I got excited about looking into Hasbro a bit, with the recent #freethewizards activism directed at the company. More on this later; first, some basic information. The text and figures may contain errors. ![]()

Hasbro is a company that owns many well-known brands. Brands familiar to many include My Little Pony, Magic: The Gathering, Dungeons & Dragons, Peppa Pig, and Monopoly.

The company has three reporting segments:

-

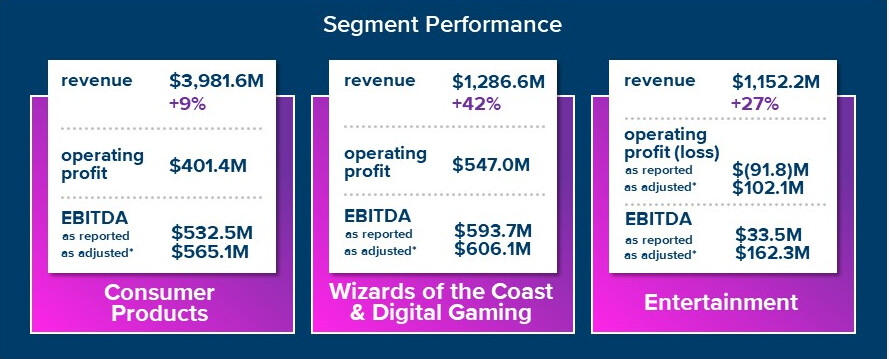

Consumer Products: Toys under their own brands and licensed toys. Previously, for example, there was a licensing agreement with Disney, which transferred to Mattel. Nowadays, they make Marvel toys, among others. A reasonably stable business with small growth. EBIT-% ~10%.

-

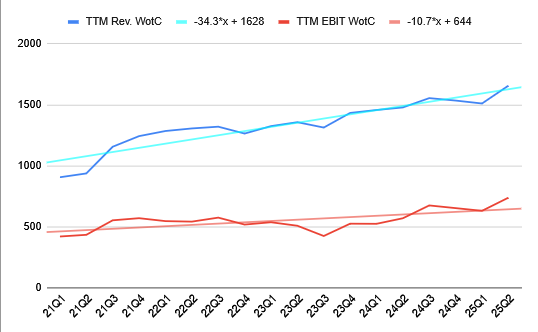

Wizards of the Coast & Digital Gaming: Magic: The Gathering, Dungeons & Dragons, and some other bits and bobs. An estimated 75% of revenue comes from MTG, 15% from D&D, and 10% from others. A fast-growing and very profitable segment. 2019-2021 revenue CAGR 30%, EBIT-% ~43%!

-

Entertainment: TV and film production, and animations. More volatile production business. Here are the big adjustments: eOne Music was sold, resulting in a write-down, as well as a write-down of Discovery Family Channel. EBIT-% ~10%. It is worth noting that this segment was acquired in the eOne acquisition in 2019, and $4.6 B was paid for it!

The company’s “Brand blueprint strategy” tries to achieve synergies by lumping various things under one roof. The strategy seems to emphasize growth more than increasing shareholder value, which is reflected in poor acquisitions. The stock has also been stagnant for the past 5 years.

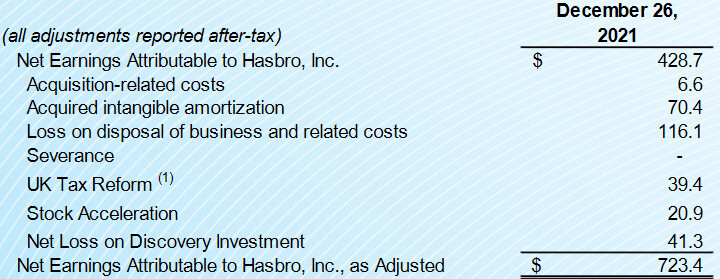

The results include many adjustments, which management can use to hide their poor capital allocation. Of course, including stock-based compensation in the adjustments is questionable, but others, being “one-time,” can be accepted. $116 M is related to the eOne Music sale and $41.3 M to the Discovery Family Channel write-down.

So, at what price can you get this treat?

Shares ~139 M

Share price $84.5

Mcap ~$11.7 B

Cash ~$1 B

Long-term debt ~$3.8 B

EV ~$14.5 BP/E ~27

P/E adj. ~16

EV/EBIT ~19

EV/EBIT adj. ~14.6

EV/EBITDA ~13.9

EV/EBITDA adj. ~11

Now to the meat ![]()

https://freethewizards.com

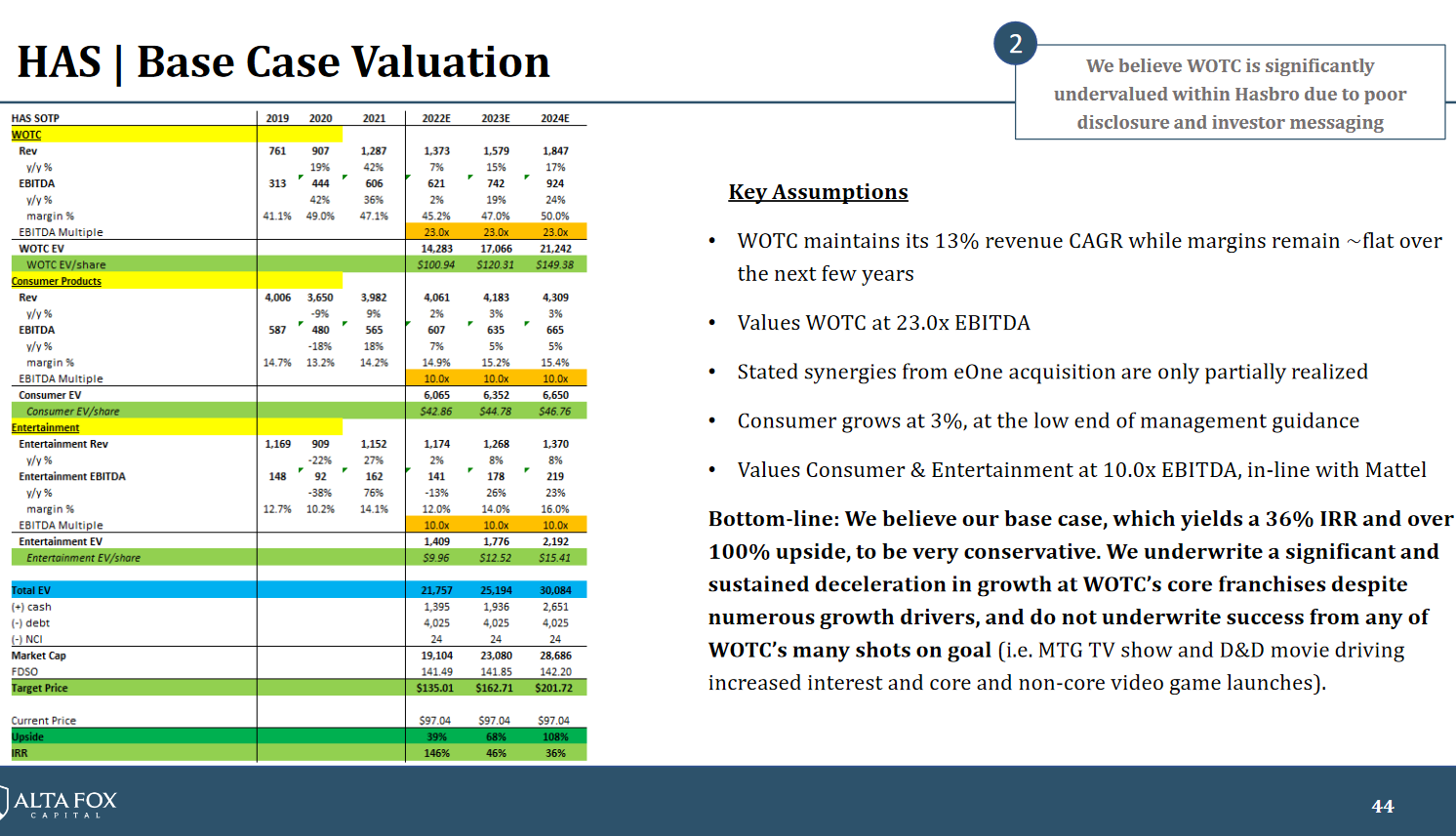

Alta Fox, an activist investor, bought a 2.5% stake in Hasbro and has been pushing for a spin-off of Wizards of the Coast. Their main arguments are:

- Hasbro uses the valuable WotC as a cash cow, even though the company has very attractive investment opportunities, and WotC is growing at double-digit rates even with current insufficient investments.

- Hasbro uses the cash flow generated by WotC for poor investments and not for WotC’s core IPs, i.e., MTG and D&D.

- Investor communication is inadequate, which leads investors to view Hasbro as a toy manufacturer, even though WotC generates half of the earnings.

- WotC has no synergies with the rest of the company. A spin-off would allow WotC to invest its own cash flow into its own operations and grow faster than it currently does.

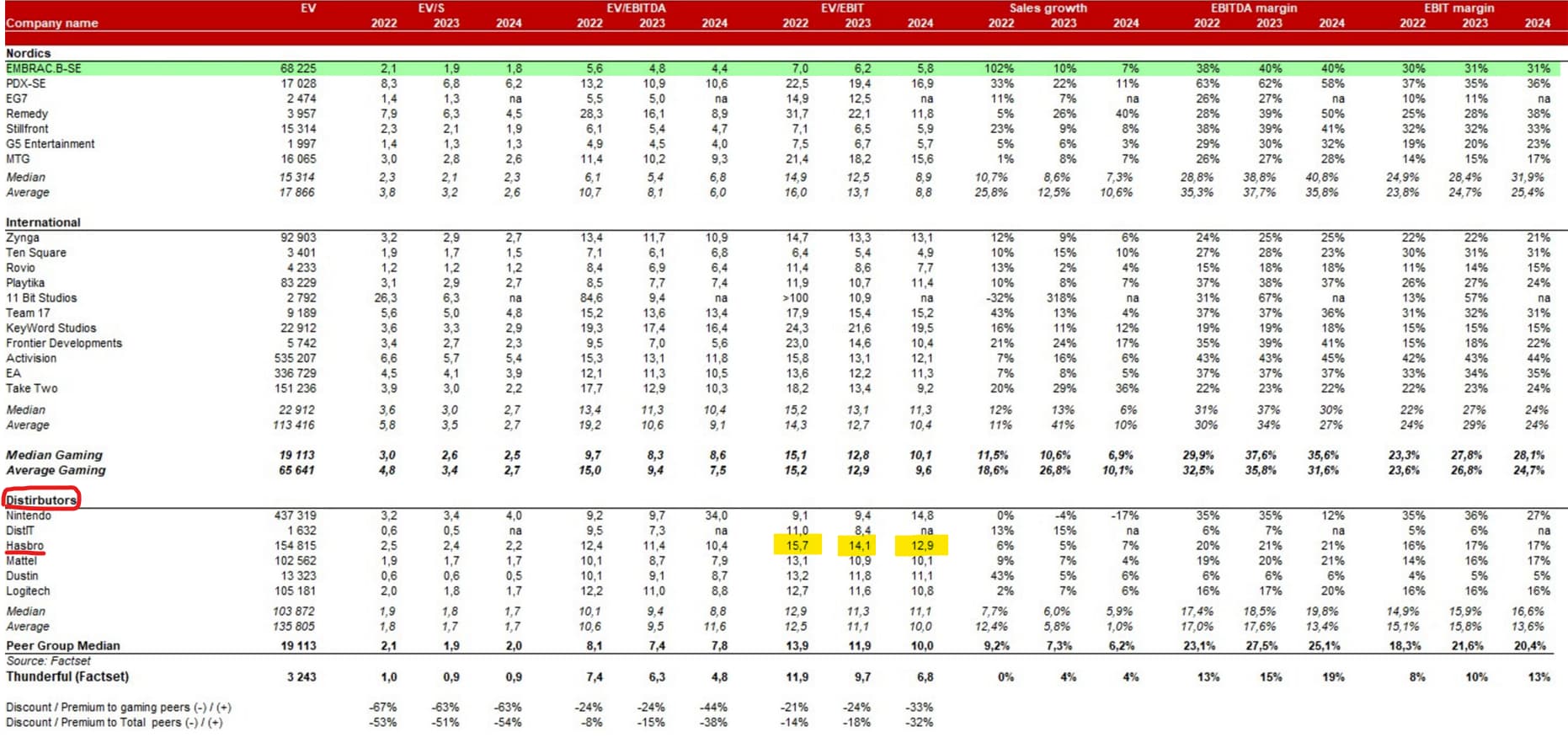

- The market currently values Wizards of the Coast, which generates double-digit growth and an EBIT margin of >40%, at an EV/EBITDA multiple of 12.3. (my own calculation from the current price, assuming others are given an EV/EBITDA multiple of 10)

- The current board, consisting of people from the entertainment and consumer products sectors, is not the right one to lead WotC.

To push for this spin-off, Alta Fox wants to change board members… And the current board opposes this. However, the WotC situation may improve anyway, as former WotC segment head Chris Cocks started as Hasbro’s CEO on February 25, 2022.

https://www.reuters.com/business/exclusive-hasbro-snubs-alta-fox-board-nominee-offer-settlement-talks-sources-2022-03-27/

Edit: Additionally, a link to Alta Fox’s slides:

https://freethewizards.com/wp-content/uploads/2022/02/Alta-Fox-HAS-Presentation-Final.pdf