemetschek/Presentations/NEMETSCHEK_Company_Presentation_0621.pdf

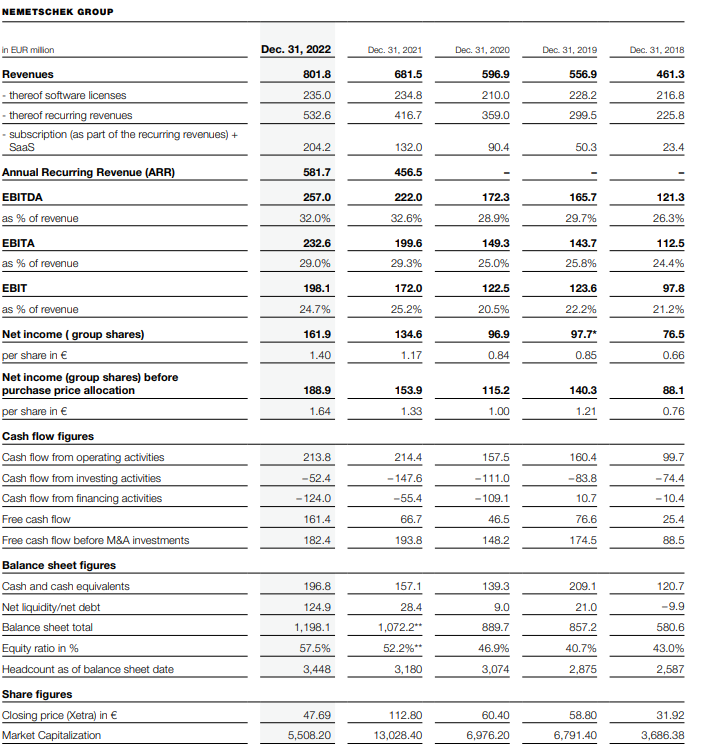

Tuoreimmasta vuosiraportista näkee mukavasti useamman vuoden lukuja.

Vuosiraportti 2022: https://ir.nemetschek.com/websites/nemetschek/English/51/annual-report-2022.html

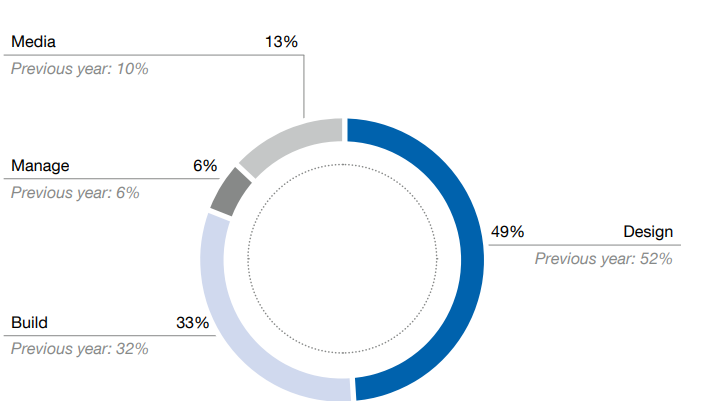

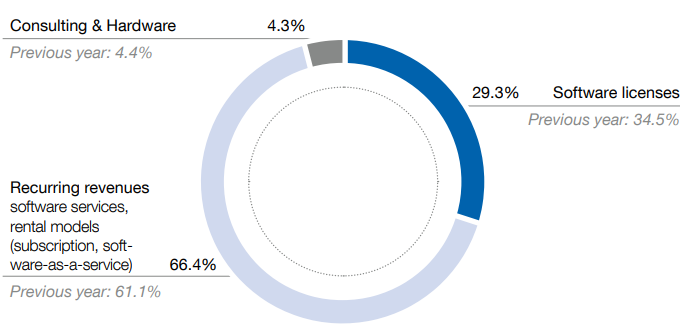

Liikevaihto segmentit

RR on ollut nousussa viime vuodet ja tähän panostetaan.

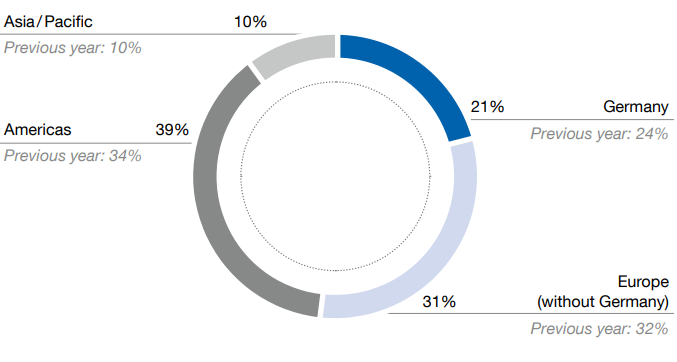

Liikevaihdon maantieteellinen jakauma

Nemetschek julkaisi Q1 2023 raportin muutama päivä sitten, linkki raporttiin tässä: News Detail | NEMETSCHEK