It’s easy to be wise in hindsight, and Kojamo’s offering would have been a treat to participate in. What’s not to like about riding along with the trade union movement and already enjoying nice returns? Housing policy favoring rental housing in large cities is only getting stronger, going completely against the main trend of housing finance, with Kojamo being one of the biggest beneficiaries. By the way, they made a fun recruitment when Olli Turunen from “Buy, Rent, Prosper” moved to head the investment unit.

1 Like

Kojamo pays its taxes in the exact same way as other companies.

I guess every listed company has shareholders who don’t pay taxes on their dividends.

By the way, do pension insurers Varma and Ilmarinen pay taxes? Pension foundations are at least exempt.

3 Likes

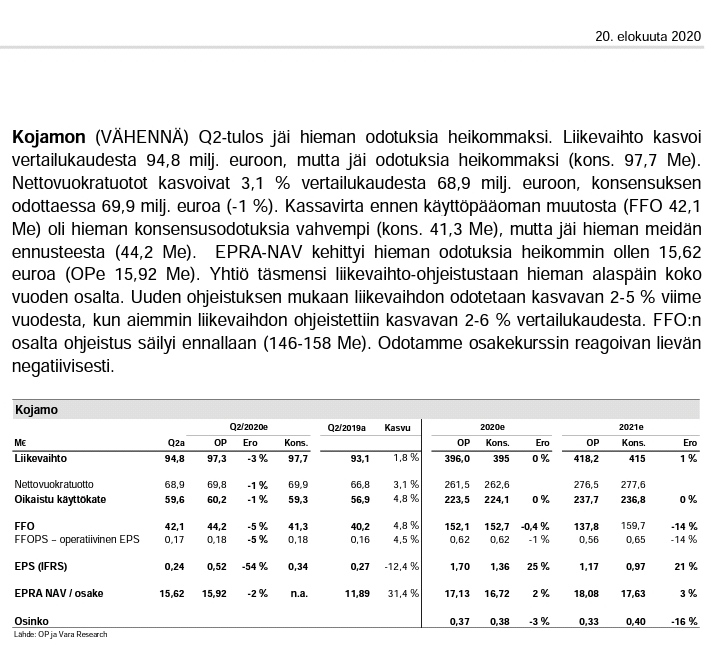

According to the earnings release, the pandemic has had little impact on operations:

- profit grew by approximately 5% and revenue by approximately 2%

- earnings per share decreased slightly (0.27 → 0.24)

- revenue is expected to grow by 2-5% for the full year

My guess for reactions: It won’t skyrocket but will rise slightly

4 Likes

OP’s morning review:

Revenue growth expectations were dropped by one percentage point in a year that included a corona quarter, and most companies still haven’t provided any guidance. I’ll forgive this

It’s just a defensive and somewhat predictable case. Moving on!

Addition: Earnings commentary à la Markku Moilanen (OP)

What if the stock drops? I don’t get it, one wouldn’t think this would be a stock where day traders would be very active for quick profits? Have expectations gone completely out of hand due to the V-curve rise?

It could be that my still limited understanding is restricting me here. Yes, earnings per share dropped slightly but still.

In general (without knowing Kojamo in depth), in this interim report season, falling short of expectations has been reacted to very negatively, and conversely, exceeding earnings has been reacted to somewhat lukewarmly.

Today, I took my first small opening position in Kojamo precisely for this reason. I believe that dips caused by large block trades (cf. yesterday’s Kamux) are good buying opportunities, as the price usually drops quite significantly. In my opinion, there’s usually no good reason for the dip, as it’s only natural that when a large block is bought, you get a discount, which in this case, compared to the last 50-day price, is about -7-8%. At the same time, it’s good to note that the stock has only traded at a higher price than that in the last two months, meaning the transaction price is actually, in my opinion, surprisingly high.

5 Likes

Varma and Ilmarinen have both been selling. Apparently, it was a block trade, but no flags have appeared yet. I haven’t seen any better reasons for the sales or much other information about the trades anywhere.

Does @Jesse_Kinnunen still read these forums and follow the real estate sector in his new job or in his free time? Are there any educated guesses as to what’s happening? Is it possible that foreigners are behind the purchases? Anyone?

Addition: ![]() Embarrassing to read OP’s morning review in the evening and realize that the answer would have been found there even before the stock exchange opened

Embarrassing to read OP’s morning review in the evening and realize that the answer would have been found there even before the stock exchange opened ![]()

1 Like

According to that article, precisely so. Quote: “We have just spent a couple of days on the phone with European investors. Based on the discussions, investors greatly appreciate our ability to invest in new housing, but they also like the Finnish operating environment that creates new supply,” Nieminen marketed.

3 Likes

Do trade unions and Finnish pension companies have so-called better information about the role of housing benefits in future adjustment measures?

In my opinion, it’s only natural that the course dips a bit when those with the best market information are selling heavily abroad.

It probably has too much weight in many stock portfolios from a risk management perspective.

1 Like

When thinking about Kojamo’s return expectations, it still doesn’t look very good from these levels. The dividend yield is still below 2%. Considering how many really high-quality US REIT firms have been beaten down, Kojamo enjoys quite a high valuation in the current market. Is this valuation then based on domestic housing subsidies, and through that, the company is allowed a dividend yield comparable to bonds?

1 Like

The drop continues. As a novice, I somehow thought that if foreign investment companies put money into this when the main owner is selling, it’s not a completely doomed stock, and I even added more at 19.2. But my stop/losses are starting to hit, my first purchases happened right at the highs. “Buy into rising prices”. Damn it.

I wouldn’t throw in the towel just yet; technically, it looks like a turnaround could be coming soon. The MA200 level will be met just above €18, and the stock is already significantly oversold. I, for one, will be looking for buying opportunities soon.

7 Likes

At current multiples, the dividend would have to rise above 4% before I would even consider buying. I’d gladly profit from the greed of the trade union movement myself, but Kojamo’s distributed dividend is a complete joke.

2 Likes

It depends. It’s not a joke if the profit is used for investments.

By this logic, quite a few listed companies’ dividends are a complete joke.

I personally had Kojamo for a long time, e.g., through the February dip. I sold them at the beginning of September for 20.10, with a 20-30% profit, when it looked like it would stay there or start to decline.

I might buy them back at some price, but probably not yet at 18. The upside is so limited. I don’t see it as a stock permanently over 20. It’s difficult to improve returns when the supply of new rental apartments in Kojamo’s area has increased, and on the other hand, tenants’ ability to pay has hardly increased. From the state’s perspective, there will probably sooner or later be pressure to start curbing the growth of housing benefit expenses, or at least there should be. On the other hand, the share of rental housing in cities has become more common in recent years.

Now, I’m going by gut feeling a bit. The current price is pretty precisely 1.2x NAV, which is quite in line with foreign peers. In my opinion, 18-19 euros is the “fair price” for this stock. The expected return is, in my opinion, lower than the rest of the market, and justifiably so, because future returns are easier to predict.