I wonder when Kamux will realize that the Sweden and Germany cards have now been played out. They should just exit both countries already and admit their mistake.

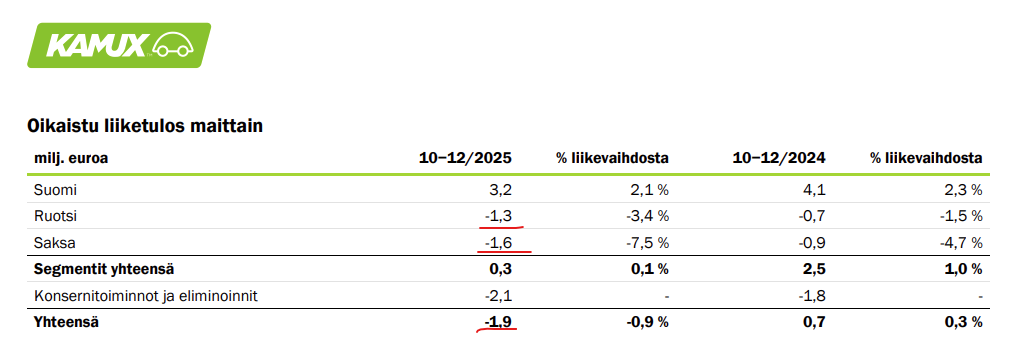

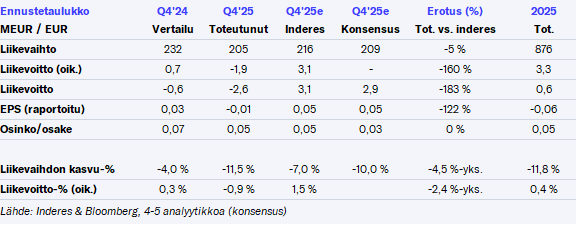

I had to do a double-take when I saw the headline “… adjusted operating profit fell in Q4,” but that’s exactly what happened, even though the comparison period was supposed to be exceptionally poor. The result fell and was below our estimates in all countries, which doesn’t leave much to add.

Guidance for this year is of course positive, and a dividend is proposed to be distributed in the fall, even though the result was loss-making.

The total maximum number of shares to be acquired during the acquisition period is 2,000,000 shares, whereas it was previously 1,000,000 shares.

However, a maximum of 4,500,000 euros will be used for the acquisition of shares during the acquisition period.

The shares are acquired to be used for the payment of rewards under matching share plans, for the Board of Directors’ share-based compensation, and for developing the company’s capital structure by reducing equity.

One can’t help but wonder at management’s faith in these international operations and the belief that they can be turned profitable. It would certainly be in the shareholders’ best interest to withdraw from them; the rate at which money is being burned there is quite staggering.

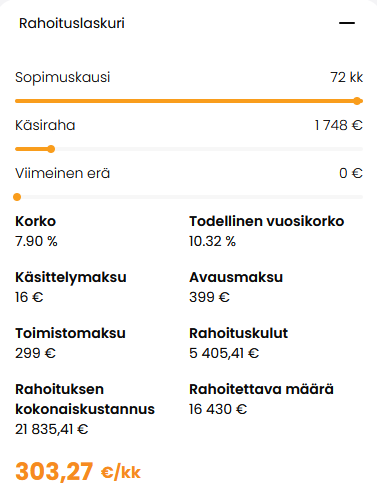

As someone who constantly has car fever, I follow the cars for sale on Nettiauto quite a bit and occasionally ask for trade-in offers. For a long time now, I’ve been wondering how Kamux manages to sell cars, as while other dealerships have similar price levels, Kamux’s financing interest rates are much higher than those of many competitors. Many large dealers have had interest rates for used cars between 1.99–2.99 for a long time, whereas at Kamux, it’s something else entirely. My understanding is that cars are largely bought, at least partially, with financing.

Now these figures reveal what many have been wondering regarding Kamux’s low valuation – Finland’s profitable result doesn’t help at all when the international operations eat it up completely. This has been priced into the €2 share price, but the numbers were even worse than I expected. And the decline will likely continue until the Swedish and German operations are shut down.

It’s a positive thing that the car dealership chain in the eye of the VAT mess mentioned in the Talouselämä article is J Rinta-Jouppi Oy, and not Kamux.

They also specifically mentioned in the briefing that Kamux does not use subcontractors (frontmen) when purchasing cars.

Kalliokoski spoke about customer satisfaction at least 10 times, and while it is an important matter, he could have opened up a bit more about other things too…

This is not true for the largest competitors specialized in used cars (SAKA, Rinta-Jouppi). None of the aforementioned offer those kinds of interest rate levels in used car sales. That interest rate level (under 3%) is one where a car dealership loses money on every single financing deal sold. Such a path is completely the beginning of the end for a company, as financing is an extremely critical element of profitability.

Kamux’s CEO said the following about the matter in his review: “Due to the weak demand for new cars, competition in the used car trade remained tight, and like the previous year, we saw significant interest rate offers in the market at the end of the year”

Clearly, the market is difficult and they are trying to boost sales with all sorts of means. But 1.99% financing for a used car sounded radical enough that I took a quick tour of the car dealerships’ websites. I pulled a VW Touran costing about 15-20k out of thin air for comparison. I’m sure the terms could be improved by providing credit and income info, etc., but I just took what the websites offered.

From Rinta-Jouppi, you’d have to request a quote separately; I didn’t go that far.

The best moment in today’s Kamux English Info session was when someone asked/pointed out that Kamux’s operating expenses were elevated in Q4.

CFO Sintonen looked puzzled and glanced over at Kalliokoski as if to ask if they were…?

Of course expenses were high since you made a LOSS..

I have been calling for a cost-cutting program at Kamux, but apparently management doesn’t feel that operating expenses are high; only the rent for the business locations seems to be a sore point. What about the large corporate expenses and the folks at the office in the warm?

Good examples of interest rate offers from Kamux and its competitors. But it’s always worth talking about the Annual Percentage Rate (APR) in accordance with the Consumer Protection Act so that they can be compared against each other.

The nominal interest rate of a loan might be 2%. Once the loan’s establishment fees, office fees, account management fees, and interest are added up, the APR actually turns out to be 6-8%. From the customer’s perspective, it only causes confusion when the actual costs of the loan are divided into five different components called by different names. I even know someone in my own circle of acquaintances who thinks they’re getting a good interest rate offer this way, not bothering to consider the big picture.

Well then, a nearly -90% crash from Kamux’s bubble prices in just a few years. Quite an achievement. The stock market’s ability to assess Kamux’s near future was completely off back then, in light of today’s information.

It’s shocking that Kamux does car business for a while and then realizes again that they’re stuck with these lousy trade-ins that nobody is interested in. In Germany, they had been clearing out stock to wholesalers in a “could we get at least something for this?” fashion.

Always the same story. They take some crap in as a trade-in and then end up holding the bag.

Kalliokoski also said in English that decision-making for buying and selling has been further decentralized to the showrooms and individual salespeople. It wasn’t that long ago when they were heading in the opposite direction—centralizing things and practicing data-driven management in the name of data analytics.

Maybe this “back to basics” will eventually bring the light; things are looking a bit brighter now, according to Kalliokoski.

Wouldn’t it be better to invest those funds in streamlining operations and exiting unprofitable markets rather than in share buybacks in a situation where the company is unable to turn a profit??