Are you claiming that management has not earned the share-based incentive scheme for which these shares are being purchased?

18 Likes

I wouldn’t be too quick to praise the strong cash flow, as its good level is mainly due to changes in fixed assets and the classification of lease liabilities as financing cash flows. It is, however, good that they aim to keep capital-intensive inventories at a suitably low level.

How do you think Kamux’s journey on the stock market and its financial performance have gone? Should destroying shareholder value even be rewarded? The reliability of management’s future outlooks is on the same level as their car salesmen’s.

4 Likes

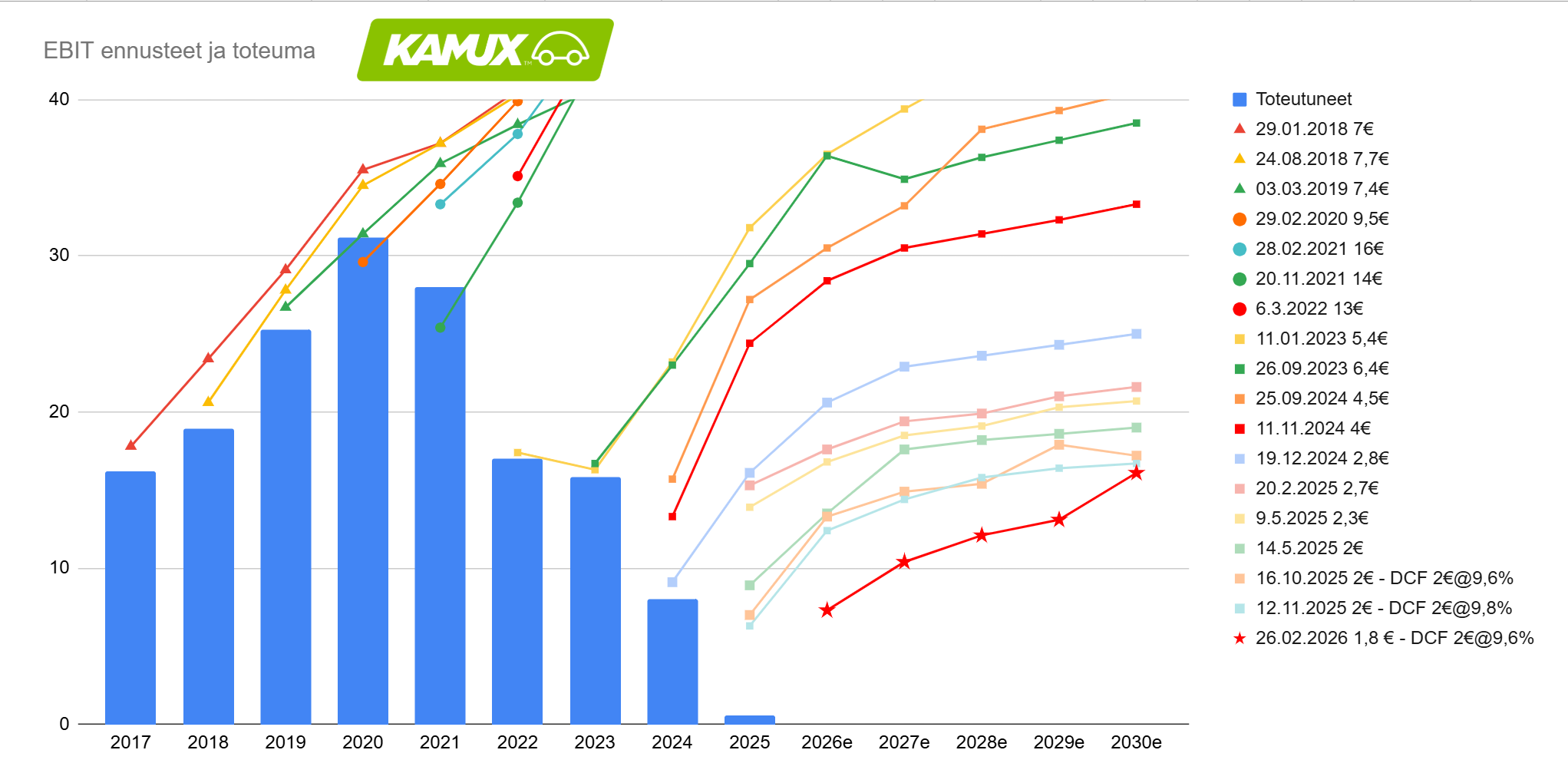

Here is a new company report on Kamux from Rauli following the release of the Q4 results. ![]()

Kamux’s Q4 result fell clearly short of our forecasts and turned into a loss. The company is guiding for an earnings improvement this year, which our forecasts also expect. However, based on the weak Q4, we lowered our forecasts for the coming years significantly (30-50%). We reiterate our reduce recommendation and lower the target price to EUR 1.8 (prev. EUR 2.0).

Quoted from the report:

Dividend proposed for distribution in the autumn despite the loss

Due to the weak Q4, Kamux’s full-year net result remained at a loss and, even without one-off items, was around the break-even level. Despite this, Kamux proposes a dividend of EUR 0.05 (totaling approximately EUR 2 million) to be distributed in the autumn. Kamux is also continuing its share buybacks by increasing the buyback program amount from one million to two million shares. At the current share price, a one-million share buyback program costs just under EUR 2 million, so the dividend and share buybacks combined are quite significant relative to Kamux’s weak earnings level. Strong cash flow and balance sheet enable the dividend distribution, but naturally, earnings performance must improve in the future for the dividend distribution to be sustainable.

4 Likes

Kamux - Finland’s Carvana

The erosion of the business has been dramatic despite sustainable competitive advantages. Forecasts have been following the decline. We are still waiting for a forecast that would be lower than the actual earnings.

22 Likes

Hi @Rauli_Juva

Could you explain in a nutshell where the positivity in your forecasts stems from?

Kamux’s Q4 results only highlighted the severe tailspin the company’s operations are in, yet you expect the business to recover to profitability immediately. You also mentioned that, in your view, the Q4 report didn’t outline any significant concrete actions to achieve a turnaround, so I’m curious to know what makes such an achievement possible in your forecasts?

11 Likes

Well, Kamux’s P/B is indeed very low already, if we assume the company can continue its profitable operations, which is very likely. The guidance can’t be [the reason] for a share price below 1.8; that already means the company is trading at 0.7x equity.

This is perhaps why Kamux doubled its share buyback program.

It’s cheap, for a reason, of course…

1 Like

Well, this is what I was trying to ask: why should we assume that?

If the company’s business trend is pointing in the opposite direction, it would be nice to hear why we should expect that direction to reverse immediately.

6 Likes

A small observation here: Kamux has €14.3M in goodwill and €1.6M in intangible assets on its balance sheet. If Kamux tries to hawk these to someone, they’ll get an incredulous look and an awkward laugh in return. So you can strip all that out when looking at Kamux’s P/B ratio. At least that’s what I do.

Regarding the treasury shares… they are given as incentives, so if they don’t incentivize and lead to better performance, it’s €4.5M of wasted money. You’d have to sell quite a few cars to fill that “share buyback pit” (lovely word).

Edit: I don’t know the terms of the incentive program, so it could well be that they actually have to perform well to enjoy these fruits. Hopefully the bar is high enough.

16 Likes

Yeah, this incentive policy for ever-declining results and money squandered abroad in megalomaniacal ways is truly incomprehensible. Shareholder value is certainly not being created with these acquisitions.

1 Like

Not all purchased shares go toward incentive schemes:

“The shares are being acquired for use as part of the payment of rewards for the Group’s performance-based matching share plan 2025–2029 and the Green Lions matching share plan, for the Board of Directors’ share-based compensation, and for developing the company’s capital structure by reducing equity”

2 Likes

A very relevant question; after all, we’ve thought a couple of times now that earnings are so low that they must be able to improve from here. If you look at Kamux’s last year, the decline in volumes started in Q2 and has since been roughly at the same levels quarter-over-quarter (or in terms of market share), taking seasonal variations into account. Thus, I believe Q1 will still see a slide in volume, but after that, the situation should stabilize. This, of course, also makes adjustment easier on the cost side when revenue isn’t leaking, and I do believe that under Kalliokoski’s leadership, some improvements can be made to operations that would support the result. Geographically, the improvement comes from a steady slight increase across all countries, even though international operations continue to show losses in our forecasts for the next few years. As I wrote, it’s hard to identify one clear, single concrete thing where the improvement would come from; it’s more about being able to perform normal buying and selling operations slightly better.

I don’t think our forecasts expect miracles in absolute terms, but you are quite right that, based on the Q4 result, this year’s forecasts could even be on the negative side.

The terms for the larger share-based incentive program are total shareholder return, earnings per share, and ESG. The threshold values for these haven’t been disclosed, but at least for the first two, no rewards can be granted from recent years. Additionally, the company has a so-called matching share plan (Green Lions), where those employees who are not part of the actual share-based incentive program receive an amount of Kamux shares corresponding to their purchases. The impact of this is smaller and naturally depends on the staff’s appetite for the shares and whether they have stayed with Kamux.

As @Tuul1puku pointed out correctly, not all of the 1-2m shares purchased should be swallowed up by incentives, at least not in the near future.

8 Likes

This is good to hear, meaning that perhaps not quite as much money is being thrown into the bonfire after all. However, ESG is one of those things that is easy to throw around, and based on it, rewards might be given even if the results are poor. It doesn’t provide much comfort to retail investors if ESG matters are in order, but the earnings are as muddy as a car in the spring.

I think this share matching is quite good. If you put your own money on the line, you essentially get shares at half price. There is surely some time limit after which the shares can be sold. If the share price doesn’t drop by more than 50% during that time, then it has been a good deal. I would certainly participate in this myself if I worked at Kamux. The expected value is good even though Kamux has had a difficult time.

4 Likes

Yeah, those items on the balance sheets of various companies are a bit of a common practice or an economic oddity, and Kamux is no exception. The stock is cheap in terms of P/B even if you were to cross out that €16M.

Now that February is coming to an end, we’ll soon see who has had an appetite for Kamux as a stock at this price level of under 1.80 and who hasn’t…

1 Like

Different companies’ balance sheets look very different. I wouldn’t quite make such a generalization about it being a local custom.

I agree that Kamux no longer looks very expensive on a balance sheet basis. After my own adjustments, I can get the P/B ratio to look below 1, but nowhere near 0.7. Since generating earnings has been difficult, the current price doesn’t appeal to me. There is, however, a price I am willing to pay for Kamux today, and it starts with a 1, just like the share price does at the moment. The cents just don’t match yet.

3 Likes

You can’t lose faith, and when going uphill, you just have to push harder!

I bought 1,200 Kamux shares at 1.77 each AND THESE WERE THE LAST Kamux shares EVER!

Now Kalliokoski can show his business skills, time to deliver!

Pajuharju wasn’t up to it.

It seems it was just too easy during Kamux’s growth phase due to the lack of competition.

Saka’s management was right when they said that competition will continue to intensify in autumn 2025.

7 Likes

It was easy to grow with the funds from the share issue, and in that race, they earned the top spot on the Consumer Disputes Board’s complaint list for car dealerships by a clear margin over other operators. The money is gone, but the reputation remains.

7 Likes