The shareholder meeting was in the morning; a quick glance shows that losses continue, though some costs have been reined in. Is the cash seriously running out this winter, when I add up the losses and cash reserves?

Google translate:

July-September 2022

Net sales decreased by -7.2 percent to 55,991 thousand SEK (60,346). Net sales have been negatively impacted by the recall of Häagen-Dazs products due to defective items during the summer.

As a result of continuously increased product and delivery costs and currency changes, the gross margin deteriorated to 33.1 percent (35.1) compared to the third quarter of 2021.

Sales of own ice cream brands decreased by -7.0 percent. The decrease is partly due to price increases in Swedish grocery retail, which affect sales to consumers, but also to reduced deliveries to Finland during the quarter.

With the decided savings program, other external costs decreased by 17.7 percent to 16,510 thousand SEK (20,062), and personnel costs decreased by 35.0 percent to 8,052 thousand SEK (12,383).

Earnings before interest, taxes, depreciation, and amortization (EBITDA) were -4,355 thousand SEK (-9,236).

Operating profit was -6,570 thousand SEK (-11,856).

Profit for the period after tax was -6,066 thousand SEK (-9,801).

Earnings per share were -0.27 SEK (-0.66).

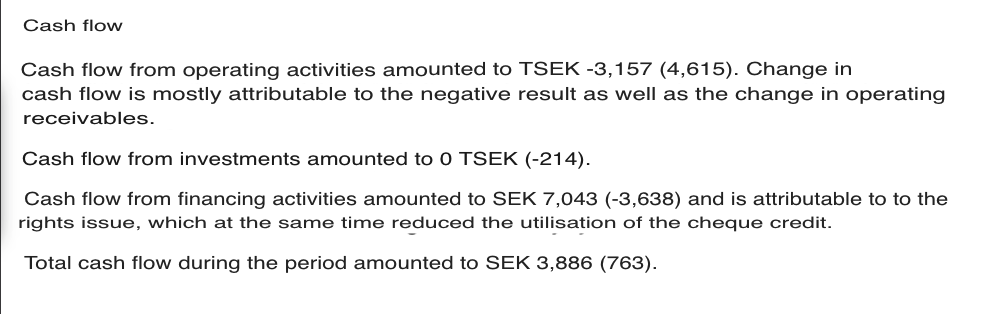

Cash flow for the period was -3,395 thousand SEK (-1,682).

January-September 2022

Net sales decreased by -5.4 percent to 181,778 thousand SEK (192,168). The change, adjusted for the terminated Nick’s agreement, is -0.4 percent.

The gross margin somewhat deteriorated due to increased raw material costs compared to January-September 2021 and was 32.8 percent (33.8). However, compared to the full year 2021, it was an improvement of 2.7 percentage points from 30.1 percent.

Growth of Lohilo’s own ice cream brands was 2.2 percent.

Earnings before interest, taxes, depreciation, and amortization (EBITDA) were -5,487 thousand SEK (-24,696).

Operating profit was -12,140 thousand SEK (-31,175).

Profit after tax was -12,007 thousand SEK (-25,565).

Earnings per share were -0.63 SEK (-1.71).

Items affecting comparability during the period were 6,250 thousand SEK. This item relates to the settlement with Nick’s and is recognized in other income. Compensation was paid at the end of March.

Profit before tax, adjusted for items affecting comparability, was -20,353 thousand SEK (-24,696).

Cash flow for the period was -142 thousand SEK (-2,627).

Cash and cash equivalents, including granted credit facilities, amounted to 5,904 thousand SEK (11,764) on the balance sheet date.

Significant events in the third quarter of 2022

During the period, costs increased due to higher raw material and delivery costs, as well as the development of the SEK against the EUR and USD.

In July, the company carried out price adjustments for most products, which continued in August and is expected to have a positive impact on product margins.

Lohilo appoints Daniel Broman as the new CFO starting January 1, 2023.

The company will not renew its distribution agreement with General Mills. The agreement expires on December 31, 2022.

Dutch listings for 2022 have increased from 600 stores to 830 stores in the Albert Heijn grocery chain.

Lohilo entered into a sales and distribution collaboration with Sproud International.

Events after the balance sheet date

The distribution and collaboration agreement with Fuud AB ends in mid-October after the FUUD group declared bankruptcy. The bankruptcy does not significantly impact Lohilo’s sales as the business has not had time to build up. The maximum customer loss risk is 230,000 SEK.

Lohilo shifts its focus to its own products. During the fourth quarter, management will launch a restructuring program with additional costs to adapt the company to this.

Improved results and bright spots in export markets

The quarter has presented challenges related to accelerating inflation, but also bright spots as we see that the changes we have implemented in the company have already had an effect and we are on the right track.

Thanks to the efficiency measures implemented in both our distribution and organization, we succeeded in reducing external costs by 18 percent and personnel costs by 35 percent during the period. We have not only reduced costs but also adapted to how we want and should operate in the future, which means we have high hopes of seeing further positive effects from the implemented savings. In addition, we have taken further measures in the last quarter to further reduce our costs.

To streamline and improve our distribution, we have also closed several warehouses. In addition to a large reduction in inventory, which lowers our costs, this change also means that we tie up less capital, especially in inventory.

Improved results

The economic downturn and increased energy and interest costs have affected consumer behavior in our grocery stores and the demand for premium products, such as LOHILO ice cream. In addition, rising global raw material prices and the weakening of the SEK lead to increased costs for products and transportation. Rising energy prices also increase our production, warehousing, and distribution costs. This means that we do not quite achieve a positive result during the quarter, although we are pleased that we are moving in the right direction and it is clear that we are significantly improving the result in the third quarter.

Focus on own brands

Following the end of collaborations with General Mills and FUUD, management and the board have assessed that in the future, we should focus more on our own products to increase margins and grow the company’s value.

The growth of our own ice cream brands in the first nine months of the year is 2.2 percent. The weaker development in the third quarter is due to the aforementioned factors: sharply increased prices in Swedish grocery retail combined with consumer uncertainty about high inflation, increased interest rates, and electricity prices.

However, in September and October, we can see the positive effect on margins of the price increases we implemented with customers. Like other consumer markets, we will implement additional price increases at the turn of the year to strengthen the margins of our own brands going forward.

New products

In September, we made the last major launch of a new ice cream product, LOHILO Everyday Slacker. The ice cream and its associated concept are specifically designed to clarify the greatness of our core product: a healthier version of your favorite ice cream. Resembling another worldwide favorite with peanuts and chocolate, the ice cream has received a warm welcome in the market and has already been launched in several markets outside Sweden.

Another exciting piece of news is that through robust product development, we have now also been able to open up an entirely new sales channel for a completely new target group by launching a protein-rich ice cream that meets the dietary needs of patients and those receiving treatment. The development of this LOHILO ice cream has taken place in collaboration with one of Sweden’s regions, where nutritionists have evaluated the nutritional value and ingredients, as well as the taste, of the ice cream.

Exports continue to grow

The success in the Netherlands has also not been long in coming. After five months in the Dutch market, we have already been able to increase the sales of our products from 600 stores to 830 stores in the leading grocery chain Albert Heijn.

Preparations for the launch of LOHILO ice cream in Norway and Denmark have progressed well and are expected to take place in 2023. In addition, negotiations are underway with a new partner in China for licensing the production of LOHILO ice cream for this market.

Financing and liquidityImplemented changes through cost savings, organizational and distribution efficiencies, and price increases have resulted in a positive cash flow impact. The termination of the distribution agreement with General Mills still means a loss of volume, which will be reflected in our sales in 2023. To adapt the business, management is now implementing additional measures during the fourth quarter of 2022 and the first quarter of 2023. These measures are expected to have full effect in a short time regarding both cost levels and working capital. The Board continues to work actively on the Group’s financial matters.

Looking Ahead

The past year has been one of great change and many challenges, both external and internal. I am convinced that the entire organization will emerge from this period of change with a stronger focus and great joy, so that we can continue to offer Lohilo’s excellent products to more consumers in Sweden and many other countries.

I am proud of my colleagues and our products, which are increasingly valued both in Sweden and in our export markets. I look forward to the future and the trends with which we work closely and which we do not believe will be significantly affected despite the state of the economy.