Ennustaja ku olis nii me kaikki oltais miljonäärejä.

39 tykkäystä

Viimeiset 10 vuotta indeksiltä turpaan, ei vaikuta hyvältä!

3 tykkäystä

Tässä on kyse ainoastaan reverse to mean-efektistä. Inderes ei osaa ennustaa yhtään paremmin kuin kukaan muukaan; alussa kävi tuuri ja niin kuin pokerista tiedetään, pitkässä juoksussa tuuri tasoittuu.

3 tykkäystä

Olen miettinyt tätä myös samalla tavalla. Teoria on ihan mahdollinen. Paljon on lopulta myös tuurista kiinni.

Toinen mahdollinen teoria on se, että mallisalkkutiimi on vaihtunut alkuajoista ja nykyisen tiimin taso ei ole yhtä laadukas kuin se oli vuosina jolloin kaulaa indeksiin vedettiin. Tätä on ikävä sanoa ääneen eikä tarkoitus ole ketään mollata, mutta jos uskoo että osakepoiminnalla voisi ylituottoa saada (ilman erityisen hyvää tuuria), täytyy myös uskoa siihen, että poimijoiden kyvyissä esiintyy eroja.

Nämä teoriat ei poissulje toisiaan ja voivat päteä yhtäaikaa. Aluksi on ollut parempi tiimi hyvällä tuurilla ja nyt edellistä huonompi tiimi huonommalla tuurilla. Graafista näkee lopputuloksen.

Edit: Erilaisia vaihtoehtoja on toki muitakin. Voihan se olla että nykyinen tiimi on paljon kyvykkäämpi, mutta vaan todella epäonninen. Jos ilkeästi haluisi mollata niin sanoisi, että täysin kyvytön, mutta hyvän tuurin ansiosta päädyttiin nykyiseen suoritukseen (hyvin epätodennäköinen vaihtoehto). Vaatii todella pitkän ajan jotta tuurin osuuden voi ohittaa.

8 tykkäystä

Henri Huovinen pohtii tätä ajan merkitystä:

https://x.com/HenriHuovinen2/status/1997708661351739465?s=20

“Jos siis salkun annualisoitu volatiliteetti on 20 prosenttia (mikä on hieman enemmän kuin S&P 500 -indeksin historiallinen keskiarvo), viiden prosentin vuotuinen alfa vaatii noin 62 vuoden sijoitushorisontin”

5 tykkäystä

Pitää aina muistaa, että indeksin voittaminen pitkässä juoksussa, esim 20-30v ajanjaksolla on erittäin vaikeaa. Siihen kykenee hyvin hyvin harva ammattilainen. Tämänkin palstan kirjoittajista lähes jokainen häviää indeksille vuosikymmenten ajanjaksolla. Jos puhutaan lyhyemmästä, vaikkapa 10 vuoden ajanjaksosta, niin onnella on hyvin iso osuus saavutettuun menestykseen.

Eli jos mallisalkku kykenee voittamaan indeksin 20+ vuoden ajanjaksolla, niin kova on suoritus. Lanttiakaan sen puolesta ei kuitenkaan kannata vetoa lyödä.

2 tykkäystä

Minusta se taas on hyvin helppoa. Ostaa kaikkia indeksiin kuuluvia osakkeita, mutta jättää muutaman surkeimman ja lähitulevaisuudessa konkurssiin kaatuvan pois. Tuollaisen mallisalkun seuraaminen vaan äärettömän tylsää, niin pitää yrittää poimia voittajia häviäjien poisjättämisen sijaan.

1 tykkäys

Toivoisin mallisalkkuun ehkä jonkin sortin strategiaa ja tavoitteita. Pelkästään “poimitaan randon yrityksiä joiden tilinpäätös näyttää hyvältä” ei ehkä ihan riitä. Näkisin että aika paljonkin markkinoilla on voitettavaa jos seuraa esim megatrendejä tai eri toimialojen kehitystä.

1 tykkäys

“Salkkumme tukijalkana toimivat laadukkaat, kestäviä kilpailuetuja omaavat ja omistaja-arvoa luovat yhtiöt.”

Kyllä tuohon megatrendit sijottuu. Suomen pörssissä ei vaan ole Microsofteja yms. megateknoa tarjolla.

“mutta jättää muutaman surkeimman ja lähitulevaisuudessa konkurssiin kaatuvan pois.”

Mitä nämä “muutamat” kaatuvat firmat ovat? Niinpä niin, sitä kun emme tiedä.![]()

Henkilö, joka kykenisi kyvyillään varmuudella lyömään indeksin vuosikymmenestä toiseen voi valita työpaikkansa sijoitusmaailmassa tuhdin tilipussin kera.

Mutta ei tästä sen enempää, kukin yrittää tavallaan ja toivotaan mallisalkulle menestystä.

1 tykkäys

Omistaja-arvoa ei ole ainakaan luotu enää pitkään toviin, pitäisikö teesejä siis vaihtaa?

1 tykkäys

Ei yritäkään ostaa laadukkaita firmoja enää? Eiköhän nämäkin salkussa olevat firmat ole ihan sääntöjen tapaan vielä salkussa. Ei ole myyntisuosituksia. Teesin vaihtoa toiseen firmaan ei siis voi tehdä.

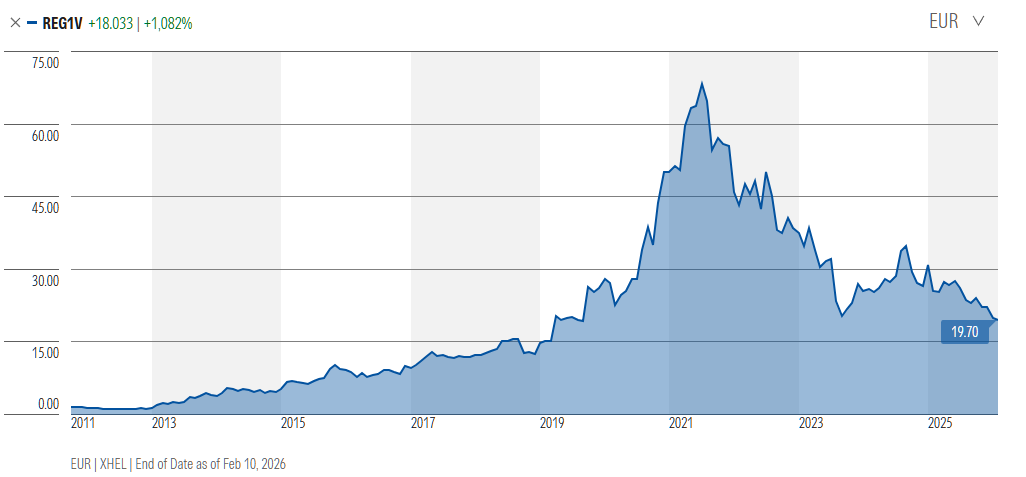

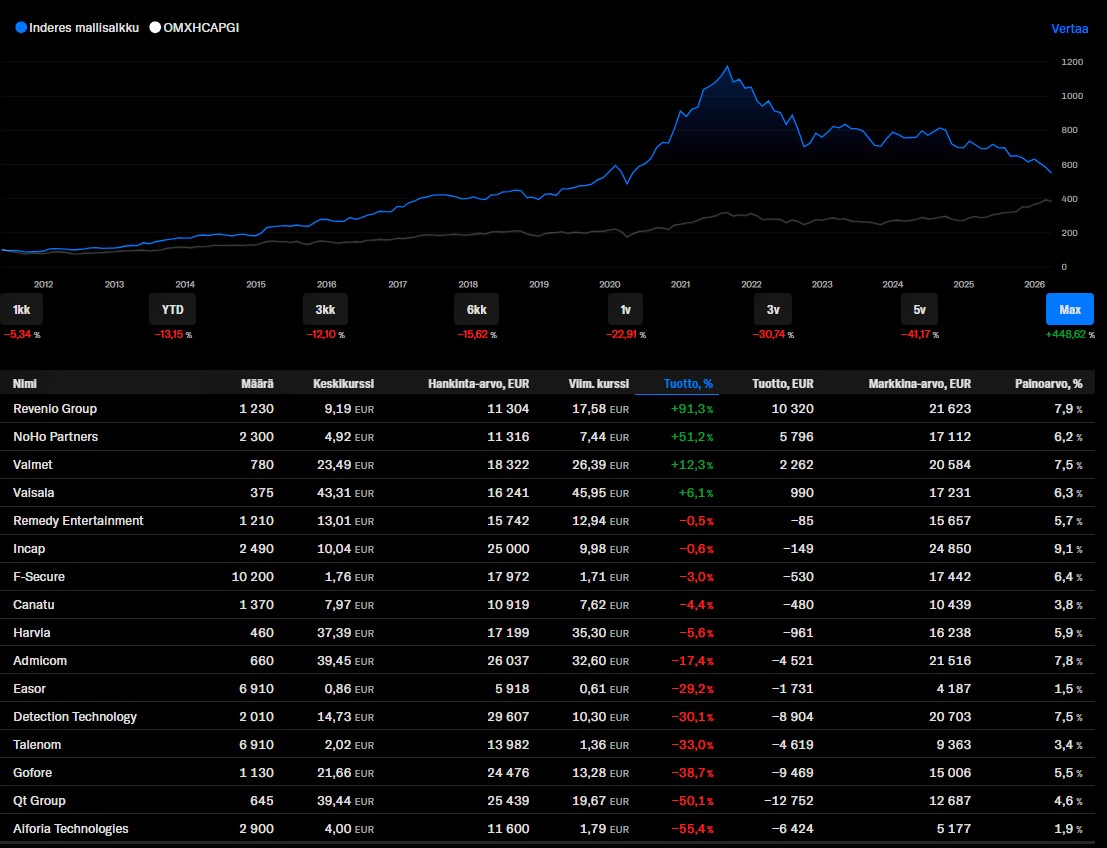

Inderesin mallisalkku etsi alussa linjaansa, mutta pian se keskittyi itseasiassa yhtiön omaan core-bisnekseen, eli kotimaisiin pienyhtiöihin. 10+ vuotta sitten pienet yhtiöt eivät olleet ihan yhtä analysoituja ja seurattuja kuten nykyään, ja näistä oli löydettävissä todella hyviäkin pelipaikkoja. Mallisalkku teki muutaman todella hyvän diilin ja oli sanoisinko kovassa maineessa. Mainittakoon vielä salkun kruununjalokivi Revenio jonka kurssikehitystä voi vaikka verrata mallisalkun kehitykseen.

Aiemmin, varmaan vuoteen 2021 asti tuli välillä seurattua mitä mallisalkussa on touhuttu, koska tatsia tuntui olevan. Sen jälkeen seuraaminen on jäänyt. Kun nyt vilkaisin salkun sisältöä ja tuottoja, niin eipä näyttänyt kovin mairittelevalta.

6 tykkäystä

Harvia, josta mallisalkku luopui olisi omasta mielestäni ollut eniten tuon salkun ”strategian” mukainen lappu. Jonkinlainen trendikin saunomisen osalta maailmalla jne. Toki arvostuksesta voi olla montaa mieltä

5 tykkäystä

Näyttäisi, että 1.5.2015 ero indeksiin oli jo revennyt nykytasolle.

Mutta toki on väärin sanoa, etteikö sen jäljeen olisi tehty ylituottoa. Ylituottoa tehtiin melko vakuuttavaan tahtiin aina 2021 syyskuuta saakka. Tämän jälkeen markkina alkoi hinnoitella muuttuvaa korkoympäristöä ja eikä mallisalkun strategia ole sen jälkeen toiminut.

IMO mikäli tälläisia pitkiä alituottojaksoja haluaa vältää, stratgiassa tulisi olla makroanalyysiä ja ehkä myös teknistä analyysiä mukana. Helppoa jälkiviisastella, mutta ei siinä lopulta olisi tarvinut kuin oivaltaa, että nousevat korot ovat kasvuyhtiöille myrkkyä ja tälläisessä ympäristössä voittajia ovat esim. pankit ja vakuutusyhtiöt.

5 tykkäystä

Viesti yhdistettiin ketjuun: Mitä sinulla on salkussa?

9 tykkäystä

Inderesin mallisalkulle v**tuillessa on toki reilua todeta, että mulla on itsellä QT:tä salkussa, mutta ei Nestettä. Viimeksi mainitut myin halvemmalla (mutta hei, ihan omani sain takaisin) pois kuin Inderes. Ensiksi mainituista en sentään maksanut sellaista hintaa kuin Inderes viimeisen ostokerran aikaan.

5 tykkäystä

Mallisalkussa Qt on lähes puolittunut. Nyt se olisi osta-suosituksella. Olisiko aika tuplata Qt omistus jos luottoa löytyy? Klassinen keskihinnan alennus. On se nyt tänään jo järkevämmän hintainen vaikka itselleni vielä liian kallis.

13 tykkäystä

Koronan aikaan kun aloitin sijoittamisen, ihailin suuresti inderesin mallisalkkua ja se toimi itselleni esikuvana mihin kaikkeen erinomainen osakepoiminta voi viedä ja iso syy miksi halusin nimenomaan alkaa poimimaan osakkeita ja haastamaan itseäni indeksiin sijoittamisen sijaan.

Historia ei kuitenkaan ole tae tulevasta, ja inderesin mallisalkun 2021 alkanut alamäki ei näytä helpottavan ja tätä menoa lähivuosina pääsemme tilanteeseen jossa Suomi-indeksi ohittaa salkun, jonka kokisin olevan valtava epäonnistuminen mallisalkulta. Siinä vaiheessa itse ainakin viimeistään vakavasti harkitsen osakepoiminnan lopettamista ja siirtymistä indeksisijoittajaksi.

25 tykkäystä