The company named Fleetcor came across my stockscreener earlier and piqued my interest. And for good reason. After that, I familiarized myself with Edenred, a peer probably more familiar to many of us. I was even more astonished. Did I find a goldmine? I’ve been poring over the financial reports of these two, and it strongly appears that the companies operate in a boring industry but with sexy profitability. Here’s a bit of Fleetcor in numbers:

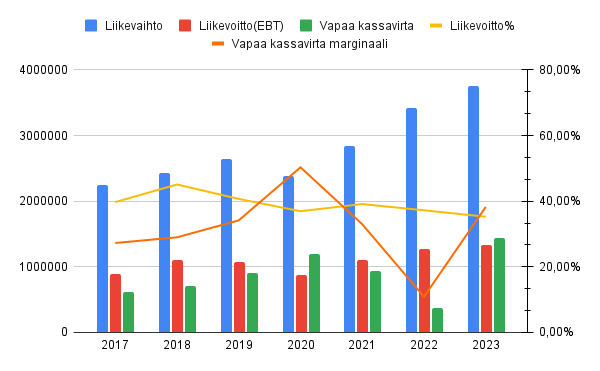

In the years 2017-2023:

- CAGR growth = 8.9%

- Operating profit margin on average = 43%

- Free Cash Flow to Equity (FCFE) margin on average = 32%

Not bad.

This business model heavily utilizes financial leverage, and the Altman Z-Score yields an average result. It is certainly not in the “danger zone,” but on the other hand, it last received a completely clean bill of health in 2018. The Beneish M-Score gives a clean bill of health for every year in the previous chart, so there’s no reason to suspect creative accounting on that front.

Valuation is not cheap by traditional metrics, but then again, the company’s performance hasn’t given any reason for such pricing either. At first glance, based on cash flow, the market prices the stock for growth roughly in line with inflation forecasts, with profitability as shown in the chart above. According to the company’s own estimates, there’s still a huge amount of TAM (Total Addressable Market) to grow into, so that doesn’t limit growth.

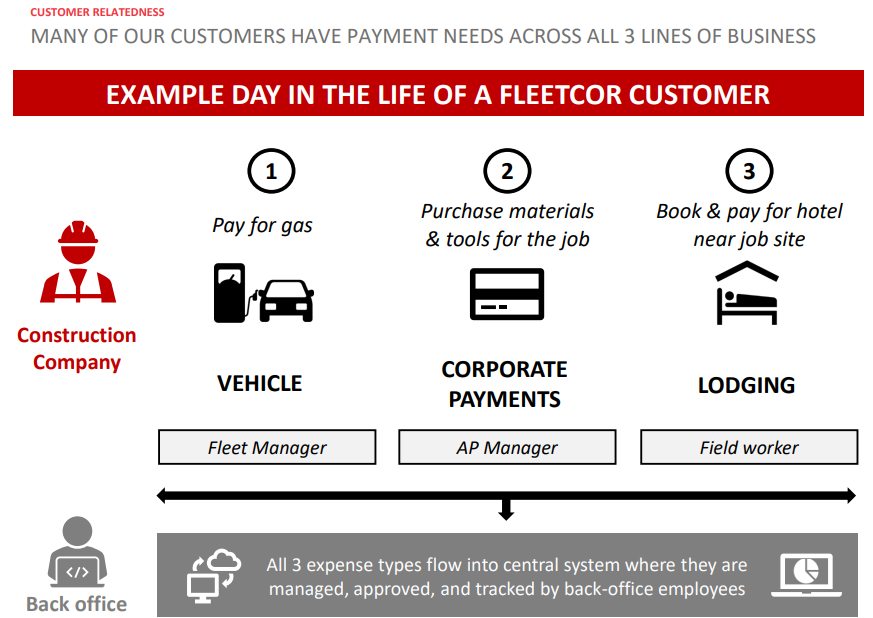

These companies offer various payment solutions to businesses. Fleetcor’s primary product throughout its history has been fuel cards, and in recent years, it has expanded to offer a more comprehensive product portfolio, including its own software for expense management. Fleetcor also went shopping in Finland when, about a year and a half ago, they acquired Plugsurfing, an EV charging service, from Fortum. Here’s a bit from the company’s own presentation about what they sell to their customers:

56% of last year’s revenue came from the USA. Other major markets, with approximately a 15% share, were Brazil and the UK. Trustpilot reviews lambast the company, but then again, the company boasts a 92% customer retention rate. Due to the limited number of Trustpilot reviews, perhaps that 92% is more indicative, although the company did go to court in recent years over some billing ambiguities, so there might be a grain of truth in the Trustpilot reviews as well.

Edenred was previously known for its Delicard corporate gift card product, but over the last decade, they have expanded in Finland to become a major player in various employee benefit implementation solutions. To my understanding, the company also has similar services globally to Fleetcor. I have only superficially reviewed their financial reports, but based on that, the figures are very similar to Fleetcor’s.

This is a brief introduction to the thread. Hopefully, it will spark discussion.

EDIT: I changed the chart’s operating profit to reflect EBT, as I believe it gives a better picture of the company’s profitability than EBIT.