The company is trading at a P/B level of about 0.7. New shares were issued to the seller at a valuation of approximately P/B 0.8, which is better than the market price. That is okay in itself.

But the big picture raises questions.

About half of the deal was financed with debt. If the net yield of the Finnish rental housing stock is around 3–4% and the cost of financing is 4–5%, the portion financed with leverage does not inherently create value without a clear discount on the purchase price or exceptional operational improvement.

The biggest question, however, is the balance sheet.

If the company trades at 0.7x book value, the most rational move from a shareholder’s perspective would be to sell assets close to book value and buy back its own shares clearly below that.

If this cannot be done, the question inevitably arises: are the balance sheet values truly realizable in the current interest rate environment?

A P/B of 0.7 can mean undervaluation – or it can mean that the market does not consider the balance sheet values to be valid.

This transaction shifts the focus away from that test. From a shareholder’s perspective, the key thing would be to get evidence that balance sheet values also hold up in actual transactions, not just in valuation models.

Varma’s occupancy rate was 83%, and 98% of their apartments are in growth areas.

Surely it can’t be that low unless something like 10% of the units are under renovation, or are our pension assets really being managed with such a “couldn’t care less” attitude?

I think Kojamo trusts its ability to find a tenant better than Varma does.

does it matter in practice if the balance sheet value is somewhat higher than reality.

”The fair value of investment properties at the end of the financial year was EUR 7.6 (8.0) billion, including EUR 40.1 (0.0) million of Investment properties held for sale. Liabilities EUR 3,391 million.”

Kojamo’s market value is 2.29 billion, which is well over half of the balance sheet value. Of course, the increase in apartment prices affects the market value the most, but I’m sure buying Kojamo is a safe enough way to invest in real estate.

From an investor’s point of view, the most essential thing is to consider the change in FFO per share. The goal of Kojamo’s strategy, updated yesterday, is to grow FFO per share by an average of 3–5% per year until the end of the strategy period, i.e., 2028.

If the integration does not proceed as expected (the biggest challenge is certainly raising the occupancy rate of Varma’s portfolio), FFO per share could even weaken as a result of share dilution.

Furthermore, Kojamo inflated the balance sheet values of the properties on its own balance sheet by billions during the real estate bubble of 2019–2022. But it only wrote them down by a small fraction. In reality, their values are lower than in 2019.

Based on these grounds, why would anyone believe that Kojamo’s apartments are on the balance sheet at fair value?

Generally speaking, I am of the opinion that Kojamo is currently bankrupt from an accounting perspective, meaning the real value of the apartments (i.e., what would be available in a forced liquidation) is lower than the company’s debt.

Looking at the situation at the turn of the year (i.e., before this new transaction), the total balance sheet value of the properties was €7.6 billion and debt was €3.4 billion. Thus, the net value for shareholders based on balance sheet values would be €4.2 billion, but the markets do not believe in the balance sheet values; instead, the company’s market cap is only €2.3 billion. So, when calculating it this way, debt + market cap = approx. €5.7 billion. Can’t it be concluded from this that the market thinks there is roughly 25% “air” in the balance sheet values, but the value of the properties is still €2.3 billion higher than the debt?

A view based on which the “real value” of the properties would be lower than the debt would require that the balance sheet values have over 50% “air”.

I wonder if that is really the right way to evaluate such a large real estate investment company? Put the entire assets up for sale on huutokaupat.com all at once, see what price you get for the apartments, and that would then be the company’s true value?

I have a smallish position in Kojamo, picked up at under ten. Just in case, as a return to a feudalistic (no one owns anything, everything is rented) social model seems inevitable. I don’t have the time or energy for direct residential property investment.

I evaluate companies more based on their money-making ability than the book value of their assets. Kojamo isn’t exactly good in this respect, but if the world develops in the direction that I imagine, then it will improve.

I can’t help but ask how this differs from Citycon, which you apparently still consider sticking with even after the takeover bid?

In my opinion, it is indisputable that Kojamo’s apartments are overpriced on the balance sheet relative to their forced liquidation price, just as they are for every real estate investment company. I don’t quite understand why this detail keeps being brought up repeatedly. We shouldn’t care one bit whether the book values are reasonable, but whether the stock price is reasonable relative to the real value.

In my view, it is highly exaggerated, even absurd, to say that the value of Kojamo’s residential portfolio is less than the amount of the company’s debt. In practice, you are claiming that in addition to the stock market, the financial market is also valuing the company completely wrong, as the company has still obtained financing on quite reasonable terms (significantly better terms than Citycon, for example). You are also claiming that the “true” yield requirement for a residential portfolio heavily weighted toward Finland’s growth centers would be close to 10%.

With all due respect, I recommend reflecting a bit on what triggers these thoughts/feelings regarding Kojamo Especially when, at the same time, Citycon seems somehow attractive, so it’s not about the industry in general.

Reflecting on my own thoughts regarding Kojamo’s recent developments, I am on a cautiously optimistic track.

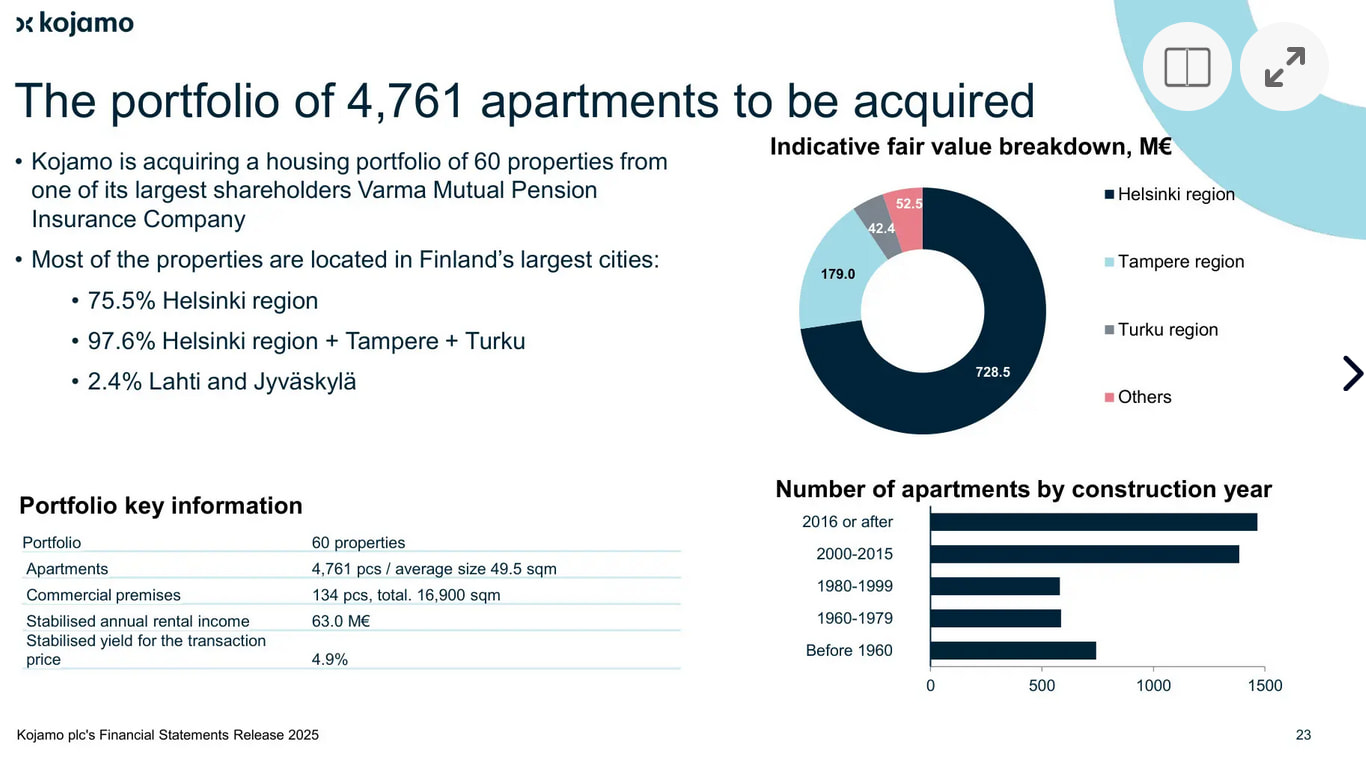

I believe the deal with Varma was good. Firstly, from a taxpayer’s perspective, it supports the idea that a pension insurance company should invest its assets according to its core competencies in areas where returns are better. When considering the occupancy rate of Varma’s housing portfolio, it is quite clear that managing this was not their core competency. Now they are involved in this business as a shareholder, and that is a good thing.

I strongly believe that Kojamo has a clear competitive advantage over Varma in managing a housing portfolio. Management costs, occupancy rates, etc., will improve for that portfolio, although in this size category and market, it may take some time. On Kojamo’s part, the prerequisites for growth in this construction cycle were pretty much frozen. This challenge was now countered with a massive investment, and I think it’s a good move, especially as pension insurance companies shift their strategies elsewhere and Kojamo’s negotiating position was likely quite good. Growth this year and next will likely come from the integration of this portfolio, increasing the occupancy rate, and I believe cost savings are also on the horizon. Perhaps construction will emerge as a clearer growth driver starting from 2028?

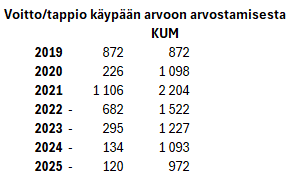

Regarding the balance sheet, I am quite optimistic. For four years now, Kojamo has recorded losses in its results from fair value measurements—additionally, overvaluation has been dismantled through sales losses. It is true that Kojamo’s cash flow model and its assumptions were ambitious and, at worst, led to inflated results. If I look at my own back-of-the-envelope calculation (attached) regarding the movements in the balance sheet and income statement, the profit/loss from fair value measurements has now returned to somewhere around the level of the first half of 2020.

Is the balance sheet healthy now or not? That is a very pertinent question. However, I no longer feel it is in any kind of critical state, even if there is still some overvaluation—the market also takes this into account in the pricing. The deal just made and the indication of financing apparently received for it suggest the same. I believe Kojamo can currently get senior debt at around the 4% level. If I do another back-of-the-envelope calculation: 600 million is financed, and the stabilized annual return on the entire investment is 63 million once the occupancy rate has risen. The ROE rises to 13%, which is already at a good level and could withstand a slightly higher interest margin.

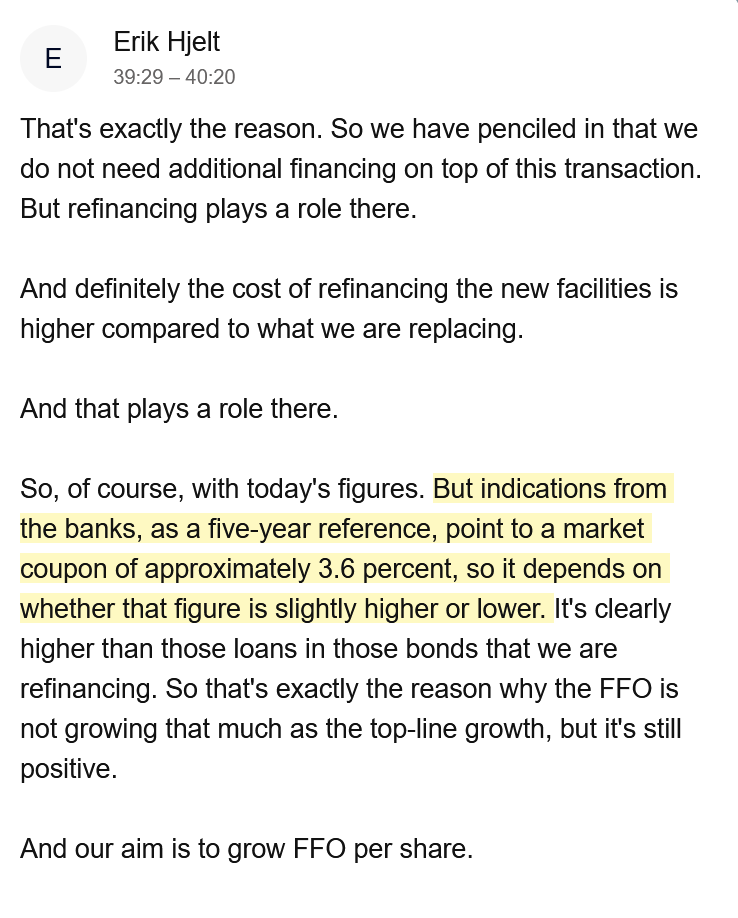

The company also stated in the Q&A session that it estimates obtaining bond financing at an interest rate of approximately 3.6x%. The current average interest rate is about 3.2%.

I wonder where they hold those stock market courses that teach companies to communicate as unclearly as possible, while still using plenty of officialese? Does, for example, the upcoming From Vantaa to the Stock Exchange program offer the capabilities to identify how strategic processes are kept front and center? In any case, whoever drafts Kojamo’s releases has at least completed Officialese I with top marks.

The notice of the general meeting also contains information about the upcoming (possible) name change; no actual separate news release has been published regarding this:

17. Amendment of the Articles of Association

As part of the company’s strategic work, the Board of Directors has considered changing the company’s name to Lumo Kodit Oyj. Renewing the brand and brand architecture is one way to strengthen the already strong Lumo brand and ensure the effective implementation of the company’s updated strategy. The Kojamo and Lumo Kodit brands would be combined so that in the future, the Company’s business name would be Lumo Kodit Oyj. The Board of Directors proposes that the general meeting decide to amend Section 1 of the Articles of Association so that in the future, the Company’s business name would be Lumo Kodit. The Company’s business name in English is Lumo Homes plc.