I’ve created a dedicated thread for Mendus, but my English is poor and I don’t know the industry at all, so there are bound to be mistranslations and misunderstandings. I looked up information on Inderes’ site, especially from the extensive report. Naturally, I googled for info and looked at things on the company’s website, etc.

Mendus develops cancer immunotherapies focusing on preventing tumor recurrence, which is the most common cause of cancer deaths worldwide. The targets are acute myeloid leukemia, ovarian cancer, and soft tissue sarcomas. The company’s previous name was Immunicum, and it was renamed Mendus after a merger with the Dutch private company DCprime in 2021. Today, Mendus is headquartered in Stockholm, while its actual operational activities are in Leiden, the Netherlands.

Core Competence and Strategic Focus

Mendus’ core competence is in dendritic cell biology, which is utilized in designing active immunotherapies based on living cells. The products are designed to build a long-lasting immune response against cancer. The company is strategically focused on cancer maintenance treatments aimed at extending disease-free survival and overall survival in cancer types where the risk of recurrence is high.

Product Development and Clinical Trials

Mendus’ lead product, vididencel, is derived from the company’s own cell line, making the product readily available and highly scalable. Vididencel has been primarily developed as a maintenance treatment for acute myeloid leukemia. Data published so far show that vididencel has a favorable safety profile, and promising signs of efficacy have also been seen in a Phase II study.

The company has collaborated with the Australasian Leukaemia and Lymphoma Group (ALLG) to expand the clinical development of vididencel. This AMLM22-CADENCE study is a controlled combination study with oral azacitidine, which is currently the only approved AML maintenance treatment.

Additionally, Mendus is investigating vididencel in solid tumors in the ongoing ALISON Phase I study in ovarian cancer. Results obtained so far support the product’s benign safety profile and show induction of immune responses in ovarian cancer patients.

Well… what should an investor consider:

There is potential in Mendus’ products if clinical development and the subsequent market entry are successful. Then again, there’s probably always potential in everything if you think about it enough. ![]()

Potential returns may be realized through favorable partnerships or acquisitions. On the other hand, the risk profile is high, especially due to research and development risks, so an investor can lose their money.

The company is not really generating revenue at the moment, but its financial potential is significant if vididencel and other products achieve market success. Mendus estimates its target market to be approximately 9.5 billion US dollars, and the market is expected to grow by over 8% annually until the end of the decade.

Mendus is an interesting player in the biotechnology sector, especially in the field of immuno-oncology. The company’s focus on maintenance treatments and its strong scientific background provide a solid foundation for future growth and success. Mendus also “offers” significant risks—I’ll repeat this because it is quite a risky company.

Here is a relatively recent extensive report from April by Antti Siltanen. ![]() As usual, there are no paywalls for this report; it is readable for everyone.

As usual, there are no paywalls for this report; it is readable for everyone. ![]()

Mendus is a clinical-stage biotechnology company developing cellular immunotherapies for cancer. The company aims to improve disease-free and overall survival in cancers with a high recurrence rate. Its lead product, vididencel, is being developed as maintenance therapy for acute myeloid leukemia (AML) and is about to enter a Phase II clinical trial. As a pre-revenue company, Mendus’ risk profile is high, as unfavorable research results can lead to a permanent loss of capital. These risks are offset by significant upside potential if commercialization is successful. Our DCF model suggests upside for stock while relative valuation is in line with Nordic peers. The stock’s upside could be realized via a partnering deal or Mendus becoming an acquisition target.

https://www.inderes.fi/research/keeping-cancer-in-check

Then here is a bit of a chat between Sara and Antti about the company from three months ago. Subscribe to the Inderes Nordic channel, and Inderes will thank me. ![]()

https://www.youtube.com/watch?v=whU0z9tZZgM

@Isa_Hudd’s CEO interview can be found here:

https://www.youtube.com/watch?v=wOOR5LYFtV0

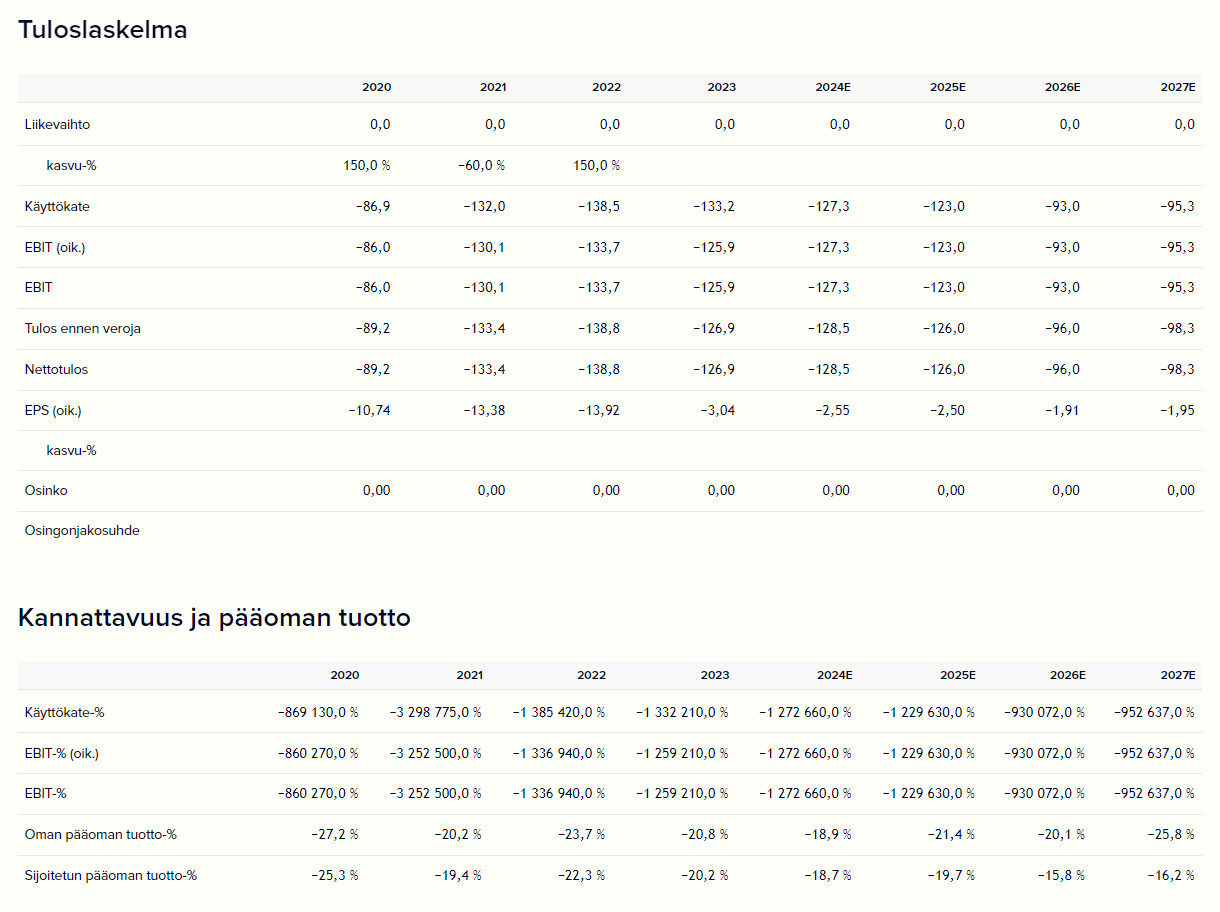

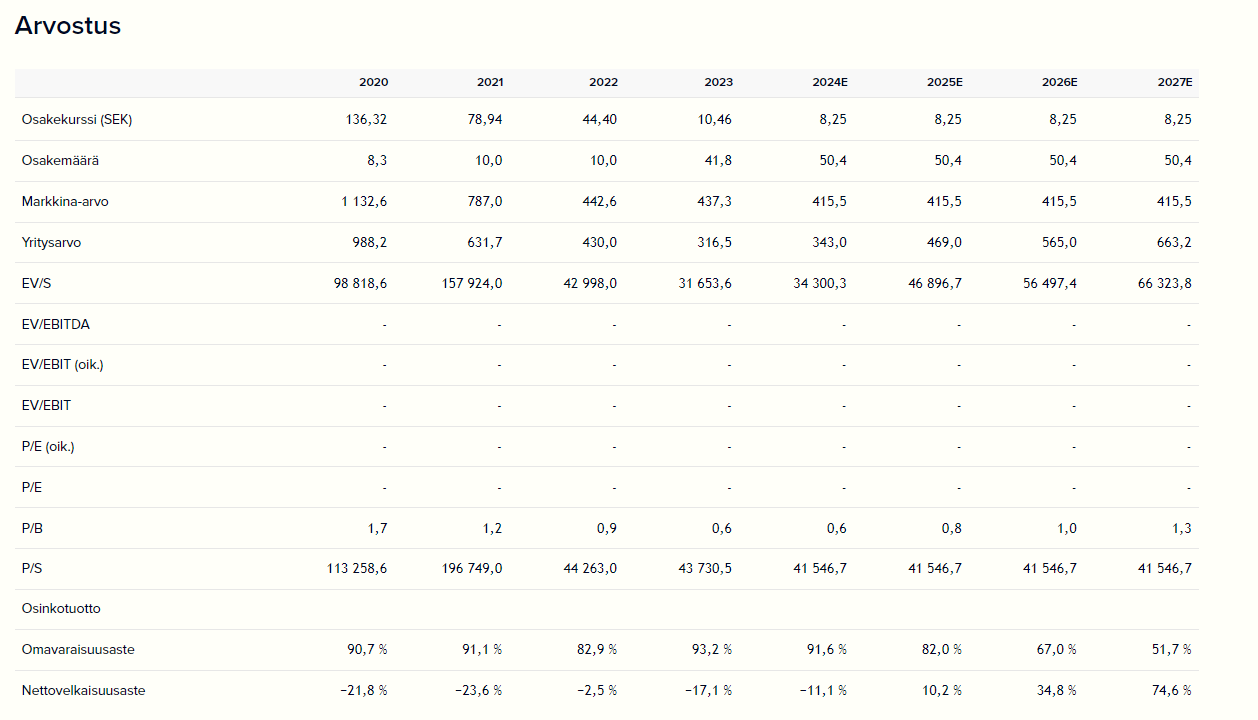

Taken from Inderes’ website: