Let’s start a thread for Purus, which was spun off from Hexagon Composite today. A comprehensive company presentation is available at:

https://cdn.hexagongroup.com/uploads/2020/11/Hexagon-Purus-Company-Presentation.pdf

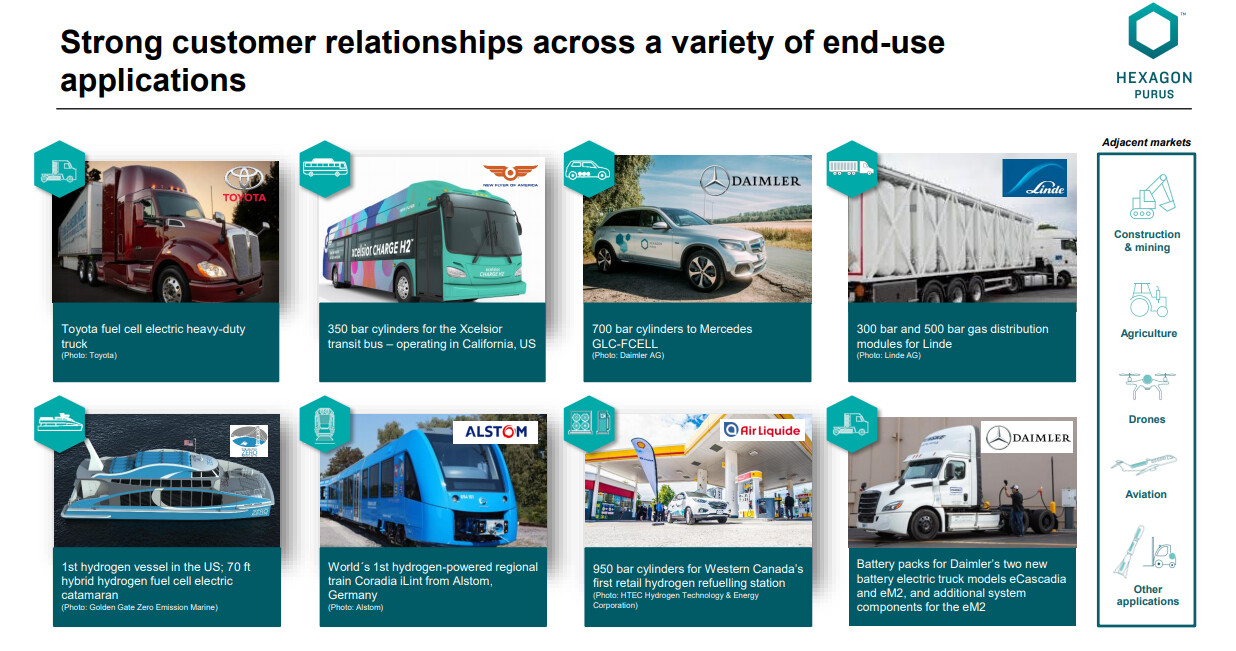

It is the world’s leading manufacturer of “zero emission” hydrogen tanks and battery systems. It holds a leading position especially in Type 4 hydrogen tanks, with applications in hydrogen cars, trucks, buses, trains, ferries, refueling stations, etc.:

Locations:

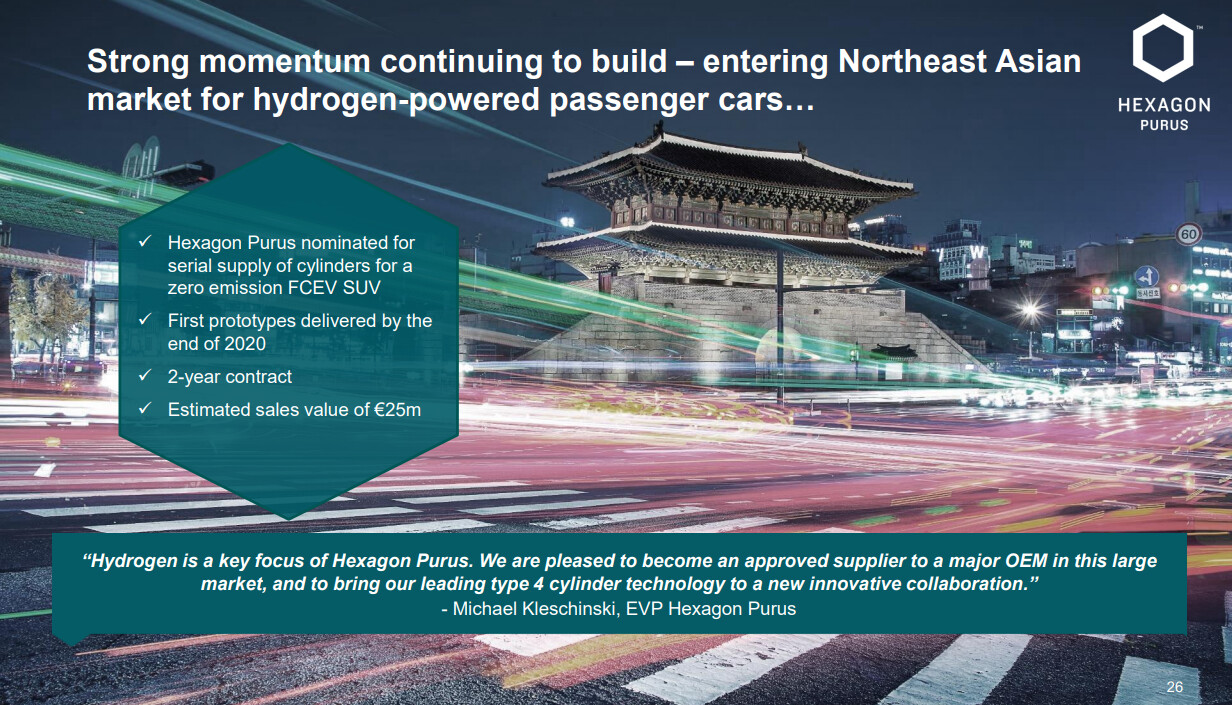

Asia is expected to become the most important region for the company, and it has already secured significant orders, for example, this one:

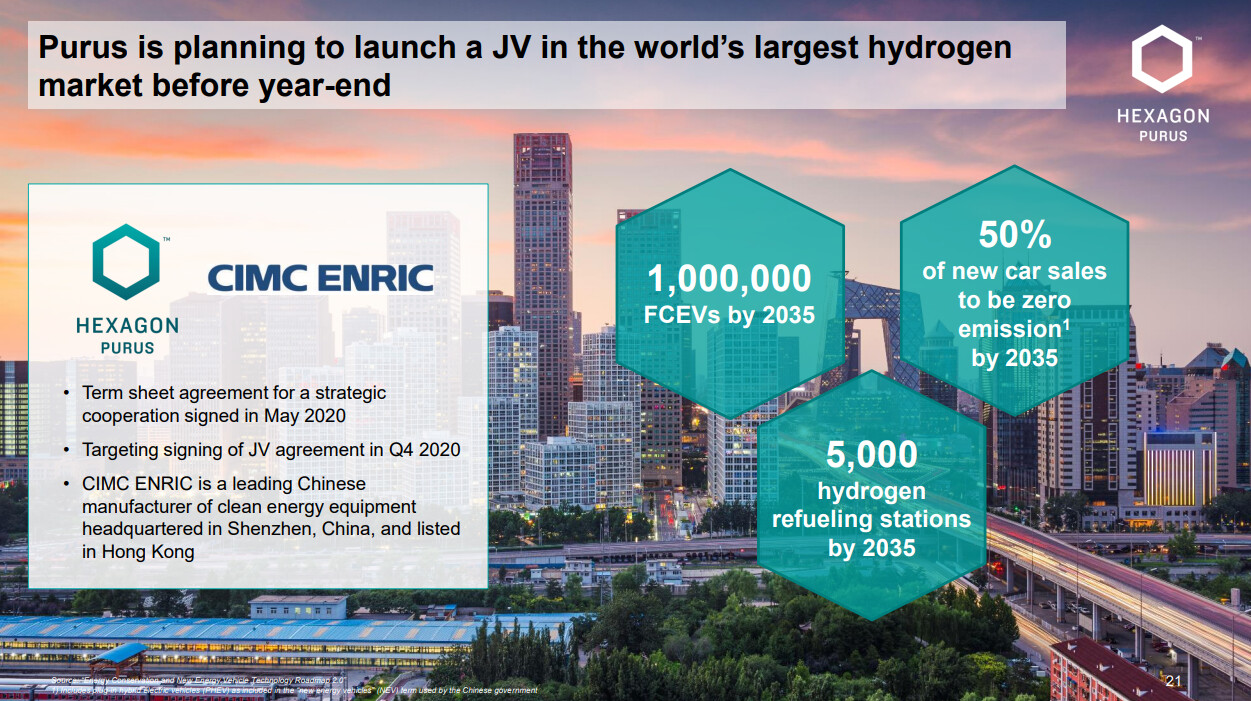

In addition, a JV with CIMC ENRIC is expected to be announced by the end of the year:

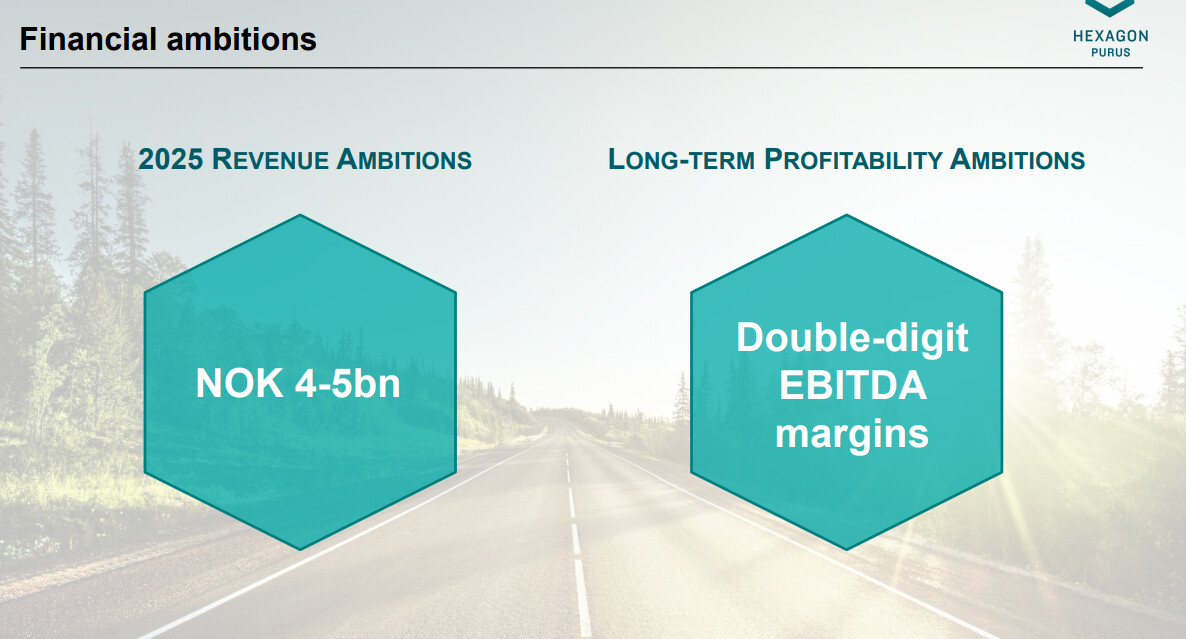

Here are the company’s targets for 2025:

The company currently has ~229 million shares, giving it a market cap of 9500 MNOK ~ €900M at the current share price. Before listing, approximately 750 MNOK was raised in a private placement. Last twelve months’ revenue was 217 MNOK in Q3 and EBITDA was -113 MNOK, so the valuation is “somewhat high”. P/S>40. For next year, the target for revenue growth is over 50%.

Hexagon Composites will host a virtual Capital Markets Day on Monday, January 11, 2021, from 13:00 – 16:00 CET.