The dividend target is also mentioned in the demerger prospectus, if you just bother to read it ![]()

57 Likes

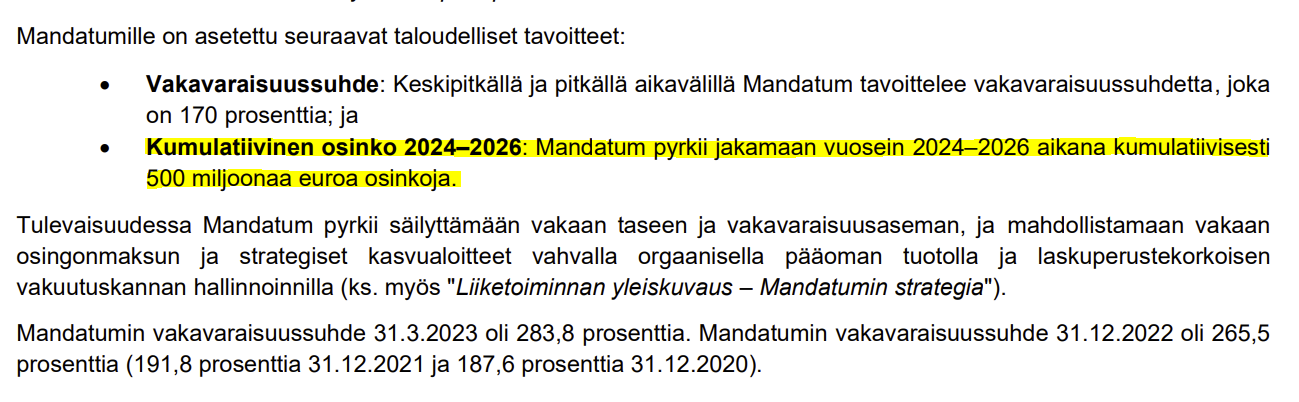

As I understand it, Mandatum will have a 1:1 share count with Sampo, i.e. approx. 555 million shares. Doing some quick math based on what Mirko pointed out, that would result in €166M in dividends per year, or approx. €0.30/share/year.

From that, one could calculate the net dividend for their own number of shares. We’ll see where the share price and thus the dividend yield eventually settles.

5 Likes

Sampo has 510,977,769 shares (https://www.sampo.com/investors/share/), some of which may still be cancelled before the demerger. Based on those figures, dividends over three years would be roughly €0.98/share, as the target is to pay €500M cumulatively. One could estimate, for example, €0.3, €0.33, and €0.35. If the share price is the planned €4.89 (~€2.5bn market cap), it will certainly be quite a reasonable dividend machine.

5 Likes

9 Likes

Just as a side note: 265.5% 2022 YE SII Ratio (2,342 / 942)…

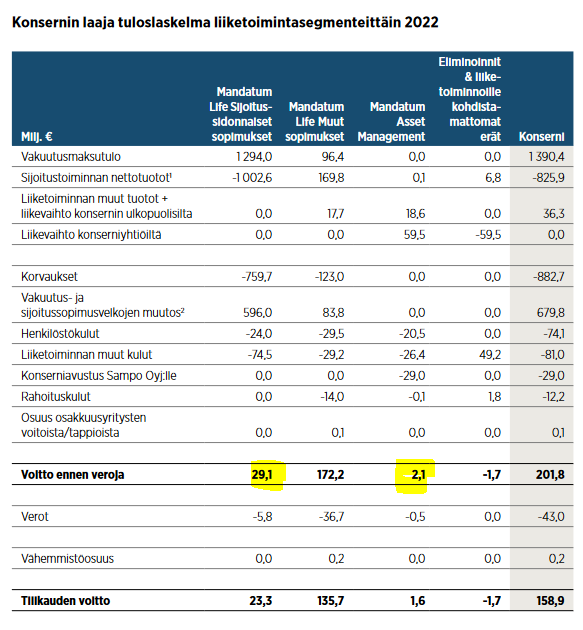

…if that were released immediately to the 170% level… the dividend would be 740 MEUR.

A few points:

- Apparently, acquisitions are being planned

- There are some rumors going around that Mandatum’s so-called fixed-rate run-off portfolio is also significantly more profitable than new sales, meaning that as a counterweight to the capital release, there would also be downward pressure on earnings (which in turn puts pressure on acquisitions to maintain the earnings level)

- Management will probably clarify the situation at some point; that dividend target combined with the 170% target (and the run-off portfolio) is quite low (though earnings capability is also a question mark)

7 Likes

Maybe this shows more clearly where the profits are made; and where the rumor stems from…

…it will be interesting to see how Mandatum starts reporting its results; Q2 is likely the first report.

2 Likes

Please note the -29MEUR group contribution to Sampo plc in Asset Management. This item will be eliminated when the demerger takes place.

16 Likes

Fair point, see also the maneuvering with personnel costs 2022 vs. 2021 (investment-linked). The point was mainly just to point out that most of the result approaches zero in the long run - growth in UL and asset management should narrow the profit gap of the run-off portfolio.

5 Likes

Inderes’ latest estimate of Mandatum’s value is EUR 2,328 million. At the end of September, there are 502 million Sampo shares. So from this, we get an estimate that Mandatum’s price would be EUR 4.637/share, and if the dividend were 0.332 for the first three years, then that results in a 7.159% dividend yield for the first three years. [figures corrected]

37 Likes

…dividend yield per year for the first three years ![]()

7 Likes

The share of asset management is indeed very small. I wonder if it will be sold off or if it’s an important part of the life insurance service package. Manta could probably also buy something to strengthen its asset management.

2 Likes

This is a good time to revisit this, a couple of months later ![]()

I have come to the understanding that asset management is specifically where more effort will be focused in the future. This will likely become clearer once Mandatum holds some kind of roadshow before the demerger. Let’s also include Sampo-Mirko’s comment from that other thread!

7 Likes

Mandatum’s investor event on Thursday, 14 September: Mandatum järjestää sijoittajatilaisuuden 14.9.2023 | Kauppalehti

21 Likes

Let’s put this in this thread as well. A supplement to Mandatum’s demerger prospectus has been published, which includes updated and new financial targets and plenty of other information that will be discussed in more detail at the investor event on 14 September 2023.

20 Likes

Is it just me, or does that ample ~300% solvency ratio and almost +9% net inflows for H1–23 look quite promising, at least in terms of dividend yield — given that the target solvency level is 170–200%?

Please note that the 296% solvency ratio at the end of H1/2023 does not include the Saxo, Enento, etc. arrangements. Taking those into account, the solvency ratio was 232%.

13 Likes

Ah OK. Well, still quite nicely above. On the other hand, let’s hope that some other use is found for the capital besides dividends…

Based on net asset value or, alternatively, based on fair values (the average price of the first day or the first five days) if this deviates significantly from the net asset value allocation ratio. The tax authorities will then confirm the allocation after the demerger.

15 Likes

I’ll add to this regarding the tax authority’s confirmation. This usually takes a few months, so it’s unlikely we’ll get this information in October, but probably within this year.

On that note, I should say that I’ve been so damn busy with work that I haven’t had time to read those supplements! I wonder if there will also be a recording of Manda’s first investment event?

3 Likes

A recording of the event will be made available.

11 Likes