Swedish Hexatronic once again released an interim report that slightly exceeded Red Eye’s forecasts, so I decided to create my first thread as the company does not yet have its own thread.

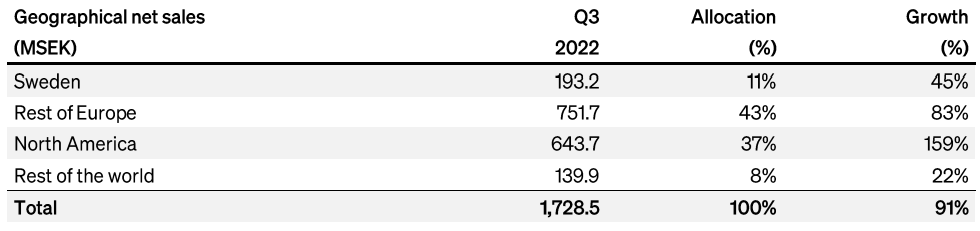

The company operates quite globally, with most of its business currently in the Europe/North America region, but they just made acquisitions in Australia, among other places.

In terms of valuation, it’s not particularly cheap (as no good growth company is at the moment), but it’s not priced like QT either, and the growth figures are convincing.

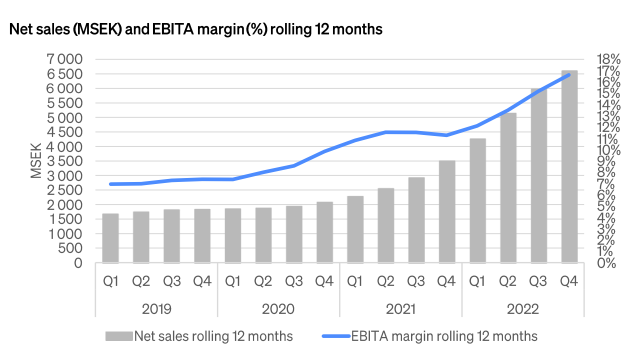

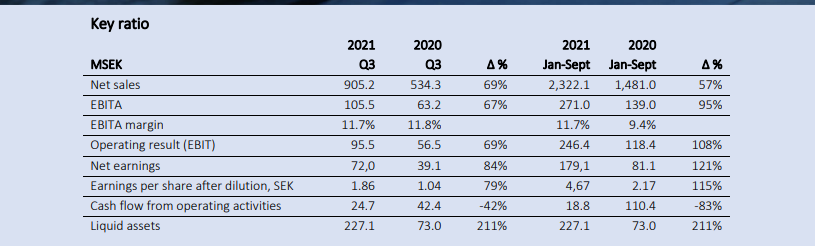

Q3 growth of 69% and growth has been accelerating. Profitability (EBIT%) is slightly over 10%, and profitability has suffered somewhat temporarily due to rising material and freight prices, but not dramatically (unless compared to the Q2 result, which was exceptionally strong).

The company manufactures various cables and conductors.

Products | Hexatronic

Interim reports, including Q3:

Financial (hexatronic.com)

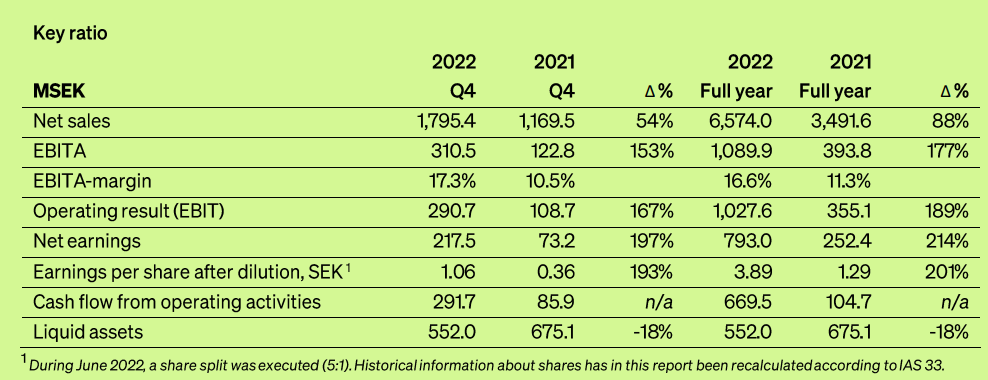

Q3 results

Red Eye’s initial comment:

Hexatronic Q3’21: Sales and Adj. EBITA Beating Our Forecasts (redeye.se)