Finda sold its DNA ownership and now has about 1 billion in cash for investments around the globe. The Aurejärvi brothers are scheming. Dividend of 8% tax-efficiently. Berkshire Hathaway’s footsteps would be quite yes to implement ![]() Let’s see in 20 years.

Let’s see in 20 years.

I was just looking at G. W. Sohlberg (GWS) on Privanet.

The company has transformed into an investment company. The latest quarterly report provides the following information:

- The company has generated a loss of approximately 10% since October 2018.

- There is some information on the distribution of holdings by asset class, but not on specific investment targets.

- Under “Private markets” there are some figures, but no specific targets.

In addition, I have been reading financial statements and other information published by the company. Observations:

- A small investor cannot know what the company has in its portfolio.

- A small investor cannot know what the cost of these holdings is.

Furthermore, when I asked directly what was in the portfolio, no information was provided.

The company can be acquired on Privanet at 75% of the portfolio’s market value, but a small investor does not know if some asset management firm is draining the company with overpriced funds or other instruments. This lack of transparency is certainly poison in such a case, and I greatly wonder why anyone offers so much for this firm. I might buy this lottery ticket for perhaps 40% of the market value, but then again, I could just go play the lottery at the local R-kioski (convenience store).

So I ask: what have I, the undersigned, failed to read or notice? Why is someone willing to pay so much? You only get about 5% in dividend yield from this. The same return can also be achieved with stocks whose business operations provide much more information.

4 Likes

Let me put this here - I just came across it myself.

I don’t know anything about the industry, and the stated “expected return” doesn’t necessarily match mine, given that it’s an unlisted company. What do you all think? (On the other hand, at least they’re not boasting utopian numbers)

My understanding of agriculture is that all you’re left with is ![]() and baling twine

and baling twine ![]()

1 Like

New on Invesdor: Solar Water Solutions

“Solar Water Solutions purifies water with solar power. Affordable water can revolutionize life and economic development in developing countries and wherever water is scarce. Today, over 10,000 people around the world enjoy water purified by SWS.”

The minimum investment of 250k was filled in a couple of days, the maximum for the offering is 1.2 million.

3 Likes

Nasdaq to Launch New Marketplace for Unlisted Securities:

5 Likes

Once again, frozen growth estimates have been thrown around, as always in these unlisted prospectuses. There’s no responsibility whatsoever for whether we even get close.

1 Like

Injeq announced that 90% of the required number of patients have been tested in clinical trials, and 100% will be reached in August, followed by a 1-month follow-up period, etc. Two patents were granted in the US and something in Europe at the end of June.

Maybe Injeq can achieve something, it kind of looks like it. But it will still take time. I assume that if they get CE markings and other things sorted, there will probably be a funding round for scaling production at some point?

I once invested a few thousand in Injeq shares through Invesdor. It’s a long wait.

4 Likes

Invesdor now has a new kind of offering: Naava’s convertible bond with an 8% interest rate.

Have you come across or invested in these before?

I’ve stumbled upon Invesdor a couple of times, and I’m always surprised by the information provided about companies. Almost all the information is vague marketing talk. Is it possible to get concrete financial data and key figures for Naava, for example?

Of course, I understand it from the platform’s side; it’s easier for someone to fall for giving money based on marketing pitches.

The new pitch does contain the financial data. However, the forecasts are often overly optimistic.

I have invested in several business loans through Fundu and Fellow Finance. In my opinion, there’s no point in investing too much in one loan, as it’s easy to invest in multiple loans.

Could I get some opinions and educated guesses on this case? Springvest is pushing Medixine, which sells a remote healthcare platform. On the surface, their business looks really interesting (remote care was growing even before COVID-19, and the pandemic is accelerating that change; the company has grown organically and is profitable; valuation is pretty good; the exit path seems logical, etc.), but why on earth is the company seeking funding from amateurs? This always raises my red flags. As someone who has worked extensively with startups, both as a founder and an investor, it seems strange that a promising company IS NOT seeking funding from health technology-specialized venture capital investors, who could help with scaling and are available in Finland and worldwide. Instead, they are seeking funding from “tracksuit investors” (retail investors) who offer nothing but money—typically in the hope of a much higher valuation, meaning investors are left with a “cash cow” role.

But is there anyone on this forum who knows about remote healthcare and could assess the need for and benefits of Medixine’s platform from the perspectives of various stakeholders (end-customer, doctor, healthcare organization, society—e.g., the upcoming Sote reform…)? I’d also be interested in the competitive landscape: are there already a ton of similar platforms, or is the market fragmented into small players, as Springvest claims?

This is the company in question: https://www.medixine.fi/

And for clarification for those unfamiliar with Springvest, it is a crowdfunding platform whose operations are heavily based on direct sales over the phone. They acquire funding for startups from small investors as an assignment. For example, Springvest called me because I own shares in a health-related listed company.

1 Like

The potential is what you pay for in Medixine. The valuation before the share issue is just over 11 million euros. But perhaps the possible increase in revenue will significantly boost earnings. According to them, they will run out of money in six months if the issue doesn’t go through (i.e., if they can’t get funding elsewhere in that case).

When adjusting equity by deducting intangible assets, equity is less than 500,000 euros. It does seem to be making a profit, and the capitalization of development expenses in 2019 at least seems to be less than depreciation, so the result appears to be on a healthy footing from this perspective, as no massive capitalizations were made during the fiscal year to push the result into positive territory.

The ratio of revenue to accounts receivable is a bit concerning. Accounts receivable are almost equal to the 2019 fiscal year’s revenue.

1 Like

Pyynikin informs me:

We are Finland’s most respected beer brand

By Pyynikin Craft Brewery Ltd

Pyynikin Craft Brewery’s popularity continues to grow. On Taloustutkimus and Markkinointi & Mainonta’s Most Respected Brands 2020 list, we clearly beat our competitors, leaving all the giant breweries behind.

Taloustutkimus Oy’s and Markkinointi & Mainonta magazine’s Brand Appreciation 2020 study investigated the appreciation of brands among Finns.

The brands studied were selected in a separate preliminary study in February–March 2020. The preliminary study identified the spontaneously best-known brands. Respondents were not given options, but were asked, “What brands, i.e., marks, product brands, or companies, come to mind from product category X?”

In the beer category of the brand study, the large domestic beer brands followed Pyynikin Craft Brewery: Sandels, Laitilan Kukko, Karhu, Olvi, Aura, Koff, Karjala, and Lapin Kulta all remained behind. Foreign competitors also ranked behind Pyynikin: A Le Coq, Carlsberg, Heineken, Saku, and Corona.

“We are grateful to Finnish consumers and our partners, especially shops and central retailers. They gave us the opportunity, consumers found us, and the result is this, Finland’s most respected beer brand,” smiles the brewery’s founder Tuomas Pere.

The popularity of the brewery’s beers and other beverages has caused challenges for production. Due to strong growth in demand, the brewery has continuously increased production capacity and staff. However, that has not been enough.

“The growth in popularity of our beers has been tremendous and has created positive problem situations for the brewery. We are sorry that our most popular products, for example, the Mosaic Lager chosen as the world’s best, have occasionally been out of stock on store shelves due to high demand,” says Pyynikin sales director Juha Leppänen.

The share of exports has been steadily increasing. The brewery is preparing to significantly increase its capacity so that there will be enough beverages for both domestic consumption and export. The brewery will also start taking restaurant customers from the beginning of next year. Negotiations on agreements will begin within this year.

“Our products are available everywhere in Finland and across Europe. With the ongoing internationalization project and the upcoming increase in production capacity, we will also be able to conquer new areas. We aim to be the world’s best-known Finnish beverage brand, and we will also open our offerings to restaurants,” summarizes community manager Veikko Sorvaniemi.

EDIT: I hope this will eventually be publicly listed, and does anyone know where I could sell my Pyynikin if I wanted to? I haven’t looked into it myself.

Edit 2: In Lidl stores internationally, at least.

7 Likes

Pyynikki shares are traded at least on Privanet https://privanet.fi/investing

3 Likes

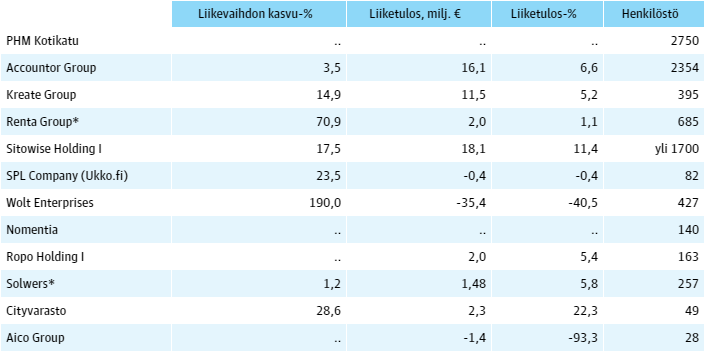

Let’s throw Solwers Oyj in here for contemplation - a news article behind a paywall, a few quotes below.

“Solwers, a company offering construction consulting and digital solutions, aiming to go public next autumn, is already diligently preparing for listing.”

“The company has been preparing for over a year now. According to Sebbas, all actions have been geared towards going public. The share issue through Invesdor over a year ago was also arranged for learning purposes.\n*”We treated the arrangement of the issue as a practice round. In addition to capital, we sought 200 new shareholders, which we got,” Sebbas says. The company raised one and a half million euros through the issue.”*

The company has prepared its financial statements according to IFRS (International Financial Reporting Standards) from the outset.

The company’s business areas are infrastructure construction, commercial construction, and digital services.

“”Our operating model is based on smaller, manageable operating environments and specialized experts. A common corporate governance then defines the limits for independence, risk management, and reporting,” Sebbas says.”

In my opinion, infrastructure construction will likely receive a boost as governments shift into recovery gear.

Disclaimer:

I am one of those 200 new shareholders ![]()

A couple of other similar risk investments have already failed, and those losses have been reported to the tax authorities ![]()

In addition to Solwers, another unlisted experiment, Yeply, seems to be progressing better than expected. Mobile bike maintenance is getting timely support from the current situation; bike sales have increased significantly, and soon they’ll need maintenance too ![]()

Let’s also add potential IPO candidates based on KL’s news, also behind a paywall.

Additionally, at least Delete Group and M-Brain have seemingly been on track for an IPO at some point. Those plans might still be waiting for improved results ![]()

4 Likes

Which broker do you use to store unlisted shares (brokered by Privanet)? Nordnet is certainly not the best choice, as in addition to Privanet’s fees (2-3%), Nordnet also charges €50 for registering a trade made through another broker and €2.50/month for custody, unless you are a member of Osakesäästäjät (Finnish Shareholders’ Association).

At Nordea (or at least a year ago), there was free custody if you traded during the previous quarter. I made some mini-purchases when the brokerage fee was percentage-based, and thus got the “custody fee” close to zero.

During the corona dip, I sold everything, as listed shares fell significantly more than Privanet’s unlisted ones.

1 Like

What bothers me more is the 50€ fee charged by Nordnet for a “trade made through another broker.” It’s not even possible to buy these through Nordnet, so it’s a “mandatory” expense here. However, as an OSKL member, storage is free for me.

At Nordea, the corresponding fee is ten euros, though it was never actually charged by Nordea.

Currently, I don’t have any unlisted shares in my portfolio, as I sold my KPYs. If/when I buy any unlisted shares next time, I definitely won’t keep them in a Nordnet portfolio for storage.

1 Like

This is good to know in advance. The plan is to transfer Solwers Oyj shares to Euroclear at the beginning of next year in preparation for listing, and a suitable custody account will be needed for that.

Both Yeply and Solwers were acquired through Invesdor. Custody is currently handled through Invesdor’s system, unless other arrangements have been made previously.