What thoughts do people have about fixed income investing now that general interest rates have been on quite a rise? What factors and mechanisms should be taken into account? I’m mainly thinking about Nordnet’s corporate bond funds. Surely, new loans issued will carry higher interest rates, but companies’ high debt servicing costs will also make repayment more difficult. Does anyone believe that the returns of low-cost and relatively low-risk fixed income funds could beat the indices (in Finland and/or Europe)? I’m looking forward to hearing some well-reasoned thoughts!

The return on bond funds can easily go deep into negative territory when interest rates rise, as has happened now. Bond funds perform best when interest rates fall (as they did excellently for years before interest rates turned upwards). In theory, bond funds balance the portfolio, but recently both stock markets and the value of bond funds have fallen (with bond funds, even several years of returns are in the red). So, if one now believes that interest rates will clearly start to fall, bond funds are probably a good option. I myself do not invest in (long-term) bond funds.

5 Likes

Before the zero interest rate world, I kept my cash in Seligson’s Money Market Fund, which invests in 3-month interest rates without subscription and redemption fees. Now, for the first time in a long while, I’ve done the same move, as the fund’s return has once again turned positive. This way, the value of short-term interest doesn’t fluctuate in the same way with the interest rate level as longer-term rates do. On the other hand, the return isn’t great in terms of investment, but for cash awaiting other work, it’s still better than a zero-interest bank account (unless interest rates are at zero).

4 Likes

It feels to me that currently, a bond fund that invests in debt securities with less than one year remaining until maturity and holds them until maturity would perform best. While theoretically better returns can be made by buying and selling securities back and forth, in practice, it might be the opposite.

2 Likes

That’s true, but you can probably get a decent return even if interest rates stay at their current level. According to OP (a Finnish financial services group), High Yield corporate bond ETFs, which they recommend, have a running yield of approximately 8%. And this should already provide some protection against a small further increase in interest rates.

The Great Rotation

The past year has seen a rotation from growth stocks to value stocks. As inflation has risen, interest rates have also been on a strong upward trend. The valuation of growth stocks has plummeted as higher discount rates cause a significant decrease in the present value of their future cash flows. Value stocks have performed better because they generate positive cash flow, and the highest quality companies are able to pass on cost increases in their prices.

What about interest rates? Bond markets have been in quite a turmoil this year. As a result of the broad-based rise in interest rates, fixed-income securities have lost a significant portion of their value. However, we are getting closer to the point where interest rates will no longer rise - at least not significantly. At that point, the bond markets will become an attractive market for private investors as well. When interest rates are expected to fall next year due to a recession and the FED’s pivot, significant returns will be available from bonds. Many current investors may not have experienced a time when interest rates have yielded better returns than stocks, and they may not understand how a decrease in interest rates affects bond values. I recommend that everyone familiarize themselves with the topic.

I assume that value stocks will continue to outperform growth stocks next year, although their returns are also likely to remain negative. Economic cooling, increased interest expenses for companies, and investors’ heightened risk awareness are driving stock prices down. So, is now a good time to rotate one’s portfolio towards the bond markets? Absolutely, even if the future does not follow the guidelines I have outlined above, bonds have once again become a credible investment target, offering both returns and diversification benefits.

P.S. “The Great Rotation” is a poor term in the sense that it gives the impression that money is somehow shifting from one asset class to another. This is certainly not what happens, as whenever someone sells a security, someone else buys it. Rather, one should think that one asset class becomes more popular than another, which is reflected in their valuations. Of course, you can make that rotation in your own portfolio!

7 Likes

Yes, if interest rates remain stable, investors will receive a return roughly in line with the current interest rate.

That 8% running yield indicates that these are junk bonds; normal, healthy companies don’t pay such high interest rates on their loans. These bonds carry higher than usual risks, especially if interest rates rise, it’s possible that such companies won’t be able to fully repay their loans. That’s why the yield is so high - there’s no such thing as a free lunch. (In terms of risk, high yields are somewhere between bonds and stocks.)

4 Likes

Through my own studies (of the basics, e.g., https://www.porssisaatio.fi/wp-content/uploads/2011/12/korko_opas_2018_www.porssisaatio.fi_.pdf) and even after discussing it with my bank’s wealth manager, I just can’t seem to get a handle on these interest rate markets.

My capacity is sufficient to understand, when explained in simple terms, how the value of a single bond fluctuates according to the interest rate level, but I can’t get past that to grasp the dynamics of the whole.

So, I’m wondering. And asking.

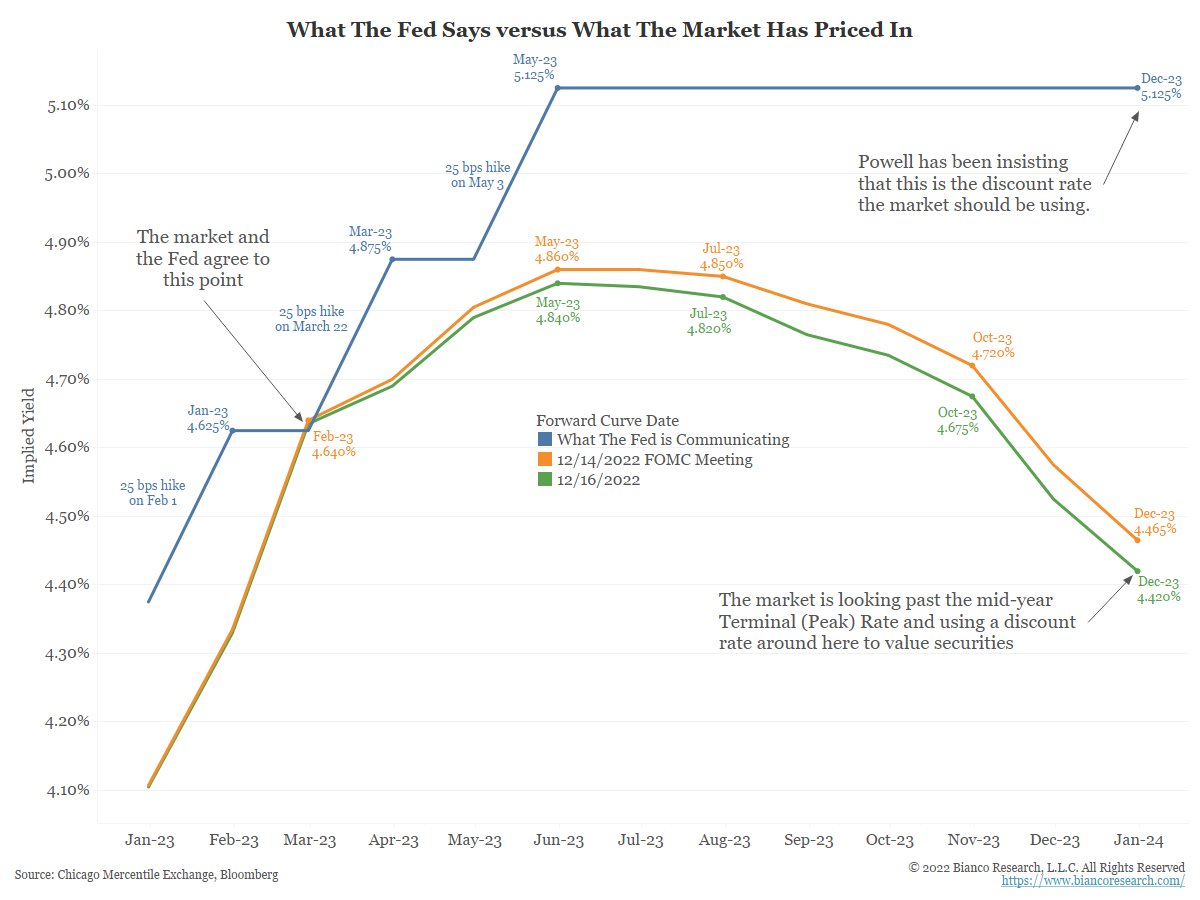

Firstly: Isn’t that a fairly clear estimate of when the interest rate peak will be reached:

Are we now waiting until next summer and then putting our bets on bond funds? It feels too easy? There are no free lunches, so what’s the catch here? If the stock market looks 6-x months ahead, doesn’t the bond market also price that in beforehand?

Secondly:

I asked my wealth manager about the scenario outlined by @kapteeni_indeksi, as I’ve been pondering the same. Anticipating a situation where the economy and stocks stall, but as rates drop, one gets returns relatively safely from fixed income, including the option to jump into stocks if a big drop still occurs. As an alternative to sitting on the rest of the cash (approx. 30% of the portfolio) and, at worst, realizing both trains have left the station while inflation has kicked in on top of it. (The goal is primarily to reach 100% stock weighting, but not at any cost.)

The core of the advice was (if I understood correctly) that because bonds issued during low interest rates have a low nominal rate, those issued from here on out will automatically be more profitable in the future because they will have a higher nominal rate. Maybe I didn’t know how to ask correctly. As a solution for “intermediate parking,” he recommended a savings account (Nordea’s flexible deposit account).

And thirdly:

TINA was last year’s word, but has it already melted away, or have stock prices only just begun to price in the flow of money into fixed income? In other words, is it actually still ahead of us? Cf. the first point. I couldn’t find (from free sources) a graph showing the movement of money into fixed income investments.

5 Likes

Today’s Kauppalehti had some interesting information about short-term bond funds. As interest rates have risen, I have been quite skeptical about investing, but it is undeniable that in short-term bond funds, investments roll over quickly and assets can be reinvested swiftly.

1 Like

I don’t like bond funds at all, but I do like fixed-income investing.

The basic idea of fixed-income investing is that (ignoring credit risk), once you have made the investment, you know the cash flow exactly and it does not change. For example, if you provide a bullet loan of 1,000 euros at a 5% annual interest rate for one year, you are without that thousand for the year, but at the end of the year, 1,050 euros appears for you. The only thing that can change this is the counterparty’s insolvency or unwillingness to pay.

A bond fund lacks this feature. You can put those 1,000 euros into a fund, but you cannot predict what you will have in a year, even in a situation where the fund’s counterparties pay their debts punctually.

I experienced this myself a year ago. I bought an apartment in an RS project (RS-kohde) in the summer of 2021, and while waiting for completion, I wanted to put the money I had earmarked for it somewhere other than a zero-interest bank account. Inflation had already risen by then. I then looked for a couple of bond funds that had a good interest rate level. In the spring, when I liquidated these investments to cover the apartment payments, they had lost value significantly, and I had to finance this loss in another way.

In direct fixed-income investing, the general interest rate level is an opportunity cost (what you would have received if you had invested differently) and it does not affect the investment’s cash flow in any way unless the investor sells their investment on the secondary market before its maturity, or the rise in interest rates causes counterparty insolvency.

The biggest problem with bond funds is that their investments are valued at market price daily (which, of course, is necessary so that the fund can be open every day for redemptions and subscriptions without restrictions). In this case, changes in the general interest rate level dominate (inversely) the value of the investment, and the actual interest yield is only visible if the general interest rate level remains stable.

The idea of fixed-income investing would be better matched by a fund where each subscription date had a locked-in cash flow, which would only be deviated from if the fixed-income securities earmarked for the subscription date’s funds encountered credit losses. Possibly, early redemption of units from a certain subscription date could be allowed, which would, of course, happen at the market price of the underlying securities. I don’t know of any such fund that is within the reach of a retail investor.

Actually, the only advantage you get with current types of bond funds is tax efficiency, as the tax authorities cannot tax the interest before redemption (in the case of accumulation units).

Direct fixed-income investments are surprisingly difficult to make as a retail investor. Primarily, bank deposits and peer-to-peer loans are available. I use both of these for my fixed-income investments. Unfortunately, I also have some bond funds, as I haven’t found suitable direct fixed-income instruments in those specific markets.

(My investment portfolio also has a large equity component, of course, but that is a topic for a different thread.)

Edit. Of course, early repayments and changes to payment plans must also be considered, but if they are counted under credit risk, what was said above still holds true.

17 Likes

Bond markets are generally more efficient than stock markets. There are no free lunches there, either. Market prices reflect current market expectations for the future. If the future then aligns more closely with your expectations than the market’s, you have the opportunity for a better return than the current expected return, net of costs.

Investing in US 20y+ government bonds at a time like this is quite risky. Few can predict interest rate and currency movements even in the near future, let alone over a 20-year period. A 20-year bond moves roughly 20% when the interest rate level moves by one percent. It is true that the 20-year expected return moves quite slowly compared to shorter-term rates, but there is quite a bit of leverage in such long bonds. Add currency risk on top of that.

For example, the ETF found under the ticker TLT is suitable as part of a diversified portfolio with an extremely long horizon, but also for speculative trading. However, I wouldn’t start investing in it instinctively without a plan and a truly well-founded view.

2 Likes

I would like to invest an elderly relative’s money for a maximum of 2 years in euros, along the lines of an Italian government bond.

Is there a fixed-income product/fund that does not reinvest, but instead allows locking in the interest yield for the next two years at the current level?

The amount would be approximately 50k–100k; they want to invest short-term while waiting for a pipe renovation, without the risk of principal loss—meaning only interest rate risk. Do such products even exist for retail investors? ![]()

You are taking quite a big risk if you start investing money that will be needed in 2 years into bond funds—and especially someone else’s money. I don’t understand much about bond markets myself, as apparently neither do you. I wonder if there even is any bond fund with capital protection.

Wouldn’t a 2-year fixed-term deposit at a bank be the safest, now that you can actually get some interest? One option is to ask banks/brokerages about corporate bonds (Investment grade level) where 50-100k is enough and which mature within 2 years. You can get a good return on them if you can get them well below the nominal price + interest on top. The risk is the company going bankrupt or undergoing restructuring. But you’d think that, for example, Finnair or Citycon or some other more stable Finnish outfit won’t collapse in the next two years…

All investments always carry risk—some greater, some smaller. In fixed-income investments, the borrower may encounter varying degrees of payment difficulties. Fixed-term deposits are likely the only ones that have a state guarantee in case of insolvency. Capital-protected fixed-income investments are indeed available, but their subscription price tends to be higher than the principal, meaning the protection doesn’t cover the entire investment.

I have also been looking for target-maturity funds, but they don’t seem to be on offer. Corporate bonds with various maturities are available on the exchange. From those, you can select options that suit your own risk and return requirement levels.

Strange comment. I want to find a product that has about 2 years of maturity remaining (plenty of such bonds have been sold on the market).

The issuer must be Italy or a larger Eurozone country.

By holding such a product until maturity, the only way to lose is if the country becomes insolvent, or relatively if interest rates rise sharply.

In absolute terms (if sovereign risk doesn’t materialize), this will yield more than a bank account over these two years; of course, a sharp rise in interest rates would provide a better return by waiting in cash.

It might be that such products are not available to retail investors with reasonable costs. A bond fund is a completely different thing, and its nominal value can drop close to zero if we get hyperinflation. But that’s not what I asked.

1 Like

In my opinion, the right place for this cash is a money market fund.

Into a bank deposit account. For example, at Aktia with a 2.75% interest rate.

[Bonds - Nasdaq (nasdaqomxnordic.com)]https://www.nasdaqomxnordic.com/bonds/bonds_mainpage/)

1 Like

Does anyone have experience with these kinds of “capital-protected” products?

These have started popping up at least from OP, and they are marketing them effectively.

Let’s share this message here as well: Finanssisektori sijoituskohteena - #308 käyttäjältä Sauli_Vilen - Osakkeet - Inderes forum

So, an interest rate podcast is coming next week, send in your topics! ![]()

19 Likes