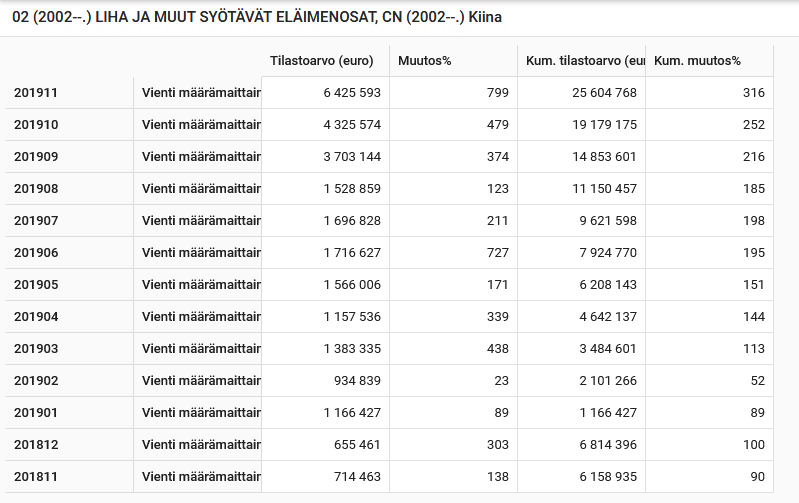

November export statistics published - meat exports to China in 11/2019 increased by about 800% compared to 11/2018, and by 316% for 1-11/2019.

4 Likes

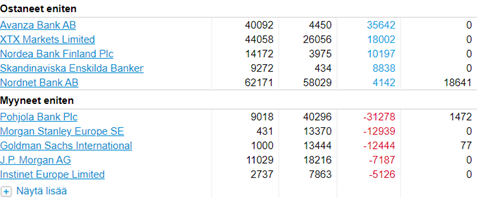

Nordea Life Insurance has disappeared from the list of owners. All sold, at least I couldn’t find it anymore.

1 Like

Congratulations! Sounds like the Nordea sales have been sold. We’ll hear on 6.2 how things are going for our boys and girls. The assumption is that Q4 is positive but revenue has slightly decreased from the comparative year. In 2020, we’ll already be clearly in a positive mood with positive business.

2 Likes

I bought the previous sizable batch, if I recall correctly, in 2015 at a declining price of 3.43 euros – an excessively large batch relative to my portfolio size (like 15% weighting). The inspiration probably came from none other than Sinko. ![]() I sold half for just under two euros after the last offering, as I had no faith in anything.

I sold half for just under two euros after the last offering, as I had no faith in anything.

Now I’ve added a small batch to my share savings account (OST), and the report will determine how I proceed with my holdings. A larger addition is psychologically very difficult; even this one was hard to swallow… Fortunately, its share of the portfolio is now only a few percent. So, my investments have gone better after the initial blunders. ![]()

Management seems to have things under control at the moment, and who knows, maybe poultry permits could be obtained for Asia? #justguessing The appreciation for Finnish raw materials there is very high. I’ve noticed this myself as a meat seller since 2010 (today, of course, as a hobby-income side hustle). ![]() When a company has a second consecutive quarter in the black, then it’s only then that we talk about a turnaround company, right? Let’s be excited about this!

When a company has a second consecutive quarter in the black, then it’s only then that we talk about a turnaround company, right? Let’s be excited about this!

4 Likes

Where does this assumption that Q4 is down year-over-year come from? Has the company itself mentioned this anywhere?

The company itself has not mentioned it. I read in some report that we are a bit behind for the whole year. Q4 revenue might show an improvement compared to the reference period. This is how I interpret that 2019 revenue would be below 2018 revenue. But I don’t think that has such a big weight compared to making a profit. Layoffs have had to be made in 2019 as well.

VR Pension Fund and the Finnish Cultural Foundation have sold quite a bit in December-January. Could it be Pohjola’s sales?

1 Like

4 Likes

I think the mood is pretty good.

Comparable operating profit is already pretty much at zero - maybe next year it will be in the black. It would have been great to see a positive (adjusted) EPS from Q4, but we’ll have to wait for the “jackpot” then.

The guidance for 2020 (“HKScan estimates the Group’s comparable operating profit to improve from 2019”) is perhaps a little bland for my taste, but I guess it’s better not to promise too much at this stage ![]() .

.

Exports are also expected to perform well in 2020, and as could be read from the previously posted Ilta-Sanomat news, work is also being done on permits for poultry and beef products.

4 Likes

It’s starting to look quite good, as profitability is improving across the board.

2 Likes

Well, it seems the results didn’t quite please the market. I would have expected a more positive reaction.

1 Like

The opening was already +5%, but the rise quickly leveled off. Let’s see in the coming days, when the results are written about, if new people get excited about a potential turnaround company ![]()

1 Like

The improvement in business cash flow from -€15m to +€73m bodes very well. I’m sure the stock price will also pick up a bit once the most impatient sellers get rid of their shares.

1 Like

Surprisingly lukewarm reception from the market, yet the report contains a lot of good news for Q4. Is the market now looking more at the full-year figures, rather than Q4, which nevertheless indicates a clear turnaround? Without the known write-down for Rauma, the operating profit would have been quite decent. To my eye, the report highlights a strengthened positive cash flow, improved profitability in all market areas, investment in the growing poultry market, and becoming the market leader in the poultry category. This will surely turn out well.

Regarding exports to China, they were quite cautious (“Demand in China is expected to remain strong in 2020. Market price volatility is estimated to continue”), so it seems it’s not yet a very significant business. A poultry export permit would be great.

1 Like

I wonder if this is the famous place to add ![]()

I have a hunch that this will turn out like Basware earlier this week.

A good interim report, but the most eager investors will be disappointed when no moon is promised and no dividend is paid. The share price takes a hit for one day (around -3.5% for Basware). The next day, the share price will head north twice as much (Basware yesterday around 7%).

In Basware’s case, I didn’t buy more at a clear buying point. I won’t make the same mistake again - I’ve bought more HKScan!

Patience is a virtue; in the long run, this is a good stock if you don’t rush things unnecessarily.

Also added at @2.35 a clear buying opportunity.

Can anyone see who’s on the sales floor today?

I also bought a little more.

Looking at Infront, some analyst has predicted a near-zero result for 2019, meaning Q4 should have been clearly profitable. At the same time, the target price is clearly below the current share price, so the numbers are a bit odd. Well, in my opinion, it’s not a bad report at all; it strengthens faith in a turnaround. However, a large company is never turned profitable in just one quarter.

2 Likes

Most owners have a different incentive than traditional investors, meaning the company is not investable.