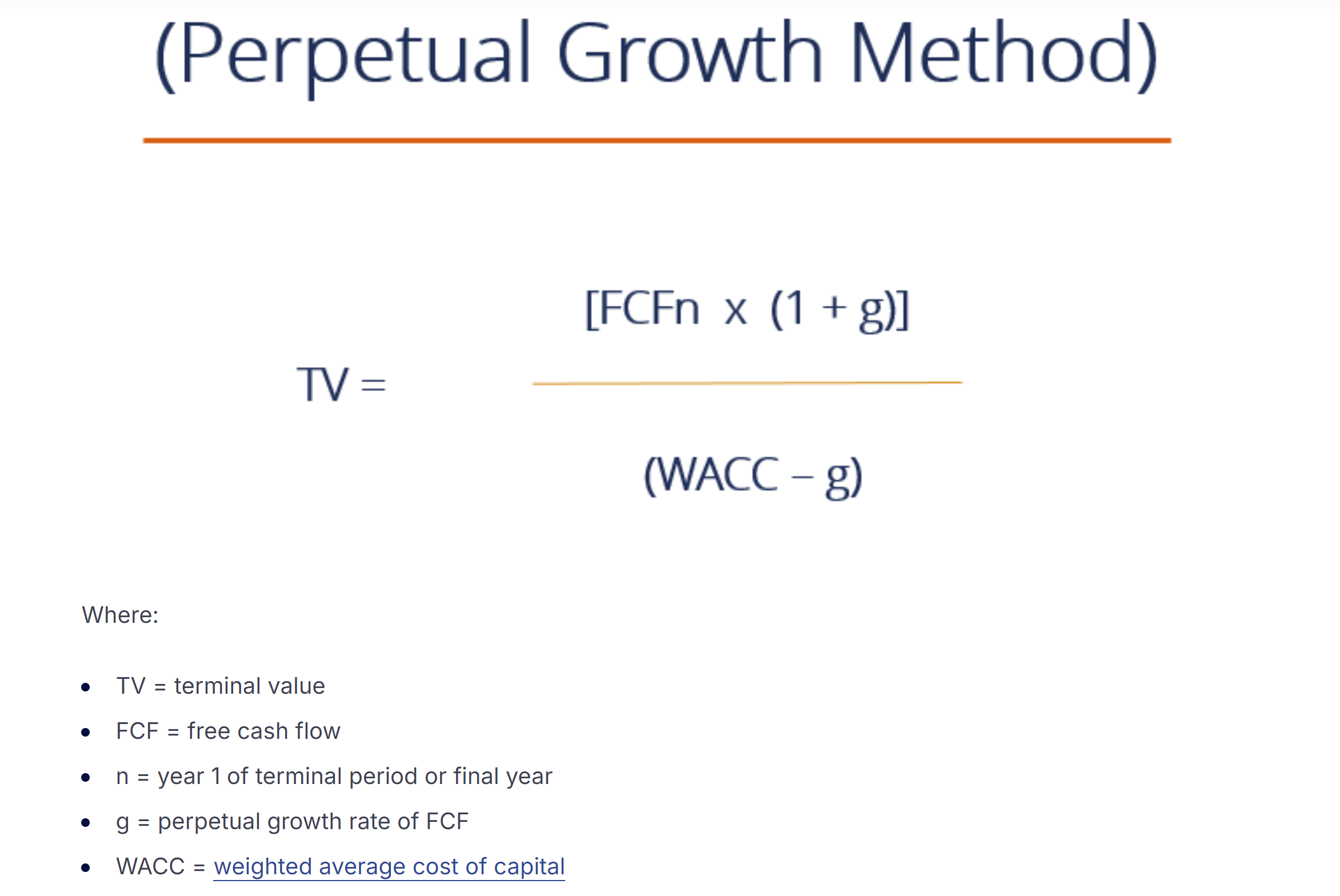

Inderes’ DCF model, like many other DCF models as I understand it, uses this so-called “perpetual growth method” (if I translated that correctly) for calculating the terminal value. In this method itself, effectively n years are discounted into the terminal value, where n approaches infinity (meaning all cash flows from years outside the forecast period are discounted to the present value). The terminal value is mathematically just a multiple of the last forecast year’s cash flow, but this can also be understood in a very simplified way such that the estimate for a single year’s discounted cash flow is some x = TERM-value/n, where n = the number of years included in the terminal period. You can vary the value of that n-variable as you wish, but the closer to infinity you go, the smaller the cash flow for a single forecast year becomes.

So, as an off-the-cuff example, if you chose n = 10, then with that value x = 10, but correspondingly with n = 20, the single-year cash flow would be x = 5. In the latter estimate, the “required” cash flow from the company in the first years of the terminal period is smaller, but the uncertainty of the forecast increases because you also have to assume a certain result from the company in year 20 (in this example, 5) ![]()

I’ll conclude by saying that I simplified the concept of discounting in the terminal value quite drastically at the end here, and personally, I prefer the thinking that the terminal period contains an “infinite” number of years, all of whose cash flows are discounted to the present day using a single formula (see above). So, in practice, the cash flow of a single year itself has no greater significance to the terminal value than the fact that if cash flows are cumulatively smaller at some point in time than what has been included in the TERM-value, then the realization of the model’s value at some time t becomes even more uncertain (the possibility of which the company’s WACC should reflect somehow).