Prices were raised in Q4 2022 and further hikes in Q1 2023. Interestingly, InPost is apparently able to raise prices less than its competitors and, in exchange, gain more volume from merchants, which improves locker utilization and profitability. This is how they intend to improve profitability during H1 2023, though inflationary factors are expected to be a headwind again in H2.

In the Q4 call, it was mentioned that Q1 has gone well, especially January and March, and there has been growth in volumes even though the e-commerce market has apparently slowed down in general, meaning they have gained market share.

I assume Q1 will therefore be good, and we’ll probably hear more about how Q2 has started then.

The share price has, of course, risen strongly, so I should calculate its valuation to see what to make of it, but things are going quite well.

Investments are needed in Southwest France especially. The UK needs more logistical capacity as there is demand for lockers… it seems the partner is changing there.

In my opinion, the best thing is if they can raise prices less than competitors and gain market share while simultaneously improving profitability (which had naturally declined in 2022 when no price hikes were made, impacting the operating profit).

The debt load is quite high and the intention is to reduce it, but with current interest rates, it certainly affects profitability to some extent.

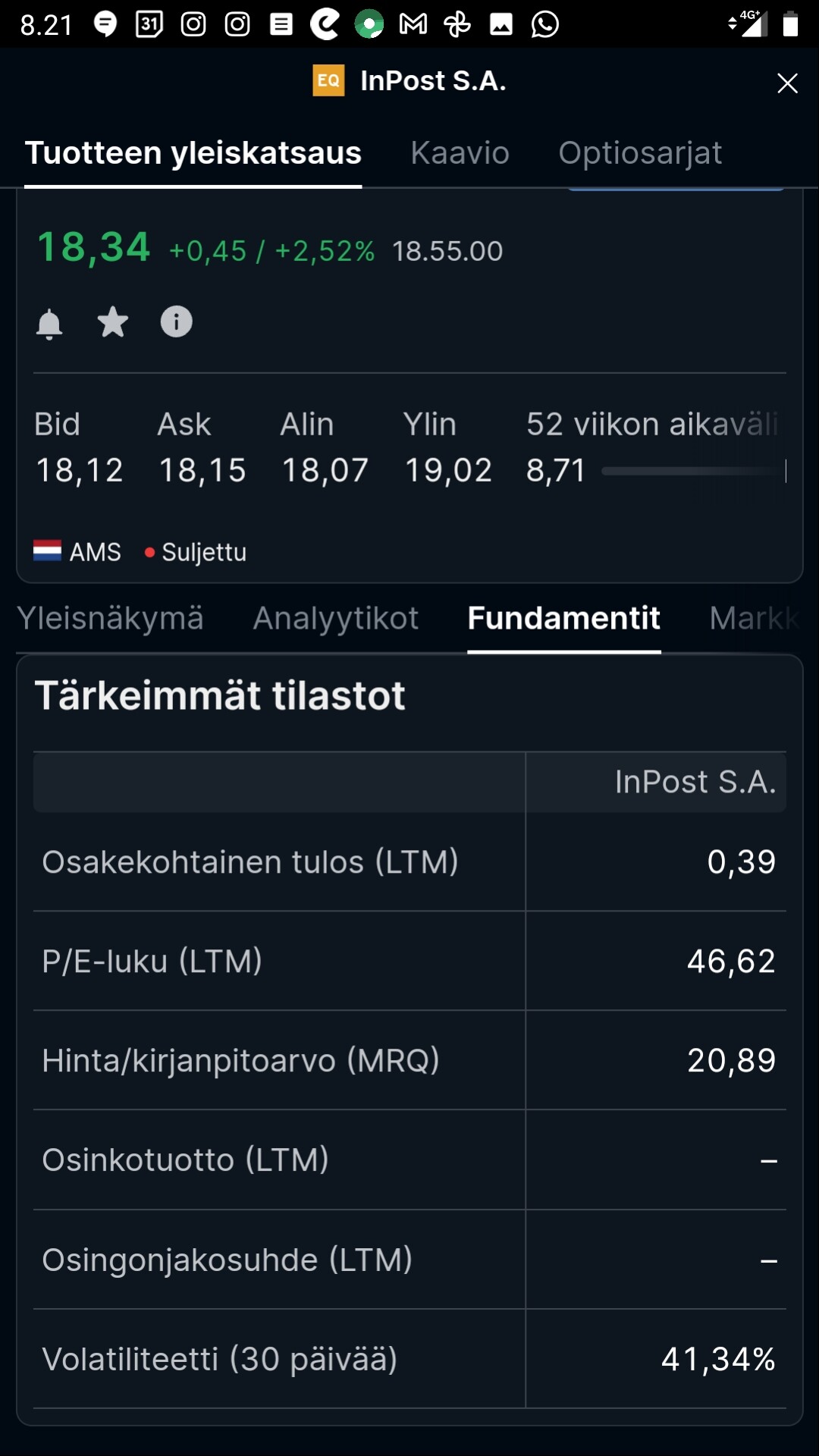

The P/E does look quite high. Capex is 1.2 billion Zloty, approx. €259 million.

Net profit after tax for 2022 was approx. €100 million.

Most of the Capex goes into parcel lockers. About 60% if I recall correctly. Some to logistics centers and some to software.

However, InPost wouldn’t have to expand all the time, and CAPEX could probably be put on the profit line?

I don’t know how investing is done, but if we took that 259m and 100m euros (yeah, I switched to euros), what would that be per share? =

SHARES OUTSTANDING 500M, so €0.71/share.

If I could be bothered, I’d look at the Q4 margin development and calculate that Q1 will bring double-digit growth in volumes and some more price adjustments, so Q2 will probably be the best quarter after that before costs hit.

The next price increases would then come at the end of 2023 after that Q1 2023.

Someone should go and set Viljo straight on how to crunch those numbers

My take is that volume is rising, relative profitability is increasing, and the geographical reach is expanding, where improvements to profitability (investments) need to be made. Poland, however, is a cash cow, and the density there will soon be at a good level, allowing investments to be increasingly shifted to France and other markets.

Besides Poland, the focus seems to be on France and the UK.

I’m not in any way qualified or reliable to evaluate those figures, so take a look for yourselves.

I listened to the latest conference call. It was professional and very well-executed. Many companies could take a leaf out of their book.

Poland is now a cash machine with a dominant position and is generating strong results. It’s also amazing that 10 million people use InPost’s mobile app, which is 1/4 of the population! Such app penetration opens up interesting possibilities. The CEO mentioned that they will soon launch a financial services feature in the app. This is an interesting expansion, and more similar ones could be on the way.

France and the UK are currently in investment mode, which is weighing on the results. But it seems they might turn profitable in about a year. In these countries, the market share is still small.

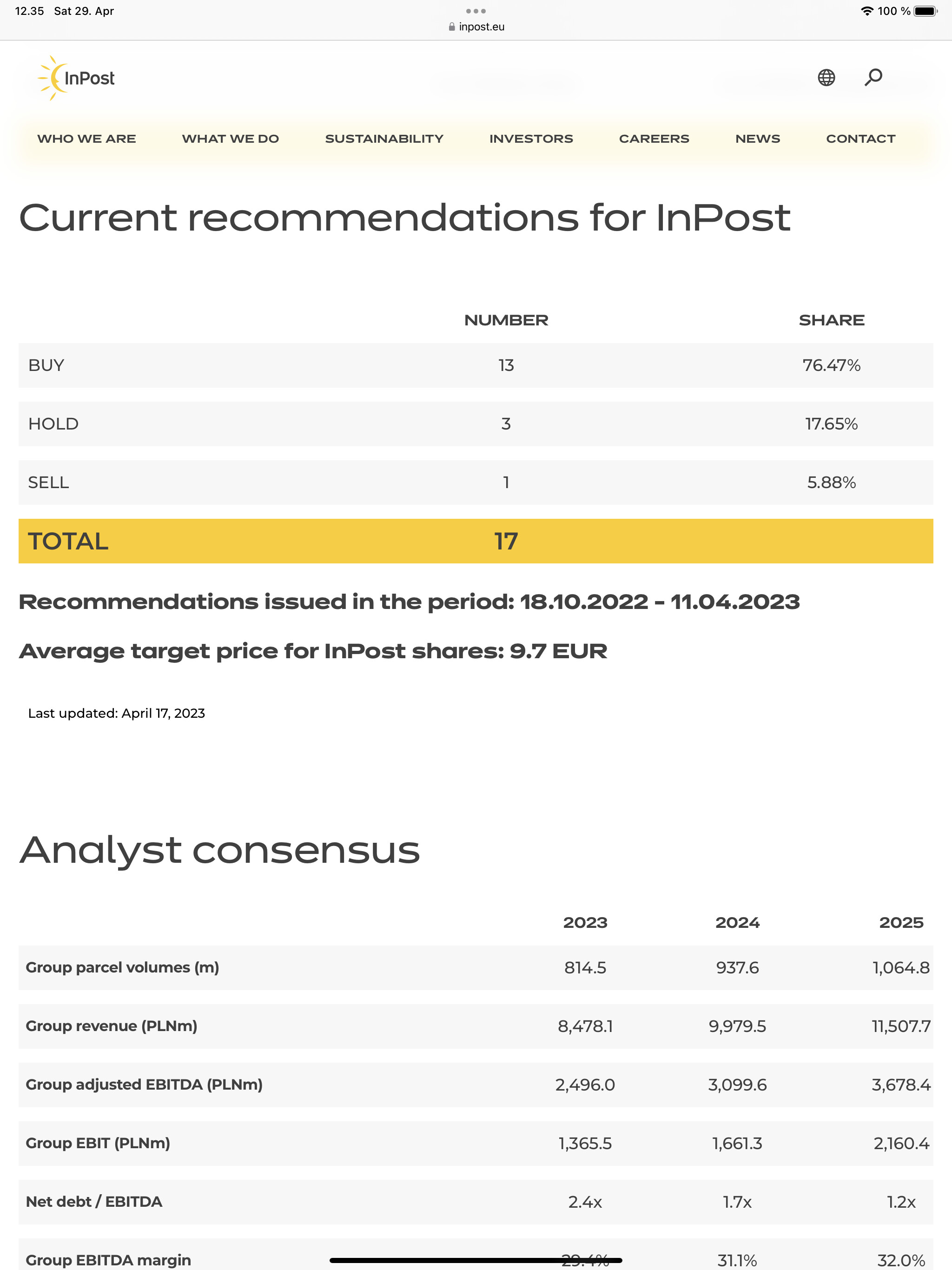

I wonder what the situation in this industry will look like in Europe in five years. One could imagine that there will be a few giants and a bunch of small local players in the market. It really feels like there’s a strong moat and network effect here. By then, these companies should be making very good profits. But InPost is already profitable, which is a great achievement for a growth company. The analyst coverage is high caliber, with questioners representing the likes of Goldman Sachs and Citibank. Here are the analyst forecasts from the company’s website:

The case is moving forward nicely. It would be nice if this wasn’t just a monologue! I’ve now got buys at the 5.xx, 8.xx, 13.xx, and 17.xx levels. Cash is coming in and can be poured into growth that is clearly faster than the market, and debt can also be reduced.

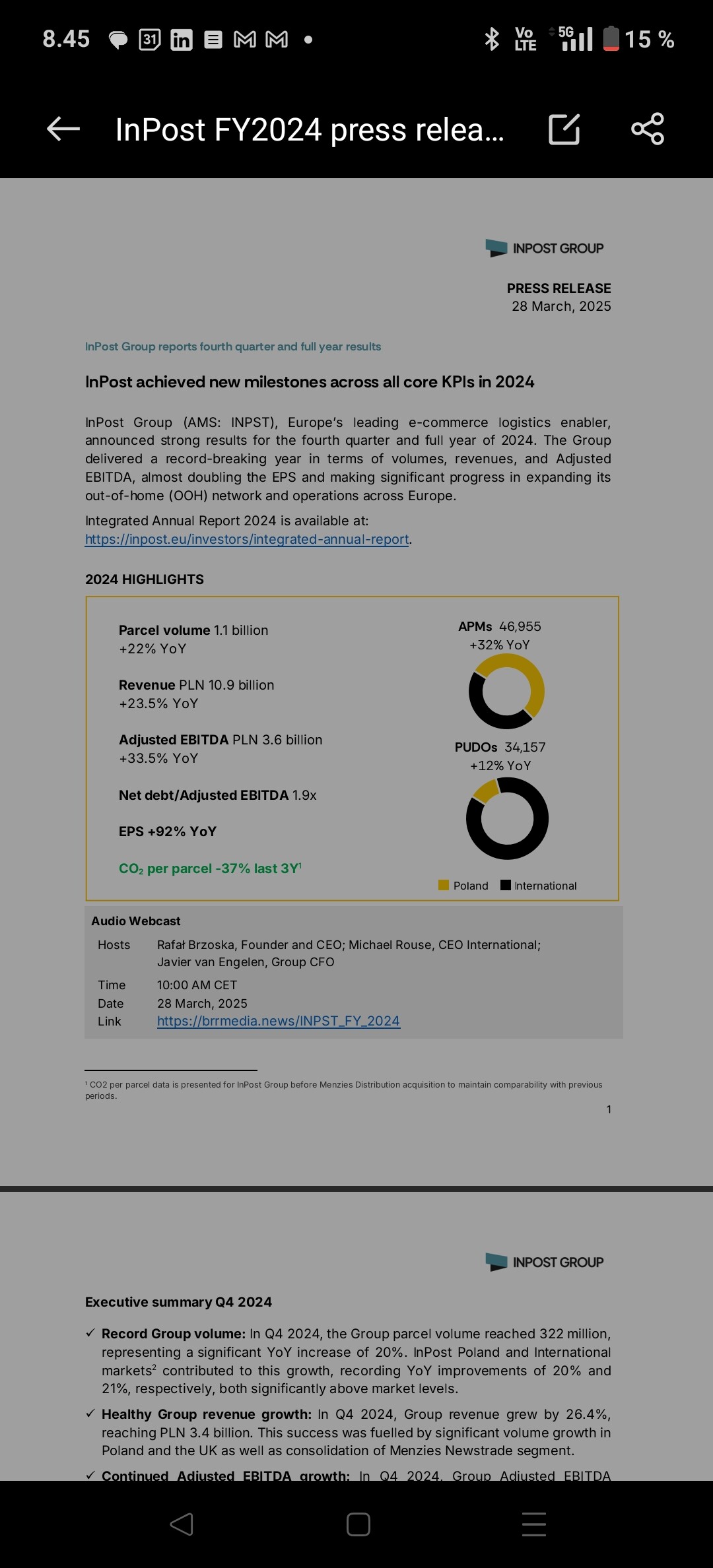

Today was the interim report and preliminary information on Q3 growth was provided.

I became interested enough to watch the latest Q2 conference call. At least based on that, the company left an interesting impression and I could well take a small starter position, so I’ll have the motivation to follow the company’s progress.

Apparently, it is the market leader in Poland and the most liked among those parcel service providers. The product seems to be in good shape, and the app seems to have good reviews in Poland and other countries.

In my opinion, there isn’t an excessive amount of debt, and the net debt/EBITDA ratio is decreasing at a steady pace. It has dropped quite quickly, though, from 2.7 → 1.95.

I suppose the core strategy for this company is that now that the domestic market has been conquered, let’s see how the conquest of Europe succeeds. At least from a geopolitical perspective, it might be nicer to get operations further west. Well, then there are probably bigger problems.

It seems it’s already No. 1 in France. Or close to it, and the UK is growing rapidly. But you can see from the figures how much expansion investment is ongoing, and it’s probably worth stepping on the gas.

Welcome along to follow, at least for now.

Of course, it would have been nicer to have bought much earlier, but I didn’t really have the energy to keep the discussion going.

I noticed this morning that an upward opening was expected on Euronext, it was up about 3.5%, but eventually turned into a decline of a couple of percent towards the evening.

In my view, the +40% margins in Poland are clearly financing growth in other Euro countries.

They seemed cautious, at least regarding the outlook for the rest of the year, since Q4 '23 was so strong. They also complained about cost inflation in the webcast—essentially hiding behind increased costs a bit.

FCF dropped the net debt ratio to 1.9. I understood that the Menzies acquisition was excluded from this figure, meaning net debt is probably somewhere around 2.2 now, at least that’s what I gathered from the webcast. English with a Polish accent isn’t exactly my strongest suit

So, as I understand it, a fairly unsurprising quarter, and we’ll wait for Q4 when they face stronger YoY figures. This doesn’t exactly seem cheap at the moment, considering a consensus beat is rewarded with a share price drop. An interesting growth story, all the same.

Information on growth has been provided again, and it’s progressing at a pretty good pace, although the UK should really step on the gas more. We are number one in, for example, France, Poland, UK.

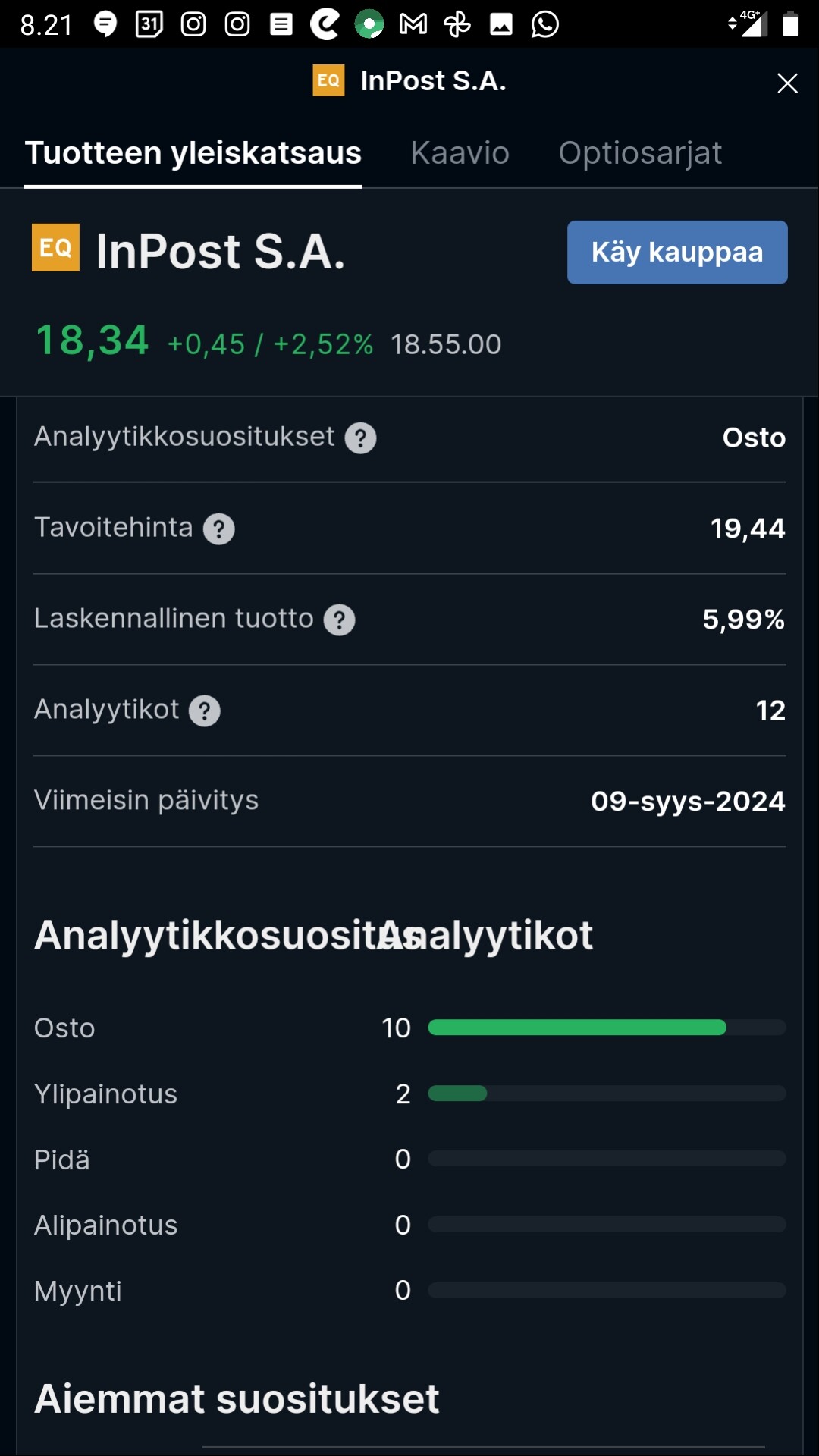

Inpost has 19 analysts, all of whom give a buy recommendation with an average price target of 19.55, and all recommendations have been updated between May and the present.

The share price just keeps falling, what could be the problem?

The next earnings report is not until September 2nd.

Inpost announced that they have been approached regarding a potential buyout, but there is no concrete offer on the table. The share price has been languishing at a fairly low level, but there has been quite a lot of movement over the last couple of days.