If I can’t find anything to buy, I keep my cash in Evli Likvidi. I have Nordnet’s trading credit in reserve, so there’s no issue with not being able to buy something immediately. I buy on credit and settle it by selling the liquid fund.

4 Likes

Somewhere in this thread, there’s that chart comparing short-term bond funds to a money market fund. In a Covid-style shock (I don’t remember 100% if it was specifically about Covid), everything went down and these funds also dropped more than the money market fund. That’s worth keeping in mind.

I personally have a small slice in a savings account and the rest of the cash in Evli Likvidi B. I think the idea originally came from this thread or from Verner.

2 Likes

It’s easy to do with Morningstar’s comparison tool

Curiously, it doesn’t show names but rather the funds by ISIN code

red Seligson & Co Money Market Fund (Rahamarkkinarahasto)

blue Evli Likvidi B

I’ve combed through quite a few short-term bond funds and, to my eye, Evli Likvidi B is a good fund, but it’s not absolutely risk-free regarding price fluctuations. If you want to avoid that, then use a savings account.

6 Likes

I’ll add that if some people don’t have a credit facility (which is indeed handy) in use, based on my own experience, with Fidelity Euro Cash on Nordnet, you can always get the money into your account on the same evening if the order is placed by the cut-off. This fund does distribute income units, and the value dips slightly when they detach, but the dividend follows. Evli’s own target for Likvidi is about a 2.5% return for this year according to the monthly report. You can already get slightly more from a savings account risk-free, and when you use AI to compare how much withholding tax on interest income eats into the return vs. a fund, it doesn’t really seem to matter much in these low-yield investments.

Edit: It seems the number of banks offering better interest rates has decreased towards the end of the year, but they still exist.

1 Like

I happened to come across this sale of Elisa’s bond and started wondering where one could normally buy such corporate bonds directly. At the moment, I don’t have any intention of putting money into them yet, but it would be nice to be able to browse what kind of bonds are on the market, especially from Finnish companies.

1 Like

They cannot be bought directly. You need a broker, i.e., through a bank or an asset manager.

1 Like

That product has nothing to do with a bond, let alone Elisa Oyj as the issuer (meaning its risk does not match Elisa’s credit risk). That is a structured product issued by Barclays that Alexandria is marketing. Based on a quick look, it’s some kind of autocall structure.

6 Likes

Exactly. Thanks for the correction! At a quick glance, I thought the purpose of that was to raise capital for Elisa.

1 Like

Short-term bond funds can involve credit risk, which means they may react somewhat in situations like the COVID-19 pandemic. If you look at Evli Likvidi B, for example, it includes Teollisuuden Voima, Tornator, Elenia Finance, etc. There is credit risk associated with these, even though the maturity is indeed very short.

The lowest-risk short-term interest rate would perhaps be something tied to overnight rates; for example, there is an ETF Solactive €STR +8.5 Daily Total Return Index that pays the Eurozone overnight rate. Even then, the ETF itself likely carries some sort of risk related to its structure.

In my opinion, bank deposits are often also a competitive option for small investors. There is no credit risk for amounts under €100k, and by shopping around, you can get quite competitive rates. For example, Svea seems to have a 3-month fixed-term deposit at 2.3%. That’s quite good, considering the 3-month Euribor is around 2%.

6 Likes

Many short-term bond funds were slightly down yesterday or today, presumably related somehow to the events in the Persian Gulf and market panic. On the other hand, at least Seligson’s money market fund did not decline. This is a daily movement, not a longer-term trend.

2 Likes

At what age did you start bond investing alongside stock investing? I personally thought that at around age 50, I would set up a fixed-income portfolio to bring stability alongside my stock (ETF) portfolio.

That age is starting to approach; are there even any others this old here? ![]()

1 Like

It’s hard to give a single answer regarding adding fixed income at the age of fifty, as everyone’s situation is slightly different. I’ll outline it through a few different factors:

- Risk tolerance. If being 100% in stocks doesn’t cause your nerves to fray, fixed income investments aren’t necessarily justified.

- Risk tolerance. If you’re reaching, say, 50 and don’t have the best possible education or background in a field with a high employment rate, gradually adding fixed income might be justified. Similarly, if health challenges start to arise.

- Time horizon. My own goal is the option to FIRE/downshift at age 50. I started gradually adding fixed income at age 45. Before that, I even had a tiny bit of leverage. The closer the need to use the funds gets, the more it makes sense to bring fixed income into the portfolio.

- Portfolio size vs. need for money. If you only need a marginal amount from the portfolio for living (e.g., 2% or less), you don’t necessarily need much of a fixed income position, as you won’t need to take a large chunk out of the portfolio annually even during a larger dip.

In my opinion, everyone has to think through the answer themselves from several angles to fit their own situation.

12 Likes

Hi. I’m 60 years old myself and have 3 ETFs and about 15 stocks. I don’t have any plans to invest in bonds yet, and I probably won’t. You have to determine the risk level and investment goal yourself according to your investment plan. Based on your own situation and risk tolerance. Just my opinion. ![]()

7 Likes

In my own investment portfolio, there is currently a peculiarity such as about 15 hectares of farmland, which I lease to a local farmer. The idea is to sell these off in the coming years and invest the money in an easier-to-manage asset with the same risk level. That is why I am thinking about this interest rate matter.

Now the idea would be to allocate the money roughly as follows:

-30% to European government bonds

-50% to Eurozone Investment Grade corporate bonds

-20% to High Yield corporate bonds

1 Like

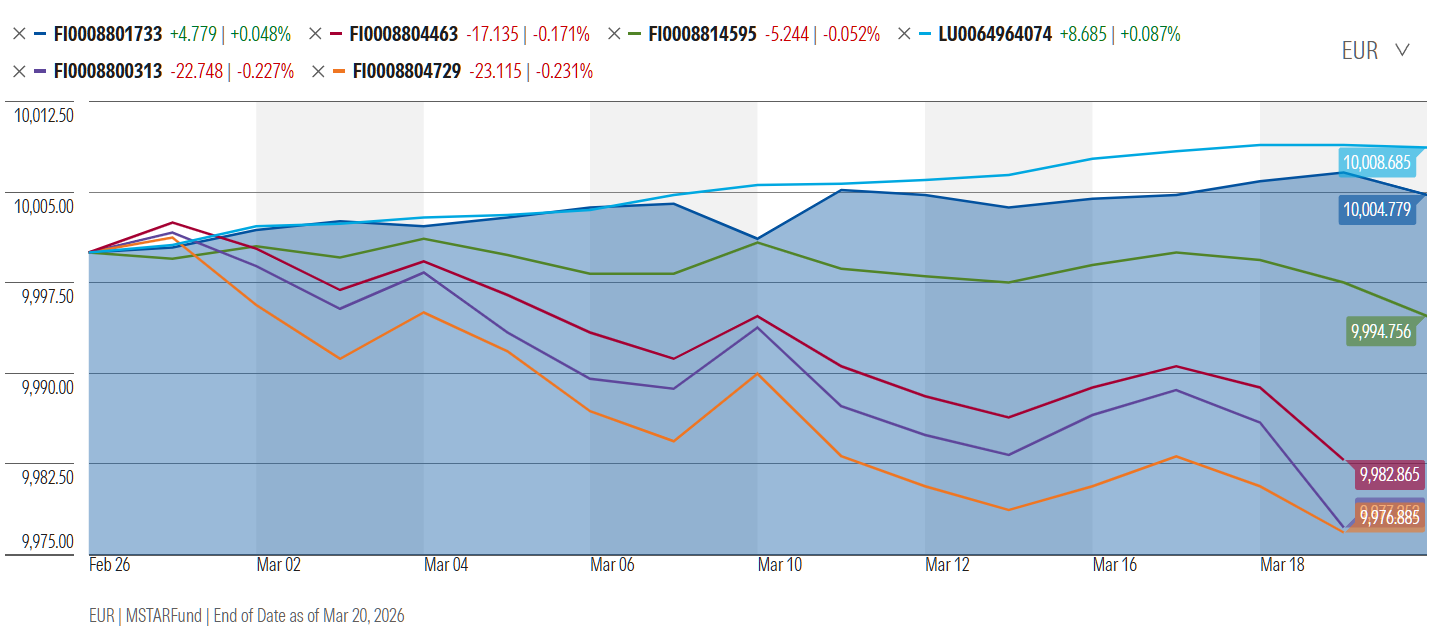

Stress testing short-term bond funds during the Iran War.

How well do bond funds serve as a cash reserve in different situations?

Blue: Seligson Money Market Fund

Red: Evli Liquidity B

Green: Nordea Fixed Income A

Light Blue: Fidelity Euro Cash A-Dis-EUR

Purple: S-Bank Short-Term Fixed Income A

Orange: LähiTapiola Short-Term Fixed Income

Fidelity and Seligson, as money market funds (or similar), have fluctuated the least. Among those containing slightly longer than very short bonds, Nordea has decreased but held its ground quite well (-0.5%). The funds that decreased the most were Evli, LähiTapiola, and S-Bank funds (approx. -2%).

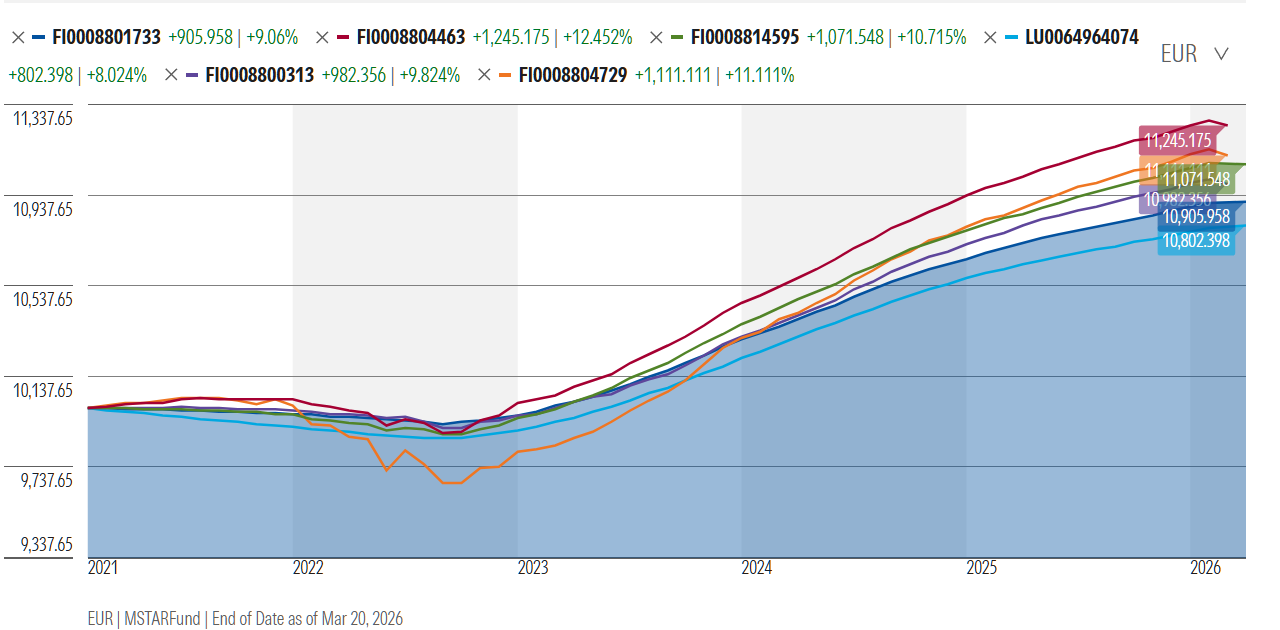

Over a longer period of five years, the situation is reversed.

To my eye, Evli Liquidity seems quite good for a longer holding period. However, there can be volatility in crisis situations. If one wants to minimize this, then Seligson or Fidelity. If one wants to avoid negative returns altogether, then the choice is a high-interest savings account.

22 Likes

Here, the cash equivalent is half in Evli Likvidi + half in a savings account and fixed-term deposits.

A fly buzzing in my ears, some 0.nn% fluctuation..

Can anyone tell me why OP Euro A has been drawing a straight line for a month now? Until now, it has been steadily ticking along with interest rates for years. Have they put the money in a drawer or what’s going on?

OP Euro is a short-term interest rate fund, meaning it holds papers with remaining loan maturities of even years. Tensions in the Middle East have increased risk premiums, which is reflected in the price of these debt securities. Interest rates have also risen slightly, leading to a temporary small negative impact.

That clarified things, thank you! I have this for reasons beyond my control, so I haven’t delved deeper into it.

1 Like

OP Euro, since it was mentioned, apparently no longer offers a bonus from that particular fund. However, I have at least at some point received a bonus from OP funds according to my bonus account, and I haven’t had any other funds with OP. I believe I checked this bonus issue last year when investing, and it was part of my investment decision to use it as a place to store my capital buffer. At least for now, the capital buffer has been moved to Collector’s savings account.

As I understand it, this is a change, and I don’t think it has been communicated very well to those who have invested in the fund. I have read the page below before, but I haven’t paid attention to that additional note.

Funds and investment-linked insurance savings*

*Excluding OP-Euro investment fund, institutional series funds, third-party funds, and structured loans, which do not accrue OP bonuses.

3 Likes