Thanks for the link ![]()

It’s nice to have a good challenger for Arvo in KPY. There are strong intentions in Kuopio to seriously expand into asset management and create growth in Finland. This is needed here, although growth, of course, does not directly equate to a good investment. The report turned out to be quite a giant, but few will likely read it all at once, so perhaps there are sections here to return to in the future. And Claude can at least efficiently read a report of this size. A small Inderes MCP advertisement is permitted here.

KPY is indeed in an interesting situation in the sense that forecasting and valuation are very difficult at the moment, and the range of outcomes is wide, even though in many ways a large part of its business is very steady.

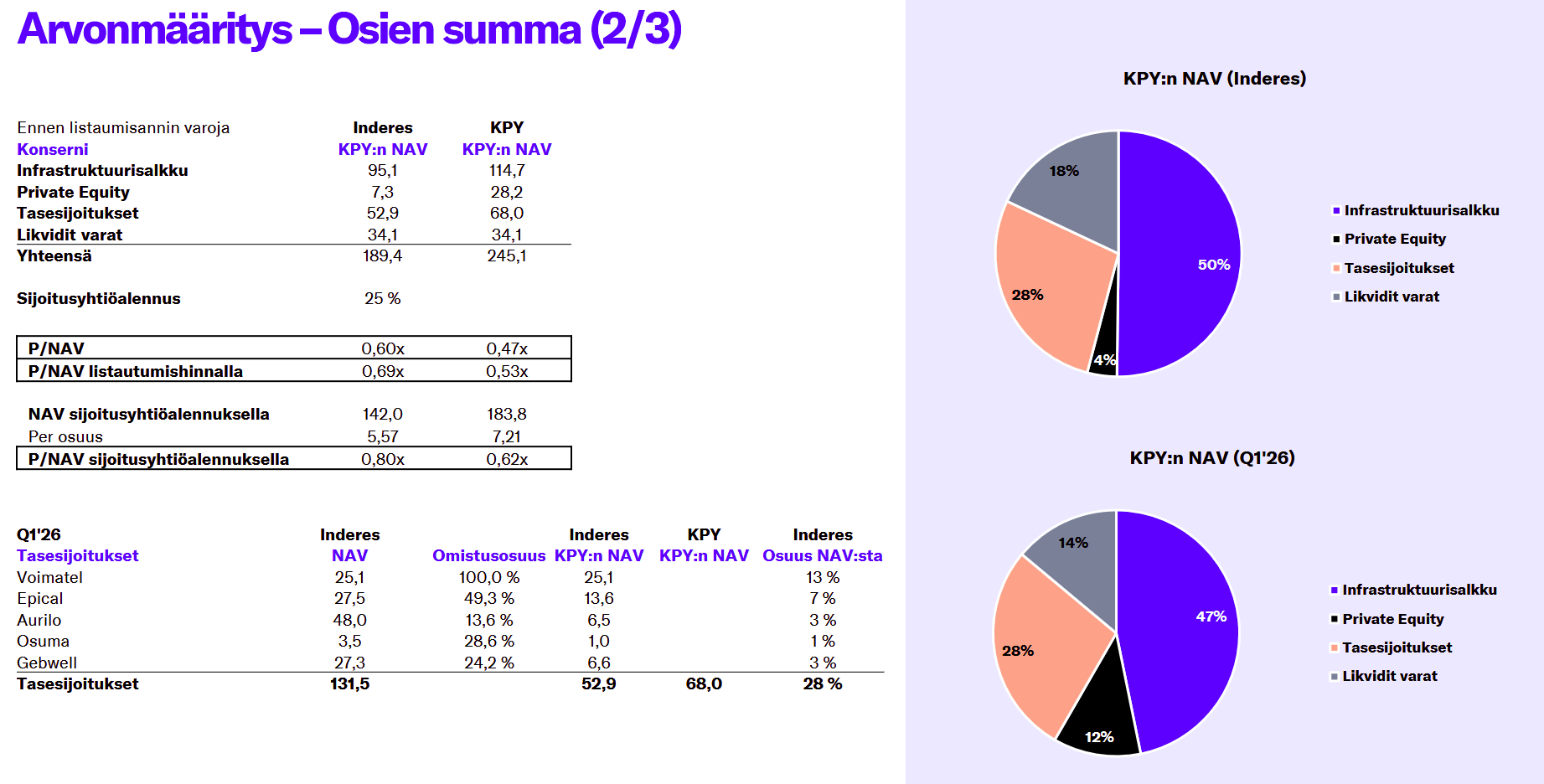

The Kuopio offices (Novapolis), which currently make up the Infrastructure portfolio, have historically performed very well (occupancy rates ~95% in the 2020s), but now public sector actors are moving away from private premises, and the market situation is generally difficult as everyone knows (occupancy rate at the end of Q1’24 was 86%). A lot depends on the development of Kuopio, as the tenant flow now relies primarily on private actors. In my assessment, rents have developed very well previously, but now the competitive situation has certainly tightened, which can be seen in Novapolis’ occupancy rates, which in turn likely requires somewhat tighter pricing. My estimate of the fair value is EUR 95 million vs. KPY’s EUR 115 million.

There is clear potential in Sentica, but the business also involves significant risk. Especially relative to the current EUR 28 million NAV valuation. I took a clearly more conservative view here, and in my own estimates, the value is EUR 7.3 million. It is easy to chart a clear increase in value here if the business progresses according to plans. Ramping up a fund business to the point where it generates steady management fee income typically also takes quite a long time.

Regarding balance sheet investments, Voimatel is a clear value driver and accounts for just under half of their value. The company’s development has been strong in recent years during the heavy investment cycle of telecom operators and fiber optics, so its valuation is not straightforward either. My own NAV estimate for the balance sheet investments is EUR 53 million vs. EUR 68 million.

Overall, KPY seems to have reached a completely different situation compared to a few years ago, as the significant holdings are doing relatively well, and Novapolis’ cash flow alone is no longer carrying the entire group. Even though it remains a very clear pillar of the earnings. The wildcard then is the fund business and the anchor investments made into these.

All in all, I believe a clear balance sheet discount is justified, but the current pricing is already so cheap (0.46x) that I started coverage with a positive recommendation to see how the fundraising succeeds and how the Kuopio office market develops. In the short term, there will likely still be selling pressure from old owners, meaning we might have to wait a moment for positive share price drivers.

We also filmed a video about KPY with @Iikka_Numminen, which will likely be released in the near future.