If you want to browse the 2025 annual report, it is now possible. A few hundred pages to browse through.

20 Likes

How are the current expansions progressing according to schedule, such as the Sadat City investment? Is the capacity for the investments on the Fiber side already “pre-sold,” so to speak? Based on the margins, pricing power and demand seem to be in better shape than in other sectors.

7 Likes

Hi! Good question!

The expansion in Egypt, which belongs to the Fiber segment, is still in its early stages, and it will take a couple of years before we see significant results from it. However, the investment is not as substantial as, for example, the expansion near Chicago in the USA. We have stated that we have not been satisfied with the slow progress in ramping up this egg packaging-focused plant, mainly due to technical challenges.

Regarding the Fiber segment, our utilization rates are at a very high level, and it was the only segment where investments increased last year. It is clear that we will need more capacity in the coming years as demand grows. Alongside egg packaging, fruit packaging in particular is a potential growth path. And when we consider different investment options, it is clear that acquisitions are also a realistic possibility that we are exploring at the same time.

/Kristian

54 Likes

By the way, what about Huhtamäki’s business in the Middle East? Do they own production facilities there? I seem to recall that they might have at least partial ownership of something. It would also be interesting to know how much the Middle East crisis directly affects Huhtamäki; increased freight costs at least come to mind. It unfortunately looks like the crisis is dragging on, though of course, a lot can happen in one night during US prime time. Did @Kristian_Tammela have time to answer?

You can see it conveniently from the map on page 9 of the annual report. There are three production facilities right there in the Persian Gulf coastal states, in Saudi Arabia and the United Arab Emirates.

22 Likes

Yes, we have two factories in the Flexible Packaging segment in the UAE and one factory in the Foodservice Packaging segment in Saudi Arabia.

Assessing the impacts of the situation is difficult; it depends very much on the duration of the situation. Energy as a cost relative to net sales is typically 3-5% at the group level. Furthermore, the price of oil affects the price of plastics, at least to some extent and over some timeframe. If our raw material costs rise, we must pass them on to sales prices. Freight costs are also typically around 3-5% relative to net sales.

It is, of course, more difficult to assess how this might potentially affect demand. That remains to be seen, and I cannot speculate on that at this stage.

I hope this helps!

/Kristian

91 Likes

Regarding the Hammond factory, the Mayor of Hammond spoke in an interview about an additional 10 million investment. Is this related to overcoming technical challenges or, for example, improving logistics? Is the factory currently running at full capacity?

9 Likes

Hi! Apologies for the delay! The factory is still experiencing technical start-up difficulties. The background for this is a large wave in the US market to replace Styrofoam packaging with fiber packaging for eggs. While egg cartons in other markets are grey/brown, i.e., made from recycled paper, in the US, several large customers want colorful egg cartons. Integrating the dye, especially white, into the integrated process has been more challenging than expected, as this is new.

In addition, most production lines are focused on 12-egg cartons, and one on 18-egg cartons. The market demand profile has changed rapidly, with customers wanting larger cartons. Some customers combine these, meaning if they want to sell smaller cartons, they also want large ones. The mentioned additional investment is related to adding another 18-line to the factory, which will also balance our production somewhat and thus support the sale of smaller cartons. We have full confidence that we will get things rolling as planned, unfortunately, it has taken too long.

PS. Today we held an earnings call on the theme of sustainability, and the recording can be found here: Sustainability results 2025 call

/Kristian

99 Likes

Here is a quick read about Huhtamäki from SalkunRakentaja. ![]()

The positive expected return is driven by a combination of low valuation, a strengthened balance sheet, and dividend yield. For a contrarian investor, Huhtamäki is a typical case where market caution has pushed multiples to the historical low end for a relatively high-quality company.

Subheadings:

- Savings program delivered results faster than expected

- Multiples have dropped to the historical low end

- Fiber Packaging is performing well, other segments are stalling

- Risks and opportunities in balance

38 Likes

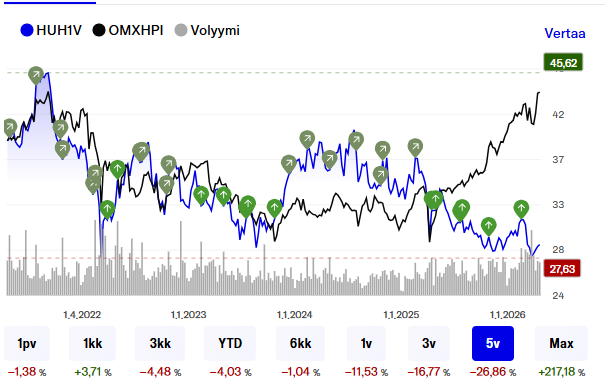

The chronic undervaluation is truly baffling. P/E 11, growing dividend yield of 4%, free cash flow of €311M, and yet the share price just keeps wallowing lower. If the earnings performance is like this during sluggish demand, what will it be if the market situation improves?

43 Likes

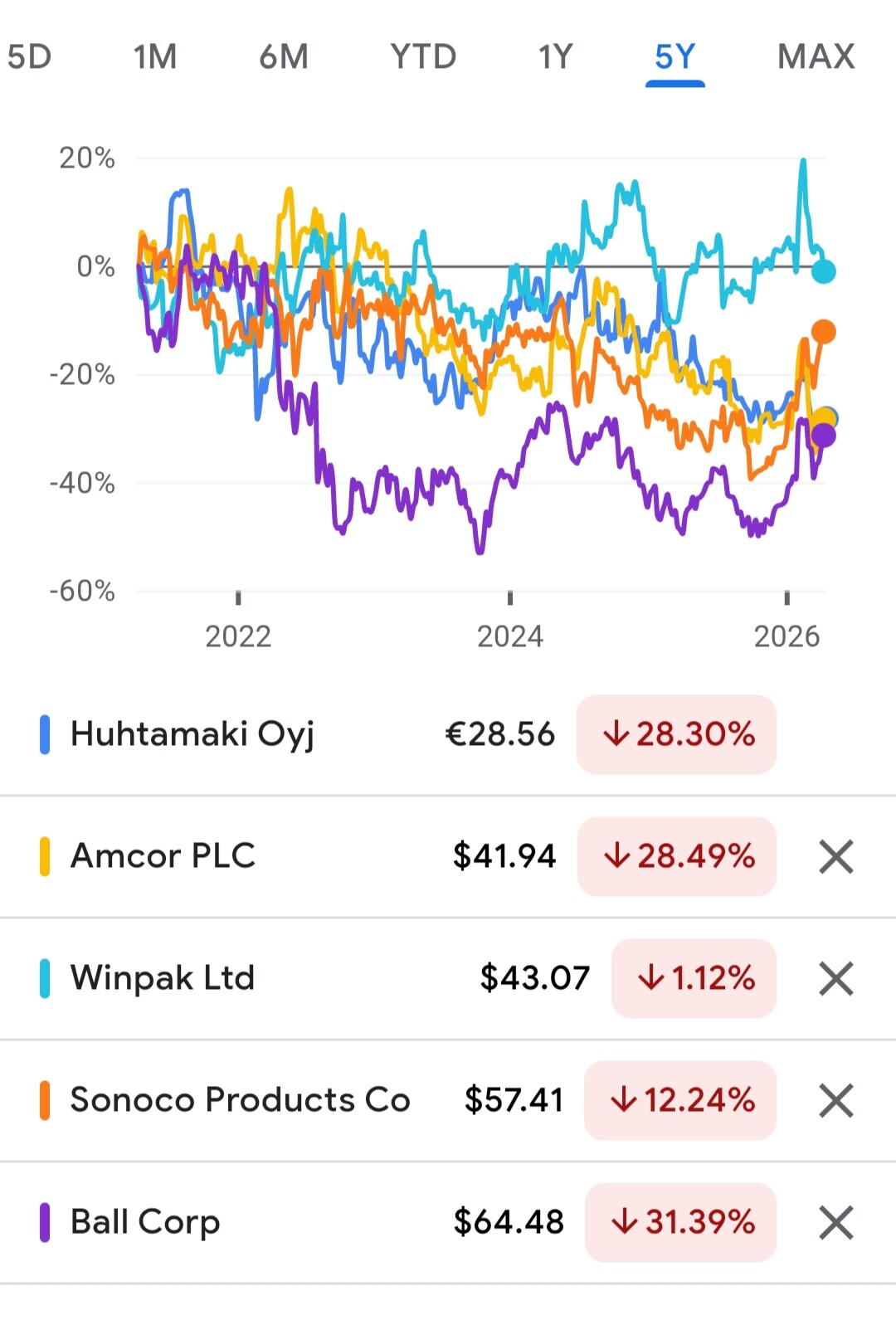

Based on stock prices, many listed peers haven’t performed particularly strongly in recent years either. There are, of course, significant differences in the companies’ product portfolios and geographical distribution.

44 Likes

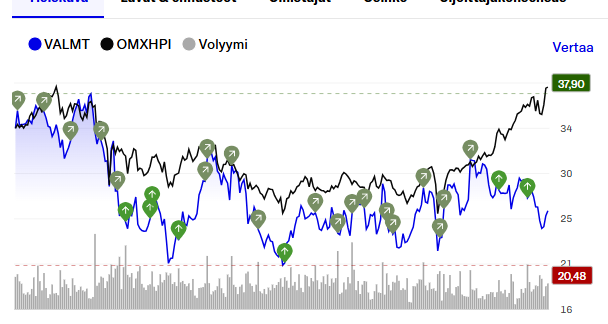

It seems to be much the same in other capital-intensive sectors as well; I just compared Valmet and Huhtamäki’s charts and key figures for fun, and to put it bluntly, they are exactly the same, both in terms of share price movements and valuation based on the figures. So I was thinking of adding one or the other to my portfolio… and looking back 5 years, it really doesn’t matter which one you pick ![]()

30 Likes

Here is Antti’s pre-result company report, as Huhtamäki reports its Q1 results on Wednesday, April 29th ![]()

We reiterate our Buy recommendation for Huhtamäki and adjust our target price for the company to EUR 36.00 (prev. EUR 37.00) following a decrease in current year estimates due to the negative repercussions of the war in Iran on the consumer sector and raw material markets. Huhtamäki’s earnings growth outlook is shifting once again, but in our view, the upside potential of the low valuation (2026e: P/E 12x) and the dividend still encourage patience.

27 Likes

Inderes:

“Huhtamäki’s adjusted P/E ratios for 2026 and 2027 based on our forecasts are 12x and 10x, and the corresponding EV/EBITDA multiples are approximately 7x and 6x. Dividend yields for the coming years are at the 4% level. Multiples for this year have already slipped approximately 10-15% below the company’s 5-year medians. We consider these valuation levels moderate for Huhtamäki, given the company’s reasonable longer-term growth outlook and fairly defensive business portfolio. The stock’s one-year expected return, consisting of valuation upside and dividends, still clearly exceeds our required rate of return. The DCF value also supports a clearly positive view of the stock.”

27 Likes

Having stagnated for years, Huhtamäki is drawing more and more talk among investors as the share price continues to slide. But is it a value trap?

I challenged Antti on this at the end of last year, but the video hasn’t aged a bit. That’s why I’m bringing it back to the thread as a reminder. ![]()

55 Likes

An exciting day ahead tomorrow for Huhtamäki shareholders. Today, we’ve had an interesting preview from around the world of where the consumer sector is heading: Coca-Cola delivered a strong Q1 result and rose over 6% across the pond.

I wonder if food packaging has moved in the same proportion?

34 Likes

Once again, the quarterly report is out! Comparable revenue grew 1%, and comparable operating profit fell to EUR 94.5 million. In that figure, currency exchange rate changes had a significant negative impact of nearly EUR 5 million, and without it, growth would have been 1%. Additionally, cash flow was positive, whereas historically Q1 has often been in the red. The market situation remains difficult, and the war in the Middle East is not helping the situation.

As we mentioned in the Q4 call, the challenging weather conditions in the US affected the profitability of the North America segment, as several factories and distribution centers had to be kept closed. The impact was roughly EUR 5 million on operating profit. On the other hand, compared to the previous year, an early Easter supported revenue in the segment, especially on the seasonally sensitive retail side (e.g., cups and plates sold at Walmart).

As a new item, it’s worth noting that we are reporting the volume of external machine sales separately in the Fiber segment. In Q1, it was over EUR 2 million lower than in the comparison period. We sell machines (e.g., for egg packaging) and spare parts externally, mainly to markets where we do not operate ourselves. These sales typically fluctuate, and this allows investors to better see the underlying development of the actual product business.

The war in the Middle East has several impacts on us. In Q1, we lost some revenue in the region due to the conflict in the Flexible Packaging and Foodservice Packaging segments. There are some factories in the region; they are now operational, but logistics is a major challenge. Another issue is the availability of raw materials, mainly related to plastics. However, the situation varies by region, with Europe seeing fewer challenges than, for example, the Middle East, India, and Southeast Asia. Due to the conflict, plastic prices have risen significantly globally (but with large differences geographically and between grades). We are doing our best to pass these costs (and higher energy and logistics costs) into selling prices. Typically, however, there is a certain lag. More discussion on the matter in the earnings call

/Kristian

69 Likes

I’ll also add a link, was this even a defensive victory: Huhtamäki Oyj:n Osavuosikatsaus 1.1.–31.3.2026: Vertailukelpoinen liikevaihto kasvoi haastavassa markkinassa | Kauppalehti

Q1 2026 in brief

- Net sales decreased 5% to EUR 946.8 million (EUR 1,001.6 million), including a currency exchange impact of EUR -62.6 million (EUR 11.2 million)

- Comparable net sales growth was 1% at the Group level

- Reported operating profit EUR 83.2 million (EUR 93.7 million)

- Adjusted operating profit was EUR 94.5 million (EUR 98.5 million), including a currency exchange impact of EUR -4.8 million (EUR 1.2 million). The adjusted operating profit margin increased to 10.0% (9.8%)

- Reported earnings per share EUR 0.47 (EUR 0.54), adjusted earnings per share was EUR 0.56 (EUR 0.59)

Today is also Huhtamäki’s Annual General Meeting, so one gets to ask questions while they’re fresh ![]() .

.

21 Likes

Huhtamäki has gained quite a bit of attention lately based on the buy-and-sell thread.

Wasn’t this actually quite good, considering that currencies are providing so much headwind. Efficiency measures are taking effect and the margin improved YoY.

Revenue slightly weaker than our expectations, but in line with consensus

Huhtamäki’s Q1 revenue was EUR 946.8 million, about 2% weaker than our forecast (EUR 964 million) but practically in line with the consensus (EUR 945 million). Reported revenue fell 5% from the comparison period, but the currency translation effect was exceptionally heavy (-EUR 62.6 million). Comparable revenue growth turned positive (+1%), which is an encouraging signal after several weak quarters.

Adj. operating margin rose to 10% – efficiency measures are paying off

Adj. operating profit of EUR 94.5 million was in line with our forecast (EUR 94 million) and the consensus (EUR 92 million). A positive surprise came from the margin, which rose to 10.0% (Q1’25: 9.8%) despite the weaker revenue. Efficiency measures and higher sales volumes compensated for the negative impact of exchange rates and weather challenges in North America.

17 Likes

AI

The market reaction to Huhtamäki’s Q1 2026 earnings release is assessed as moderately positive, as the company managed to exceed analysts’ earnings expectations despite a difficult market environment.

Here are the key factors influencing the share price development:

-

Better-than-expected result: Adjusted EBIT was EUR 94.5 million, which exceeded the consensus estimate of 11 analysts (EUR 90.6 million). Adjusted earnings per share (EUR 0.56) was also stronger than the forecast (EUR 0.53).

-

Resilience of margins: Investors are reassured by the increase in the adjusted EBIT margin to 10.0 percent. This shows that the company’s efficiency measures and pricing power are effective, even though net sales fell by 5% due to exchange rates and challenging weather conditions.

-

Stable outlook: Huhtamäki kept its outlook for the full year 2026 unchanged, which provides stability to the market. Analysts, such as Inderes, had already reiterated their “buy” recommendation before the report due to a moderate valuation level (P/E approx. 12x).

-

Cash flow: The significant improvement in free cash flow compared to the comparison period is particularly positive.

18 Likes

When it snows even as far as Texas, it’s challenging to get workers to the factory, trucks moving, etc. ![]()

43 Likes