Rauli has prepared a comprehensive report on Luotea, which, like other extensive reports, is reliable for everyone. ![]()

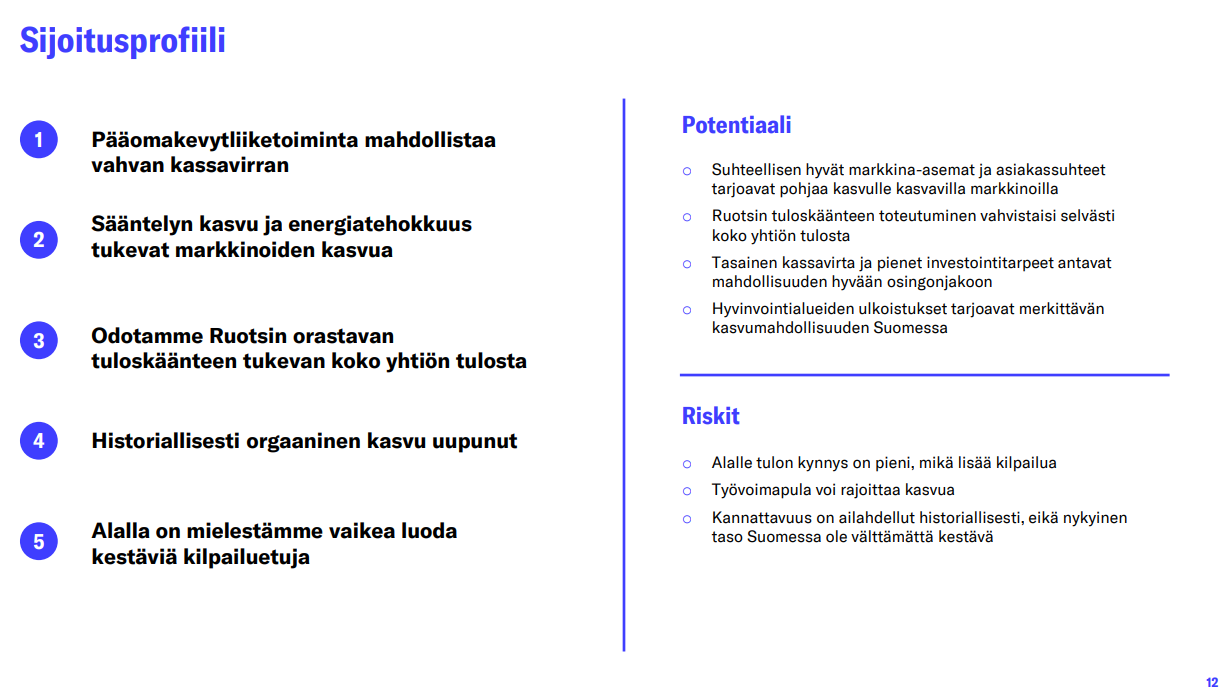

We expect Luotea to continue its clear trend of improving results in 2026-27, with Swedish losses turning into profits. We estimate the company will generate strong cash flow, which we believe alone provides a sufficient return expectation for investors. We reiterate our “add” recommendation and a target price of 2.6 euros.

Quoted from the report:

Strong cash flow profile

Luotea’s business is asset-light, and thus it should inherently generate good cash flow, naturally depending on the level of profit. Luotea’s reported depreciation level in 2026 will include approximately EUR 1.5 million in acquisition cost depreciation, which does not impact cash flow. We have removed this from our adjusted figures. We estimate that the depreciation of the company’s fixed assets will be slightly higher than investments in the coming years. The company’s net working capital is negative, which means that growth should inherently release capital and support cash flow. However, we do not expect significant growth or the release of net working capital in the coming years. Due to the above factors, the company should structurally generate more cash flow than reported profit. Our forecasts for the coming years are consistent with this, with free cash flow exceeding our net profit estimates.