Miksi ei tenbägännyt Bittium kuulunut Inderesin Mallisalkkuun? Olisi sopinut sinne monella tapaa

1 tykkäys

Ollu VÄHENNÄ suosituksella eiliseen asti!! Merkit,merkit,merkit,merkit,merkit

7 tykkäystä

Nokian Renkaat on noussut noin 50 % vain neljän kuukauden kuluessa siitä, kun osake myytiin mallisalkusta.

12 tykkäystä

Juu, en ole seurannut mallisalkkua kuin vain harvoin ja sivusilmällä, eikä se mua kiinnosta, enkä halua mollata mallisalkkua, mutta sen on aivan järjetön viritelmä sääntöineen, salkuhoitajineen ilman punaista lankaa, vähintäänkin yhtä huono kuin 99% Suomi-osakerahastoista ellei huonompikin.

Ihmettelen: miksi kukaan aloittava tai kokemusta omaava sijoittaja käyttäisi yhtään omaa arvokasta aikaansa tai energiaansa mallisalkkuun - parempaa infoa löytyy tälle ajalle vaikka seleemalla yhtiökohtaisia palstoja

3 tykkäystä

Vastaan tähän sellaisena ihmisenä, joka on enemmän tai vähemmän sijoittanut Mallisalkun mukana osin jo vuodesta 2020 alkaen. Energiaa tähän käytän siksi, että mielestäni ”aihio” aidosti markkinat selvästi hakkaaviin tuottoihin on olemassa. En itse näe, että mihin esim. @Juha_Kinnunen tietotaito osakemarkkinoilla olisi yhtäkkiä kadonnut savuna ilmaan, vaan sen takia, että pienempien firmojen (joihin Mallisalkku pääosin ainakin minun mielestä vaikuttaa sijoittavan) voittokulku on brutaalisti katkennut viime vuosina (ks. FNFIEURGI-indeksiä vaikkapa). Lisäksi epäonnistumisista suurin osa on selitettävissä ihan algoritmisesti sillä, että useimmiten yksi teesi oston/myynnin suhteen on mennyt metsään (mistä on seurannut casen pieleen meneminen ja alituotto), mitä nyt väistämättä tapahtuu kenelle tahansa sijoittajalle.

Näkisin, että hyvin paljon todennäköisempi vaihtoehto krooniselle alituotolle Mallisalkulle on vain pitkittynyt huonompi jakso, joita tulee kaikille sijoittajille ennemmin tai myöhemmin. Tämä siis nykyisillä tiedoilla arvioituna. Historiallisesti kuitenkin Mallisalkku on piessyt vertailuindeksinsä oikealta ja vasemmalta, enkä näe, että tämän jatkumisen mahdollisuus olisi mihinkään maagisesti kadonnut tämän Hesulin pikkuyhtiöiden surkeuden keskellä.

25 tykkäystä

Kuten mainitsin, toin esille vain ihmetyksen - enkä tuomitse salkun tuottajaa enkä aliarvioi salkun hyödyntäjiä. Se on kuitenkin fakta, että alituottoa on ollut ei vain yksi vuosi vaan useampi, ja menestyksekäs alkutaipale on historiaa. Viimekädessä meistä jokainen on just niin hyvä sijoittaja kuin - jos ei nyt viimeisin sijoitus, niin ainakin viimeisin vuosi ! Katsotaan @Johannes_Sippola argumentointiasi sitten taas vuoden päästä -”mihin tietotaito osakemarkkinoilla olisi yhtäkkiä kadonnut…” Toivottavasti olen väärässä ja se on palannut, mutta sallittakoon myös epäillys sen suhteen.

ps. en todellakaan ymmärrä argumentointiasi lause “algoritmisesti, sillä, että useinmiten yksi teesi …” Mitä algoritmisesti tähän liittyy ja hyvänen aika, salkkuhan on kokonaisuus, olipa yksi teesi vienyt tai tuonut tuottoa, ja lopputulos on aina kokonaisuus. Tsemppiä kaikille kuitenkin tekemiseen ja uskonluomiseen, katsotaan mieluummin tietty aina eteenpäin.

2 tykkäystä

Silläkin on merkitystä että mitä on otettu tilalle. Kai sielä joku parempi kohde oli? En oo seurannut…

1 tykkäys

Joo en noin tarkasti katsonut, aina pitää vähän liioitella ![]() Tilalle tais tulla Vaisalaa joka ei ole oikein liikkunut mihinkään. Vaisala toki erittäin laadukas yhtiö ja varmasti hyvä pitkässä pelissä.

Tilalle tais tulla Vaisalaa joka ei ole oikein liikkunut mihinkään. Vaisala toki erittäin laadukas yhtiö ja varmasti hyvä pitkässä pelissä.

4 tykkäystä

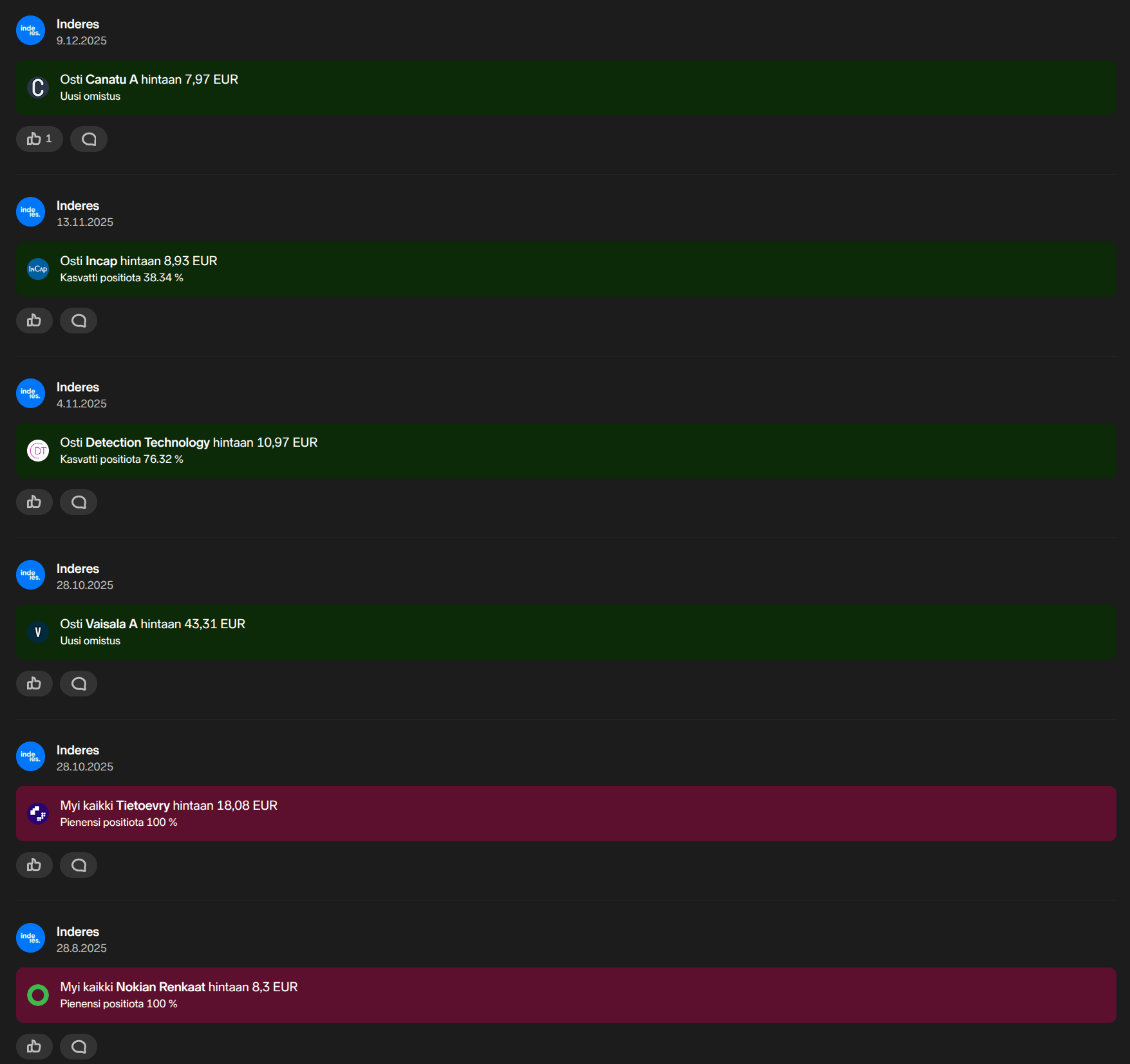

Kyllä sieltä ihan hyviä poimintoja on lyhyen aikavälin tarkastelulla tullut. Parhaana Canatu 18% nousulla, mutta ei niin loistavia, että se riittäisi paikkaamaan rinkuloiden huonosti ajoitettua myyntiä.

Mallisalkku kaipaisi teknistä analyysiä mukaan tekemiseen. Nyt myydään ja ostetaan liiaksi momentumia vastaan.

9 tykkäystä

Mallisalkun vuosikatsaus julkaistu, käydään tällä viikolla tätä tarpomista vielä videolla läpi ![]()

38 tykkäystä

Hellou Mallisalkkutiimi! Olen edelleen fani, ja vaikka suoriutuminen on ollut heikkoa, on Aten hauis oikeasti livenä vieläkin isompi kuin ruudulta katsottuna näyttää. Huhhuh.

Muutama asia, jota itse havahtunut pohtimaan omissa sijoituksissani. Koen, että ainakin itselleni hyvä keino oppia kun käy muutamia asioita itsensä kanssa läpi, joko peilin edessä tai sitten ihan vaikka ratin takana körötellessä töistä kotiin.

-

Mitkä olivat konkreettisesti suurimmat syyt heikkoihin muutamaan vuoteen? Oliko vika ostojen ajoituksella, oliko teesit väärät ja kärähtikö siellä yhtiöissä tulostaso vai arvostustasot? Etenkin case Neste sai miettimään (myin myös duffella!

), että miksi takinkääntö, eikä käytännössä edes katsottu sitä omaa teesiä maaliin asti (uusiutuvien ykkönen).

), että miksi takinkääntö, eikä käytännössä edes katsottu sitä omaa teesiä maaliin asti (uusiutuvien ykkönen). -

Heikkojen päätösten perustelut: miksi (peräpeiliin katsottuna) jokin selkeä virheellinen päätös on tehty? Muutama epämiellyttävä keissi, kuten Harvian myynti, Nesteen myynti ja Nokian renkaiden myynti ovat jääneet monille kummittelemaan (epäilemättä myös teille) Miksi myynnit ovat olleet epäonnistuneita? Onko Ruoholahdessa liikaa yritystä markkinan ajoittamiseen?

Onko kyseessä ollutkin enemmän myynnit turhautumiseen, kun varsinaiseen teesiin heijastaen (toki NR kohdalla hyvin perustelitte, miksi teesi olikin murentunut). Silti en usko, että edes ammattianalyytikot olisivat immuuneita tunteilulle, ja joskus päätöksiä voi tapahtua silkasta turhautumisesta markkinan oikkuihin. "The market can stay irrational longer than you can stay solvent."

Onko kyseessä ollutkin enemmän myynnit turhautumiseen, kun varsinaiseen teesiin heijastaen (toki NR kohdalla hyvin perustelitte, miksi teesi olikin murentunut). Silti en usko, että edes ammattianalyytikot olisivat immuuneita tunteilulle, ja joskus päätöksiä voi tapahtua silkasta turhautumisesta markkinan oikkuihin. "The market can stay irrational longer than you can stay solvent." -

Onko huonot vuodet saaneet varovaisemmaksi allokaation puolelta? Nyt positiot ovat kesyjä alta 10% per rivi. Pelätäänkö näpeille tulemista, vai eikö meillä ole Hesulissa mitään selkeää “tällä tehdään tuottoa”- tilaisuutta?

-

Heikki Keskivälin sanoin, kuinka kääntää (edellisvuosien) tappiotkin voitoiksi? Minkä asian on muututtava? Vaikka pitkän ajan träkki edelleen hivelee silmää, vuosi kerrallaan kun eteenpäin mennään, sen taakse piiloutuminen on entistä hankalempaa.

Kaikki nämä ilman sarvia ja hampaita! En tiedä, onko näissä mitään oikeasti vastattavaa, mutta jos herättää mitään ajatuksia niin… ![]()

E. Meinasin jo lopettaa, mutta humanisti sisälläni huutaa kysymään myös mentaalipuolta!

- Olkoon asteikko 1-10 (1 = ei tunnu missään, 10 = oon ihan patakinnas, pitäisi vaihtaa alaa), kuinka pahasti heikko suorittaminen ja foorumilla mallisalkkuun kohdistuva naljailu menee ihon alle? Ollaanko siellä täysin teflonia, vai onko välillä läppärin kannen sulkiessa sellainen olo, että vittu tulkaa itse tekemään paremmin.

34 tykkäystä

Pari huomiota:

-

Mallisalkun painossa korostuvat pienet yhtiöt ja ne ovat pärjänneet heikommin viime vuosina.

-

Inderesin analyyseissä nähdäkseni yrityksen “intrinsic value” saa liian vähän huomiota. Turvallisuusmarginaali eli arvon ja hinnan välinen ero on hyvä lähtökohta sijoittamiselle. Toki arvon määrittäminen on vaikeaa.

5 tykkäystä

Seurannassa olevista firmoista 16/171 on ulkomaisia, joista puolet on osta- tai lisää-suosituksella. Milloin saadaan seurannassa olevat ulkomaiset firmat mukaan mallisalkun sijoitusavaruuteen?

Mallisalkun firmoista ainoastaan yhdella on vähennä- tai myy-suositus. Löytyykö salkusta positioita, joiden kanssa koette olevanne jumissa suosituksista johtuen?

Löytyykö sijoitusavaruudesta osakkeita, joita tekisi mieli ostaa, mutta suositus on “väärä”?

Perustuuko osakkeiden osto- ja myyntipäätökset puhtaasti fundamentteihin vai hyödynnättekö teknistä analyysiä mitenkään?

Mikä on mallisalkun tuotto-odotus vuodelle 2026?

9 tykkäystä

Mille mallisalkun riveistä teillä on ladattuna eniten odotuksia vuotta 2026 ajatellen?

5 tykkäystä

Gofore on vähennä suosituksella, joten mallisalkku pystyisi halutessaan nämä myymään. Eroaako Jonin ja mallisalkkutiimin näkemys Goforesta vai onko ero pelkästään ajallinen? Katsooko mallisalkkujengi Goforea vuosien päähän kun Jonin suositus perustuu lyhyemmälle aikaperiodille?

Mallisalkun on vaikea tehdä nopeita liikkeitä, mutta oletteko miettinyt eri kohteille mikä olisi syy myydä kohde heti laitaan jos vaan sen pystyisi tekemään? Esim. jos kasvuyhtiöksi mielletty ja salkkuun siksi ostettu kohde ei kasvattaisi liikevaihtoa tms. asia missä oma sijoitusteesi alkaa hajota. Asia mitä joskus itsekin teen on se, että syy omistaa muuttuu matkalla, mutta positio pysyy. Sijoitusteesi muuttuu toivotaan toivotaan moodiin. En sitä ostaisi salkkuun, mutta kun on jo niin myyntinappia ei löydy. Välillä se on viisasta ja välillä ei, mutta yleensä teesin rikkoutuessa olisi parempi ottaa exit. Pahimmassa tapauksessa kallis kasvuyhtiö muuttuu arvoyhtiöksi ja siitä käänneyhtiöksi ja siitä kriisiyhtiöksi. Annie Duke puhuu tästä aiheesta termillä kill criteria. Talenom lienee ainakin jotain muuta mitä mallisalkku luuli ostaneensa eikä siitä luovuttu, vaikka se oli vähennä suosituksella. Mikä on Talenomin kill criteria?

20 tykkäystä

Onko foorumin paineessa pitkäjänteisyys unohtunut?

Löytyykö seuratuista yhtiöistä kassavirtapohjaista paremmuus järjestystä? Miten mallisalkun yhtiöt on siinä sijoittuneet?

11 tykkäystä

Ja täältä tulee uusin Mallisalkku-video ![]()

Aiheet:

00:00 Aloitus

00:19 Mallisalkun musta vuosi

05:59 Syitä heikkoihin tuottoihin

15:25 Asteikolla 1-10, miltä nyt tuntuu?

18:41 Viimeisimpänä Canatua salkkuun

21:56 Yksittäisten rivien koko

24:15 Gofore

28:04 Talenom

31:06 Suositukset ja Mallisalkku

35:38 Lähtökohdat ja odotukset vuodelle 2026

41:00 Isoimmat odotukset Mallisalkussa

43:47 Mallisalkun tuotto-odotus

46:00 Ulkomaiset yhtiöt

46:51 Fundamentit ja tekninen analyysi

26 tykkäystä

Videon esittelykuva on kyllä hieno ![]() pitää vielä pistää video katsellen

pitää vielä pistää video katsellen

9 tykkäystä

“Edellisessä vähennä suosituksessahan kävi sillä tavalla, että meidän karenssin aikana kurssi laski jo niin voimaakkaasti, ettei saatu lupaa myydä. Kysyttiin kyllä lupaa.”

“Tätä on tapahtunut siis aiemminkin.” -Juha

Mikäs sääntö tämä nyt on, ja miksi se on niin huonosti määritelty, että pitää erikseen lähteä kyselemään? ![]() Mikaeliltako näitä pitää käydä kyselemässä? Kyseessä oleva yhtiö oli siis Talenom, jossa Juha on vieläpä itse analyytikkona.

Mikaeliltako näitä pitää käydä kyselemässä? Kyseessä oleva yhtiö oli siis Talenom, jossa Juha on vieläpä itse analyytikkona.

Vähän surullista, kun Juha joutui toteamaan, ettei käytetä TA:ta, kun meillä ei ole valtaa ajoituksiin. Koita siinä sitten biitata indeksiä ![]()

Edit. Tämä kysymys vähän kierrettiin, kun kysyttiin ainoastaan, että minkä asian on muututtava? Vastaukseksi saatiin luonnollisesti, että salkun yhtöiden pitäisi alkaa performoimaan paremmin ja kasvattamaan tulosta ![]() Ituhippinen varmaan tarkoitti kysyä pikemminkin, että mitä mallisalkkutiimin tulisi tehdä toisin?

Ituhippinen varmaan tarkoitti kysyä pikemminkin, että mitä mallisalkkutiimin tulisi tehdä toisin?

6 tykkäystä