Create a separate thread for FAANGs. FAANGs are the stars of the bull market: Facebook, Amazon, Apple, Netflix, Alphabet (Google’s parent company, if anyone hasn’t noticed yet).

There’s already a thread for Facebook here, but one hasn’t been opened for the others yet.

FAANGs evoke admiration in some investors and rage in others: they are disrupting an increasing number of other industries (commerce and media being the foremost), and their grip on consumers is completely unprecedented. In addition, they are constantly strengthening their positions by buying out young competitors with their hefty cash reserves or literally driving dinosaur competitors into the ground.

An interesting aspect of several of these companies is their ability to nimbly spread into new areas (e.g., banks’ territory), which increases market potential. Furthermore, they have remained in excellent shape and have been able to build parallel platforms alongside old ones (case QQ and WeChat, etc.), thus staying afloat in a changing world, which is often a challenge for large companies. As one commentator noted, these companies are “structured” as moonshot launchpads.

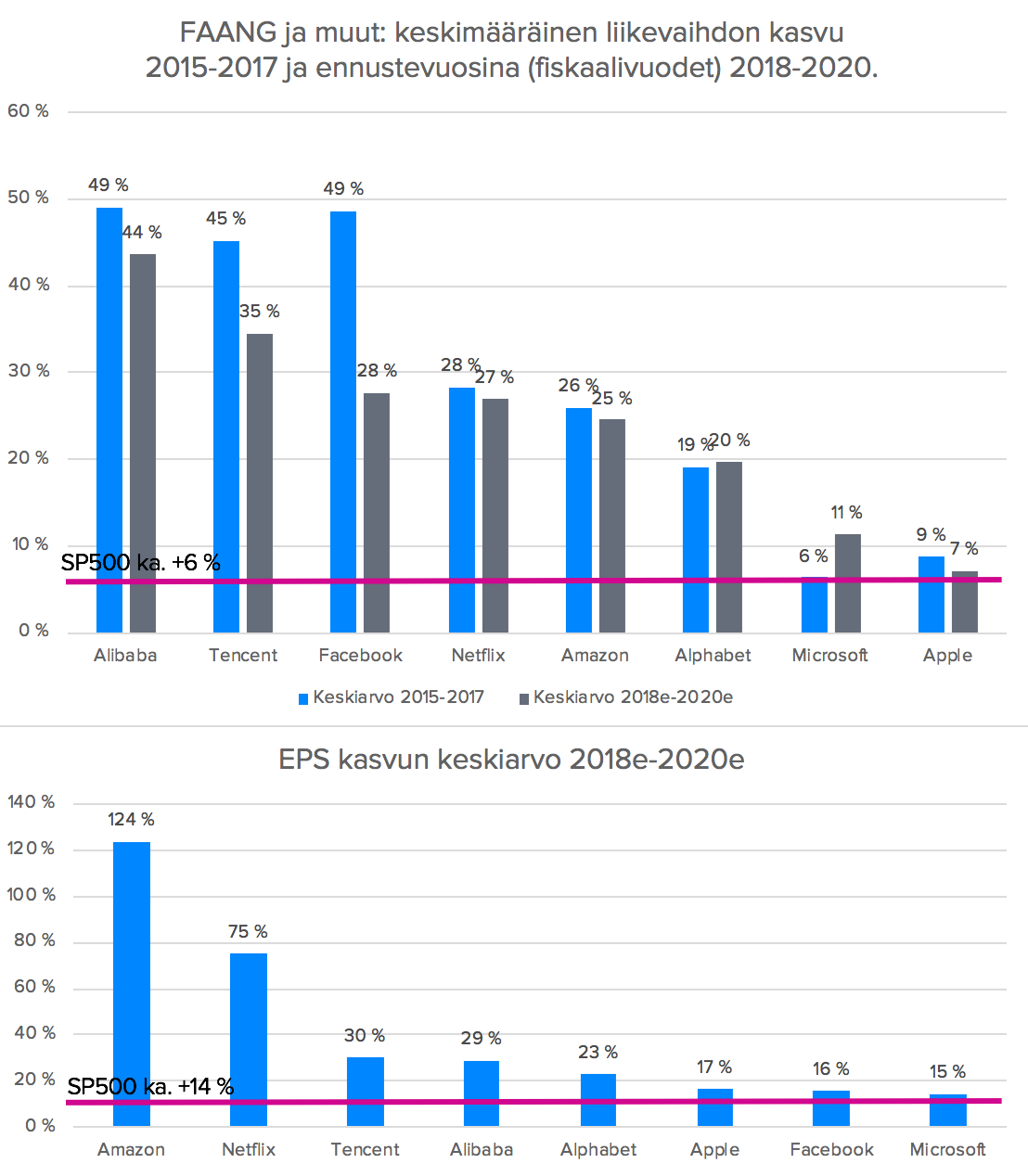

To provide some substance to the opening, I created a simple chart showing the average revenue growth of FAANGs from 2015-2017 and for the forecast years (source: Capitaliq) 2018e-2020e, as well as the average EPS growth for the same period. In addition, I included Microsoft, a trusted friend of all office workers, and a couple of Chinese internet giants, Alibaba and Tencent, for comparison. The red line from Inderes marks the average revenue and EPS growth of the SP500 index during the same period.

Their growth and growth prospects are almost entirely in a different league compared to “average companies,” but a lot of good has also been baked into the prices: P/E ratios are moving around 23-35x for the coming years.

Some believe these are a full bubble, while others think it’s a must to be on board with them. Regardless of your opinion on these as investments, it’s worth following these companies and their movements. Do you have FAANGs in your portfolio? Does this group of companies spark any thoughts?

Psst! This is not an analysis or investment recommendation ![]()